Baidu reported better-than-expected 4Q results driven by the strong adoption of its artificial intelligence (AI) tools across cloud services, smart transportation, and autonomous driving end markets. Shares of the China-based tech giant closed 3.6% higher in Wednesday’s extended trading session.

Invest with Confidence:

- Follow TipRanks' Top Wall Street Analysts to uncover their success rate and average return.

- Join thousands of data-driven investors – Build your Smart Portfolio for personalized insights.

Baidu (BIDU) posted non-GAAP earnings of $3.08 per American Depositary Share (ADS), exceeding analysts’ expectations of $2.59. However, its bottom-line declined 19.2% year-over-year as increased expenses remained a drag and offset the benefits from higher revenues.

The company’s total revenues increased 5% year-on-year to $4.64 billion and surpassed the consensus mark of $4.44 billion. Baidu Core contributed $3.54 billion, a 6% year-on-year increase, while sales from the iQIYI unit declined 1% to $1.14 billion.

For 1Q, Baidu forecasts revenues of between $4 billion and $4.4 billion. (See Baidu’s stock analysis on TipRanks)

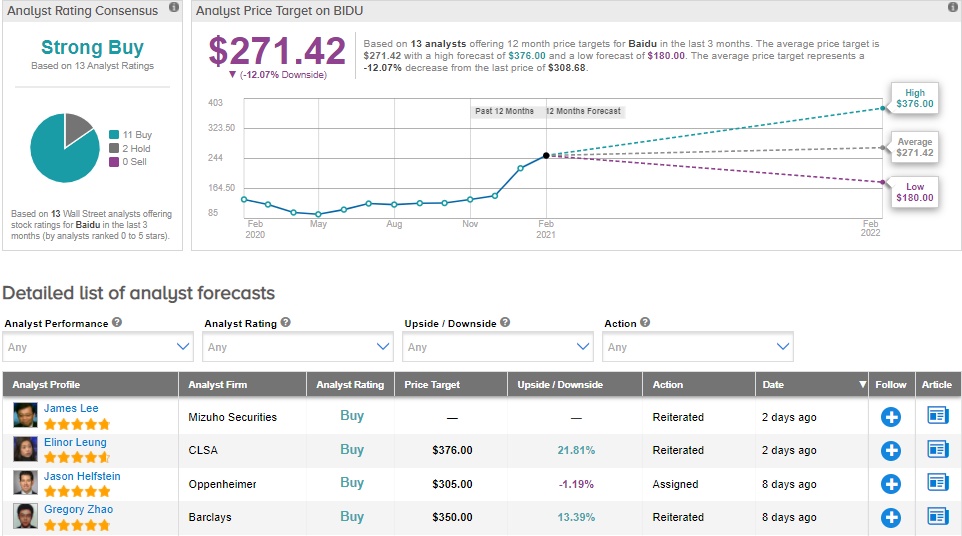

On Feb. 10, Barclays analyst Gregory Zhao raised his price target for the stock to $350 (13.4% upside potential) from $190 and reiterated a Buy rating. Zhao noted that Baidu is the best example of traditional internet services companies successfully entering “frontier tech areas” including AI, chip design, cloud, autonomous driving and smart living. The analyst sees further upside potential in its share price given the recovery in core ad business.

Overall, the rest of the Street has a bullish outlook on the stock, with a Strong Buy consensus rating based on 11 Buys and 2 Holds. The average analyst price target of $271.42 implies downside potential of 12.1% to current levels. Shares are up about 129.4% in one year.

Related News:

Ecolab Dips 4.1% As COVID-19 Dented 4Q Profit

RingCentral’s 2021 Guidance Tops Estimates After 4Q Beat

Lattice Semiconductor’s 1Q Sales Outlook Exceeds Street Estimates