Shares of Aurora Cannabis Inc. (ACB) had a great run in extended market trading on Wednesday after the Canadian cannabis company announced its acquisition of Reliva as a gateway into the U.S. market.

Pick the best stocks and maximize your portfolio:

- Discover top-rated stocks from highly ranked analysts with Analyst Top Stocks!

- Easily identify outperforming stocks and invest smarter with Top Smart Score Stocks

Shares spiked as much as 30% on the news in after-hours trading. Under the terms of the deal, shareholders of U.S.-based Reliva, which sells hemp-derived CBD products, will receive $40 million Aurora shares. The agreement also includes a potential earn-out of up to a maximum of $45 million payable in Aurora shares, cash or a combination thereof, over the next two years subject to Reliva achieving certain financial targets.The deal is expected to close in June.

With Aurora’s stock down 44% since the start of the year, the news may offer some relief for investors. What’s more the company expects the deal to be “immediately accretive to Aurora on an adjusted EBITDA basis” and help drive its goal towards adjusted EBITDA profitability in its fiscal first quarter of 2021.

“Together, Aurora and Reliva will partner to create an international cannabinoid leader that we believe can deliver robust revenue and profitable growth,” said Michael Singer, Executive Chairman and Interim CEO of Aurora. “We have taken the time necessary to carefully assess the Company’s entry into the U.S. market and we firmly believe that the combination with Reliva will create significant long-term value as Reliva provides us options to grow in hemp-derived CBD internationally.”

Aurora has been on a rollercoaster in the past six months with its CEO and founder Terry Booth resigning, while it also reported a bigger first-quarter loss than the market anticipated, slashed 25% of its corporate headcount and cut capital expenditure to C$100 million in the second half of 2020.

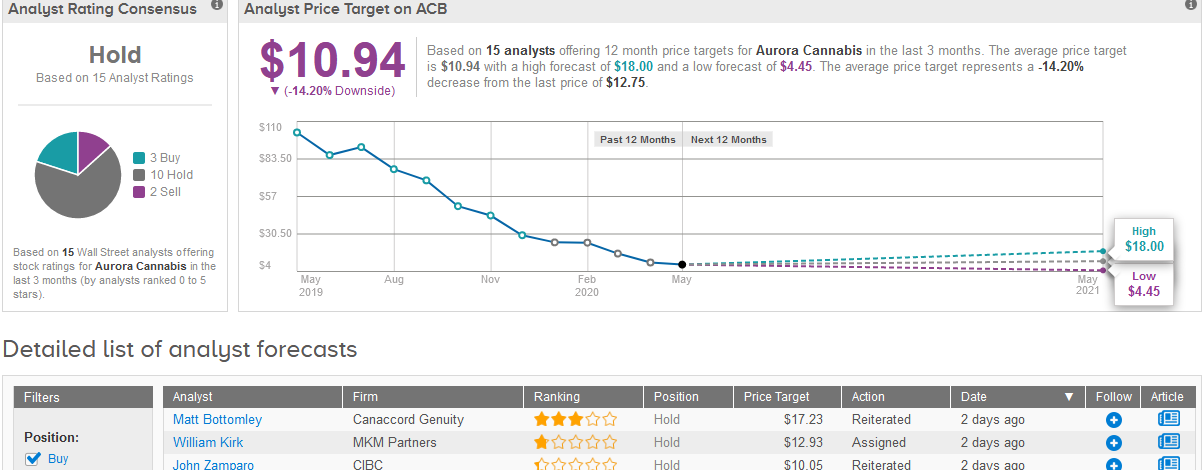

Before the announcement, MKM Partners analyst William Kirk, who has a Hold rating on the stock with a $12.93 price target, said this week that despite the efforts to streamline production, Aurora is still growing far more cannabis than it is able to sell.

“We don’t see demand growth accelerating enough to consume this inventory and expect Aurora to ultimately write it down,” Kirk wrote in a note to investors. “With an uncertain revenue outlook, we don’t yet have enough confidence in cost-cutting measures to rely on their 1Q’21 positive adjusted EBITDA goal.”

Overall, Aurora stock has a Hold analyst consensus backed up by 11 Holds and 2 Sells versus 3 Buys. It appears analysts are also still looking for more confidence in the company’s operations as the $10.94 price target suggests downside potential of 14% over the coming year. (See Aurora stock analysis on TipRanks)

Related News:

Gilead and Galapagos Score Positive Topline Results For Ulcerative Colitis Trial

Moderna Spikes 21% Amid “Positive” Early-Stage Covid-19 Vaccine Data

AstraZeneca-Merck Lynparza Prostate Cancer Treatment Gets FDA Approval