Save the best till last? It’s a play used in many walks of life, but is it about to get applied to the stock market this week? Specifically, we’re talking about the upcoming earnings readout from Nvidia (NASDAQ:NVDA), which is set to take place once Wednesday’s market action comes to a halt.

Invest with Confidence:

- Follow TipRanks' Top Wall Street Analysts to uncover their success rate and average return.

- Join thousands of data-driven investors – Build your Smart Portfolio for personalized insights.

The chip giant has played a significant role in the stock market rally seen over the past year and a half, with a series of estimate-trouncing quarterly reports driving much of the AI-fueled optimism.

But can the company keep on delivering the goods when it announces its fiscal first quarter of 2025 results (April quarter)? It will be a tall order, says Bank of America’s Vivek Arya, an analyst ranked in 7th spot amongst the thousands of Wall Street stock pros.

It’s not that Arya anticipates a disappointing performance from Nvidia. In fact, the 5-star analyst calls the stock a “top pick,” expecting the company will beat Street estimates. The problem is investors have gotten used to Nvidia beating expectations to such an extent that anything less than a blowout quarter and outlook has the potential to send shares tumbling.

According to the “bullish investors” Arya has spoke to, expectations appear to be “well-above consensus estimates as usual,” with sales of $26 billion expected in the quarter, 6% ahead of consensus at $24.6 billion, while the guide is expected to be near the $28 billion mark, ~5% ahead of the Street’s $26.7 billion forecast. Additionally, gross margins are anticipated to reach a peak of 77% in FQ1, with “well-expected outlook” calling for a drop to 75-76% in FQ2 with Arya noting “normalization after some one-off factors” drove GMs above 75% in the last few quarters.

“However,” Arya goes on to say, “even if NVDA were to potentially deliver on these bullish expectations, the stock could still react unfavorably as bears will likely complain that: 1) NVDA QoQ sales growth will decelerate to ‘only’ 7-8% QoQ in FQ2 (Jul) outlook, well below the mid-teens or better the last few quarters, 2) GM peaking and decline is a sign of pricing pressure, unfavorable mix (more China H20 shipments and/or more inference units) and slowing demand/easing supply.”

Conversely, a positive outcome might materialize should Nvidia report a modest beat in FQ1, followed by an optimistic guide for FQ2 (July quarter) calling for 10%+ growth. Additionally, the company could maintain a favorable gross margin of 76-77%, as the Blackwell ramp-up is scheduled for later in the year and the Hopper cost structure “remains favorable.”

Even that, however, might not be enough. “A stronger JulQ ramp, although may raise fears about OctQ facing headwinds, so decision tree stacked against the stock near-term, in our view,” the analyst summed up.

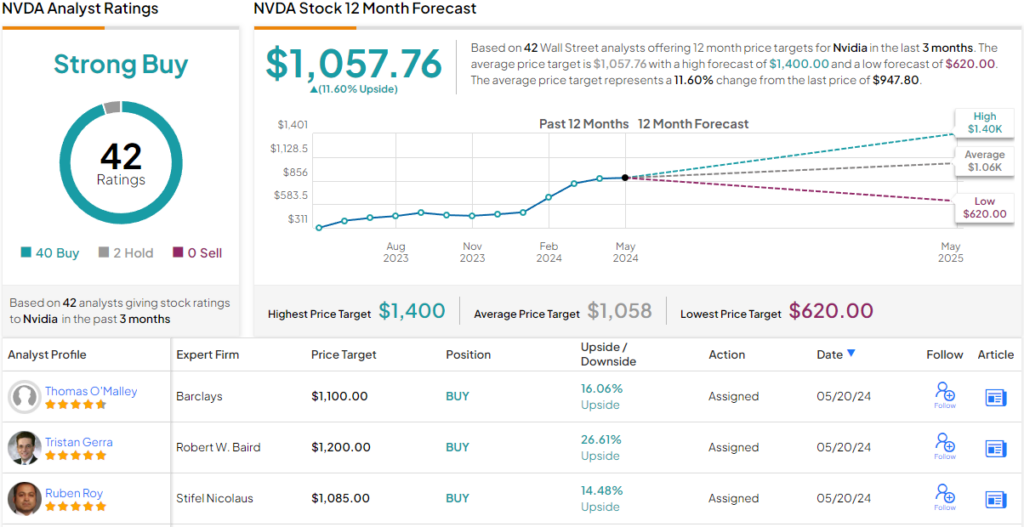

All told, Arya rates NVDA shares a Buy, along with a $1,100 price target, suggesting the stock has room for 16% growth over the coming months. (To watch Arya’s track record, click here)

Nvidia gets plenty of support from the rest of the analyst community. Based on a mix of 40 Buys against just 2 Holds, the stock claims a Strong Buy consensus rating. At $1,057.76, the average target implies shares will climb ~12% higher in the months ahead. (See Nvidia stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.