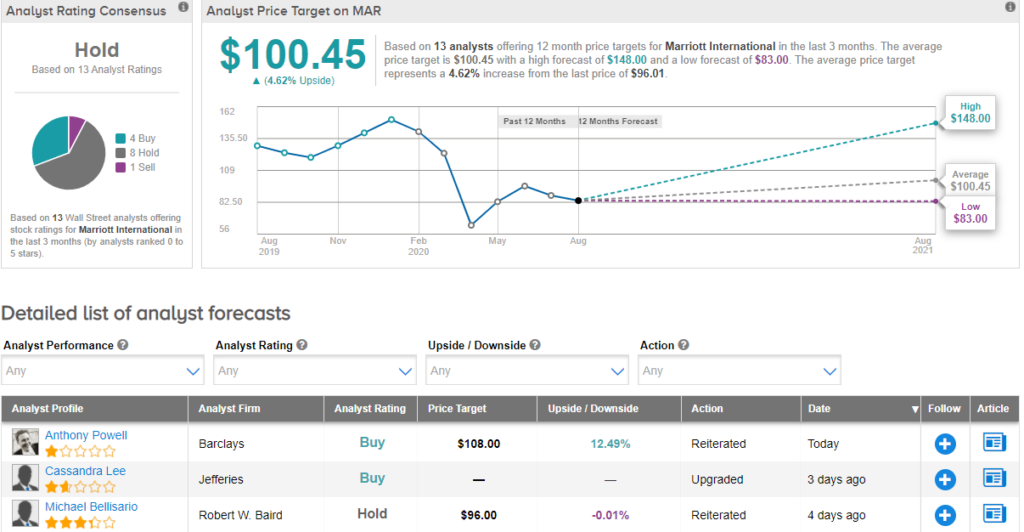

Barclays increased Marriott’s price target to $108 (12.5% upside potential) from $105 and reiterated a Buy rating, amid expectations for a recovery in travel demand once COVID-19 related health problems subside.

Discover the Best Stocks and Maximize Your Portfolio:

- See what stocks are receiving strong buy ratings from top-rated analysts.

- Filter, analyze, and streamline your search for investment opportunities with TipRanks’ Stock Screener.

Barclays analyst Anthony Powell wrote in a note to investors that Marriott’s (MAR) key financial metrics in the China region are “encouraging” and highlight a “number of signs of improvement”. Powell is optimistic about sequential demand improvement in July across the North American region and hopes for more significant recovery once the health situation improves.

Global travel restrictions have been hurting Marriott’s financials. On Aug. 9, the company reported that 2Q revenues plunged 72% to $1.46 billion year-on-year. For the quarter, the hospitality company posted an adjusted loss per share of $0.64 compared with adjusted EPS of $1.56 in the year-ago quarter.

However, its revenue per available room (RevPAR) in the China region was a brighter spot. The key metric in China was down about 61%, compared to 84.4% decline for the whole company. All hotels in the country are now open and occupancy rates have reached approximately 60%, depicting normalizing conditions in the region.

Overall, MAR has a Hold analyst consensus. The average price target of $100.45 implies upside potential of 4.6% to current levels. (See MAR stock analysis on TipRanks).

Related News:

Marriot Posts Wider-Than-Expected 2Q Loss, Sees ‘Gradual Recovery’

Wedbush Sticks To Hold On Nordstrom Ahead Of 2Q Results

Barclays Lifts NetEase’s PT On Gaming Sales Growth Bet