Intel (NASDAQ:INTC) had a downer of a year in 2024. While much of the tech industry reaped the rewards of the AI revolution, Intel lagged significantly behind its data center competitors, particularly the market-dominating Nvidia. As a result, Intel shares lost more than half of their value during the year.

Intel’s Board of Directors was clearly unhappy with the company’s trajectory, expressing their displeasure by removing long-time Intel veteran Pat Gelsinger from his CEO position in December. Gelsinger, who was brought back to lead Intel in February 2021, had evidently failed to win over the board with his ‘5 Nodes in 4 Years’ strategy.

While company ‘shake-ups’ can cause instability, they may also help struggling firms begin to turn things around. Not so in this case, asserts one investor known by the pseudonym Value Edge, who argues that Intel’s board has failed to learn from previous mistakes.

“The Board’s co-CEO decision mirrors past mistakes, focusing on product groups while neglecting the critical foundry segment, risking Intel’s future competitiveness,” the investor opined.

Value Edge explains that Gelsinger was in the midst of guiding crucial significant technological developments that could have helped Intel regain its competitive advantage. The investor adds that the company veteran of nearly three decades was exceptionally familiar with Intel, its technology, and the opportunities (and challenges) within the industry.

The newly appointed co-CEOs, however, come from finance and marketing backgrounds – lacking the technical expertise Gelsinger brought to the role. As Value Edge points out, this gap in technical knowledge could further hinder Intel’s efforts to reclaim its standing in the rapidly evolving tech landscape.

“The board wants to focus on the products group, which lost its moat in the first place due to the lagging foundry segment that Gelsinger was trying to fix,” Value Edge argued. The investor contends that an enhanced emphasis on the products group demonstrates a lack of interest in pursuing the investments needed to turn Intel’s Foundry competitive once more.

“The current Board is made up of many of the same folks that have overseen the entire awful past decade for Intel,” concludes Value Edge, who, unsurprisingly, professes scant faith in the current leadership. The investor is therefore downgrading INTC to a Strong Sell. (To watch The Value Edge’s track record, click here)

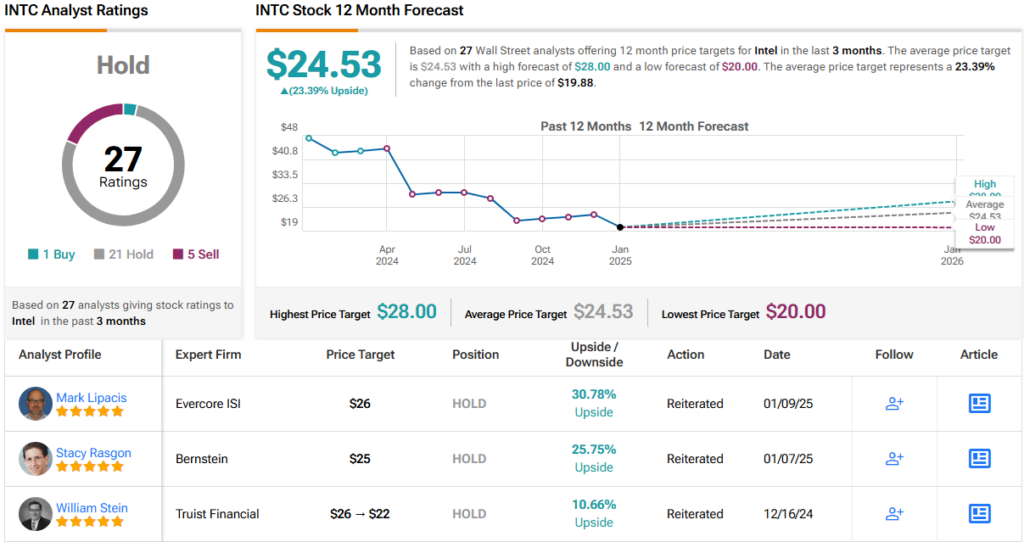

Over on Wall Street, however, the jury is still out. With 1 Buy, 21 Hold, and 5 Sell recommendations, INTC holds a consensus Hold (i.e., Neutral) rating. Nevertheless, its 12-month average price target of $24.53 suggests an upside of 23%. (See INTC stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured investor. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.