Barclays (LSE:BARC) (NYSE:BCS) looks like a very different proposition today than it did a month ago. The stock is up 25% over the past month, reflecting renewed positivity following the announcement of a strategic overhaul. Its three-year plan to aid its flagging share price includes a £2 billion cost-reduction plan and £10 billion of buybacks. Moreover, with its return on tangible equity (RoTE) above 10%, Barclays looks vastly underappreciated at 0.5x tangible book value. That’s why I’m bullish on the stock.

Refocusing on Its Best-Performing Division

Barclays is a universal bank and is among the big five banks in the UK. It is also the largest investment bank in both the UK and Europe, boasting a retail and commercial banking arm that serves over 48 million customers globally. The bank primarily operates through two divisions: Barclays UK and Barclays International.

The former generates most of its revenues through net interest income, supplemented by fees charged for wealth management services and Barclaycard usage. Barclays International generates revenues through trading, fees, loan issuance, and other avenues.

Barclays has returned a profit in each of the last 15 years since the financial crisis. However, importantly, the lender has seen returns improve in recent years, with group RoTE above 10% from 2021 onwards. This has been driven by Barclays UK, which averaged a RoTE of 19% between Fiscal 2021-23 despite only accounting for 21% of the bank’s risk-weighted assets (RWA) in 2023. By comparison, Barclays Investment Bank, which accounts for 58% of group capital, has only averaged a 10% RoTE over the three-year period.

As such, it’s reassuring to see Barclays refocusing its efforts on its UK banking operations. The company said it would allocate an additional £30 billion of RWA to its UK retail bank in the years to 2026. Britain’s second-largest bank has already boosted its operations in this area with the £600 million acquisition of Tesco’s (LSE:TSCO) banking arm in February.

The “Goldilocks Zone”

Rising interest rates have been part of the reason for these improving returns. Of course, higher rates are a double-edged sword. On the one hand, they mean Barclays and their peers can achieve higher interest rates on their loans, thus expanding the margin between borrowing and saving rates. On the other hand, they mean a less vibrant market for investment banking, lower demand for loans, and possibly more customer defaults.

As such, there’s something of a Goldilocks zone where banks thrive. In the UK, this is thought to be when the Bank of England’s rates are somewhere between 2.5% and 3.5%. At such a level, margins can remain elevated while impairment concerns fall. While interest rates are expected to remain elevated in the UK for longer, there’s certainly the risk that RoTE will fall in the long run – when hedging strategies have worn down – if interest rates head back to the near-zero levels of the 2010s.

On the topic of hedging, Hargreaves Lansdown (LSE:HL) expects Barclays’s gross hedge income to reach £6 billion in 2025. That’s almost three times greater than in 2022.

Size Is a Moat

As the UK’s second-largest bank and Europe’s largest investment bank, Barclays is simply too big to fail. That’s one of the most compelling moats that any company can have. Nonetheless, size plays a crucial role in the banking world, where profit margins can be particularly sensitive to the prevailing interest rate environment. The scale of a bank’s operations can significantly influence its ability to navigate through economic fluctuations and interest rate cycles.

Moreover, larger banks often have the capacity to implement more sophisticated risk management strategies. They can employ hedging instruments to mitigate the adverse effects of interest rate movements, enhancing their overall financial stability. This capability is especially vital during periods of economic uncertainty or rapid changes in interest rate trends.

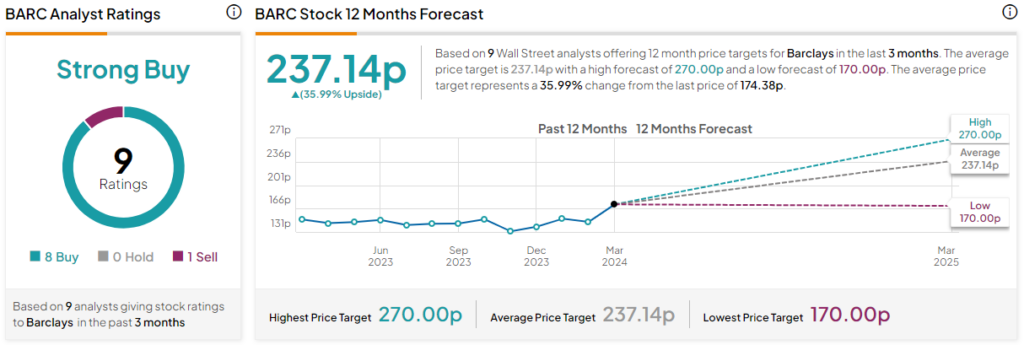

Is Barclays Stocks a Buy, According to Analysts?

Barclays stock is a Strong Buy, according to analysts. The British bank has eight Buys, zero Holds, and one Sell rating. The average Barclays stock price target is 237.14p, inferring 36% upside potential. The most recent analyst forecast, which came from RBC Capital, infers a staggering 52% upside.

The Bottom Line

My investment thesis centers on the excellent value Barclays offers. The bank is trading at multiples far below its peers, especially those in the US. Starting with the price-to-earnings ratio, we can see that Barclays trades at 6.6x, representing a 37.6% difference to the sector.

In fact, across the board, Barclays looks very inexpensive in terms of near-term metrics. Perhaps most alluring is its price-to-tangible-book ratio of 0.5x, and the company currently trades at a huge discount to net tangible asset value. Personally, this indicates that the stock is clearly misvalued, especially considering RoTE has continually exceeded 10% in the past three years. It’s no longer underperforming.

Investors will have to hope that its turbulent relationship with regulators is over, but this shouldn’t overshadow a very positive forecast for the medium term. In addition to a recovering share price, it’s also worth considering that the bank’s 4.6% dividend yield was covered 4x by earnings last year. It’s one of the strongest and most stable on the FTSE 100 Index.