Unlike recent years, 2025 has been anything but bullish for Nvidia (NASDAQ:NVDA) so far. The stock has struggled to gain traction and remains 9% in the red year-to-date.

Various factors have kept sentiment in check, including overall macro uncertainty, specific headwinds such as DeepSeek’s noisy market entry, and the potential for further China export restrictions. Moreover, the chip giant is, in some ways, a victim of its own success, with jittery investors questioning whether further outsized growth is achievable from here on.

So, there’s nothing like a catalyst to reignite momentum – and Nvidia has one coming right up. GTC, its flagship GPU tech conference, takes place this week (March 17–21), and Wall Street will be eager to hear about CEO Jensen Huang’s plans.”

While pipeline updates will surely be forthcoming, Bank of America analyst Vivek Arya thinks much of the focus will be on several other items. These include the recovery of gross margins, with expectations that they bottomed out in the current fiscal first quarter (April) and could expand to the mid-70s% in 2H. Arya considers GM% a “key indicator of NVDA’s pricing power, cost structure and supply chain execution.”

During the Hopper product cycle, gross margins peaked at an unusually high 79%, boosted by factors like expedited product shipments and favorable supply chain conditions. Now, with the transition to the Blackwell architecture, Nvidia is facing cost pressures from manufacturing delays, higher input costs and increased overhead expenses related to installing complex AI systems for customers. These factors have pulled GMs down to 71%. Investors will be watching closely to see if Nvidia can stabilize and improve margins as Blackwell ramps up.

“We believe the ongoing Blackwell transition and related complexity likely the biggest incremental lift NVDA has had to make (rack scale systems, liquid cooling, mask changes, complex CoWoS-L packaging, 12-hi HBM) and changes from here will likely be more manageable,” Arya said on the matter.

The “China impact,” including the effect on the H20 chip and potential offsets from demand outside China (which is estimated to result in a ~$10 billion (5% sales) and 30-40 cent (10% EPS) headwind without offsets), will also be a key focus area.

Additionally, the competitive strength of Nvidia’s GPU platform compared to custom chip (ASIC) alternatives will be under the microscope. Here, given Nvidia’s broad pipeline, the analyst expects Nvidia will hold on to its leading 80-85% share, even in the face of “heavy ASIC competition.”

Lastly, investors will be hoping Nvidia offers some insights on AI TAM and the sustainability of growth beyond CY26.

With NVDA stock’s pullback, Arya sees a “compelling valuation” and accordingly rates the shares as a Buy, with a $200 price objective. This target implies an upside potential of 64%. (To watch Arya’s track record, click here)

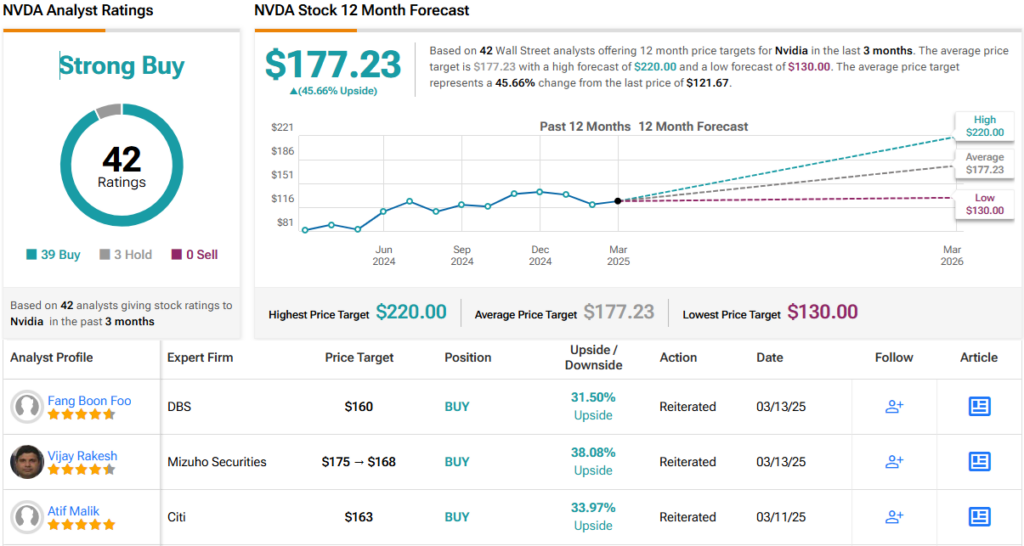

It’s not just Arya who’s bullish – Wall Street is overwhelmingly on board. Out of 42 recent analyst reviews, 39 rate NVDA a Buy, with only 3 opting for Hold. That lands the stock a Strong Buy consensus rating. Meanwhile, the average price target of $177.23 points to a ~46% upside over the next year. (See NVDA stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.