Diversification is king for Yum! Brands (YUM), the parent company that owns KFC, Taco Bell, and Pizza Hut under one corporate umbrella. The $45 billion market-capped titan operates 61,000 restaurants across 155 countries and wants to chisel away market share from larger rivals. While Mcdonald’s (MCD) remains the juggernaut of the sector and competition is fiercer than ever, I have a few reasons why YUM stock could experience significant upside in 2025.

With an imposing blend of operational resilience, strategic planning, and agility, the company has withstood significant challenges in the global economy and shifting consumer behavior. The stock has risen 18% over the past 12 months, including a substantial 21% bullish run year-to-date. YUM’s franchised model enables the company to keep cash flows steady, collecting enormous royalties even with a reasonably light balance sheet. This could be just the approach YUM needs over the coming years, making me rather bullish on the service restaurant company.

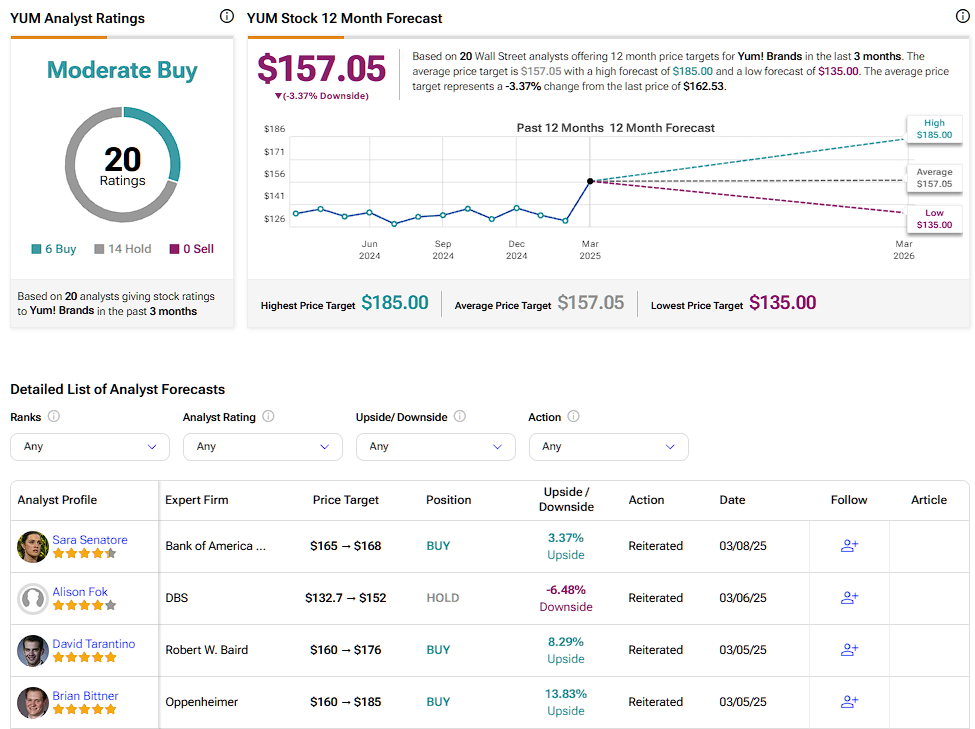

Moreover, Bank of America stock analyst Sara Senatore shifted from her long-held neutral stance this month to become a YUM bull with a corresponding target price of $168 per share. Analysts from Robert W. Baird and Oppenheimer also reiterated their respective Buy ratings last week.

The Growing Yum! Brands Empire

It’s hard to find anyone who hasn’t heard of KFC, Pizza Hut, or Taco Bell, and this will only continue, with almost 60,000 outlets worldwide. The restaurant giant has pulled in an impressive $2.4 billion in sales in Q4 2024, up 16% year-over-year and comfortably ahead of analyst expectations.

It’s not always been such a success, though. In 2024, sales disappointed analysts, and with more than 2,000 stores opening in the previous year, it looked as though management might be scaling at an unsustainable rate. Fortunately, this gamble has paid off, with scale and an adaptable model leading to an enormous presence that few rivals can compete with.

The next leg up for the company appears to be in digital transformation, notably in the Byte platform. This PoS platform, backed by AI, looks to give franchisees leading capabilities made possible by the scale of the operation. This includes mobile ordering, kitchen, inventory and labor optimization and menu management. In the U.S., more than 300 million transactions are being made on the system per year, with 25,000 of the company’s restaurants expected to have it available in 2025. By building on the business model and targeting further emerging markets across India, Africa, and Southeast Asia, patient shareholders should see further company growth to come.

YUM Demonstrates Strength in a Challenging Landscape

From a brief overview, the franchise model looks to be working wonders for the company, with operating profit growing by 8% and labor expenses reducing by a healthy percentage. However, with global economic pressures and uncertain geopolitical dynamics, the landscape is reasonably challenging for companies operating across many regions.

In the last quarter alone, same-store sales declined by 1%, impacted by the conflict in the Middle East and increased competition. Franchise agreements were also halted in Turkey, removing 284 KFC and 254 Pizza Hut stores. However, management still expects unit growth to be between 4% and 5%, so while some regions are proving challenging, the diversity of YUM’s worldwide assets helps mitigate this risk.

Considering the Risks for YUM’s Bullish Case

Despite my bullish stance, it’s always wise to consider the alternative bearish view to maximize objectivity and minimize mistakes. One risk worth keeping an eye on is YUM’s debt ratio. YUM is reducing its debt exposure, but its net debt remains at an uncomfortable 213%. When inflation is still frivolous, and future interest rates are uncertain, YUM’s debt levels could become concerning if not addressed. Where competitors may be able to slash prices in such an environment, YUM’s enormous investments in digital transformation and new stores may undermine the stock going forward.

McDonald’s recent campaign to release $5 meal deals and Domino’s aggressive discounting history show this is already underway to some degree. Although Yum! can arguably do the same, franchisees may resist any moves impacting margins. Investors could quickly lose interest if the sector is forced towards a race to the bottom regarding value.

Is YUM Stock a Good Buy?

On Wall Street, YUM stock carries a Moderate Buy consensus rating based on six Buy, 14 Hold, and zero Sell ratings over the past three months. YUM’s average price target of $157.05 per share implies approximately 3% downside potential over the next twelve months.

My proprietary discounted cash flow (DCF) analysis puts the fair value of YUM’s share price at about $120. If management can achieve around 5% growth in unit sales and see some tailwinds from the digital rollout, there could be some decent upside ahead. The restauranteur’s debt and uncertainty in sales certainly make YUM stock more risky, but by the same token, it opens the door to greater rewards.

YUM Wrestles For Greater Market Share

Investing in YUM stock is essentially a bet on the strength of its global network. While risks exist—primarily related to debt and geopolitical disruptions—management remains confident in the success of its digital transformation and store expansion efforts. Although there may be safer and more lucrative investment opportunities, I believe the company is on the right trajectory, making me optimistic in the near term. Further forward, YUM is on track to turn its short-term successes into long-term market share, given its strongly diversified business model.