On July 24, U.S. telecom giant AT&T (T) reported its Q2 results, delivering pretty much what shareholders wanted to see: strong cash flows that reaffirmed the dividend safety thesis. My bullish stance on T centers around it being one of the top-income stocks to own. The Dallas-based company continues to reduce leverage and make progress with its investment-led strategy to attract more subscribers. This performance in Q2 confirms that AT&T is on track to remain a strong dividend performer for years to come.

AT&T Q2 Earnings Review

AT&T didn’t beat expectations on either the top or bottom line for Q2. EPS matched estimates at $0.57 but showed a 9.5% year-over-year drop. Revenues hit $29.80 billion, falling short of the $29.98 billion forecast. Is this a reason for AT&T’s stock to plummet? Not quite.

In fact, AT&T’s stock jumped as much as 8.5% in the next two trading sessions. Why? Because there were two key factors more important than just beating the top and bottom line consensus: solid free cash flow numbers and strong subscriber growth.

As I mentioned in a prior article on T stock, AT&T is viewed by many as a top defensive and income stock. Therefore, strong cash flows are crucial for assessing how well the telecom giant is managing its leverage, funding CapEx, maintaining operational flexibility, and, of course, sustaining dividends.

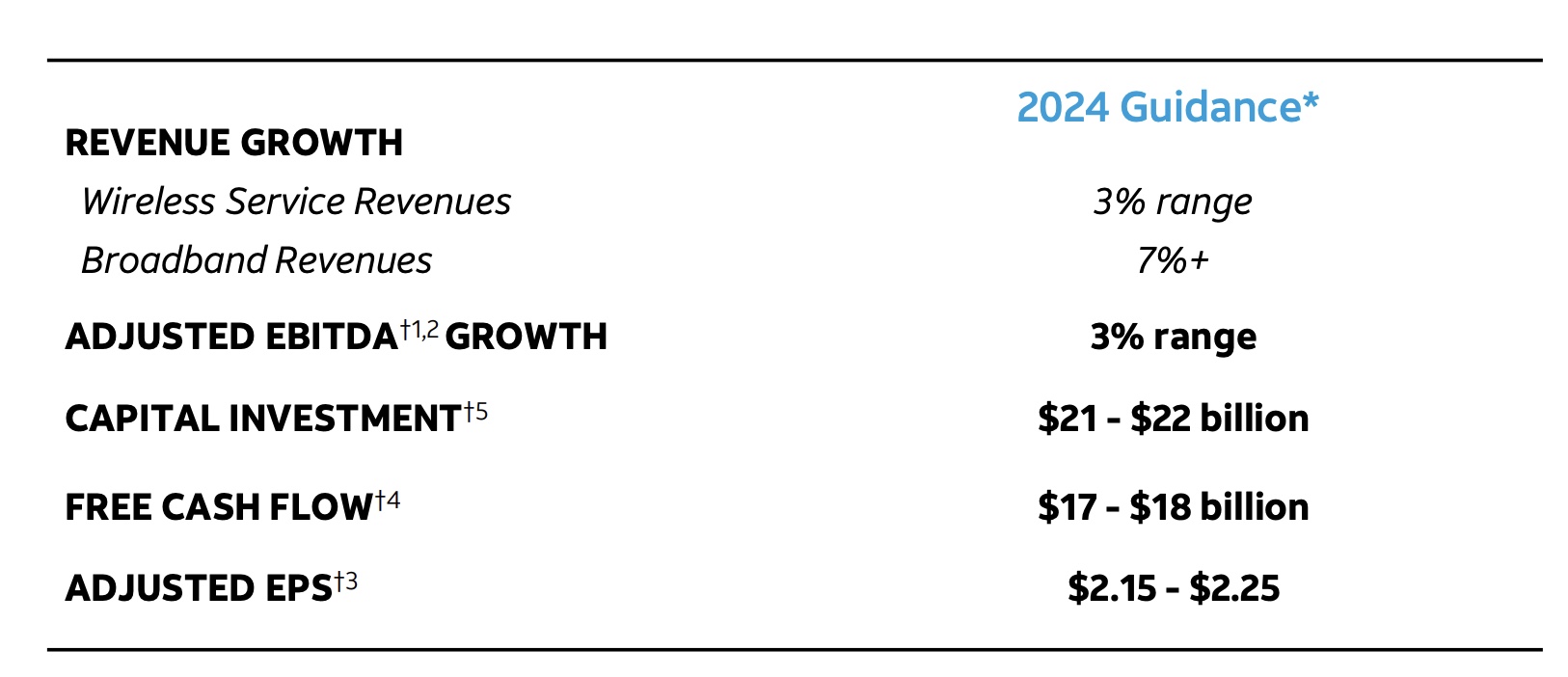

During Q2, free cash flow came in at $4.6 billion, a 9.5% year-over-year increase, and above the $4.2 billion that analysts had forecasted. Management noted that the 3.4% growth in adjusted EBITDA and lower capital investments of $4.9 billion (down $1 billion from the previous year) were key drivers behind this strong free cash flow. The full-year guidance for free cash flow, between $17 billion and $18 billion, seems achievable and even conservative, indicating that the company is on track.

Thus, AT&T’s capital allocation approach looks solid. Even though profits were down in Q2 compared to last year, the robust cash flow shows effective cost management, debt restructuring, and capital management—all of which align with the investment thesis for a defensive income stock like AT&T.

The company has been striking a balance between efficient growth and long-term investments. By paying down debt, AT&T’s net debt to adjusted EBITDA ratio dropped below 2.9 times by the end of June, providing more room to return value to shareholders. Additionally, this strategy has contributed to increased customer acquisition, which was the second-most important highlight for Q2.

AT&T added an impressive 419,000 postpaid phone net subscribers, far exceeding the expectations of around 285,000. This is a notable improvement from the 326,000 added a year ago, thanks to AT&T’s effective customer retention in both wireless and fiber services.

In addition to the growth in subscribers and segment revenue, AT&T experienced an increase in its average revenue per user (ARPU), highlighting the company’s robust monetization potential.

Income Seekers’ Trust Regained and Likely to Strengthen

Not long ago, in August 2023, AT&T was trading near $13 per share. Meanwhile, the 30-year Treasury yield was climbing rapidly to nearly 5%—levels not seen since 2007.

With dividends being a cornerstone of AT&T’s investment thesis and the stock offering a yield of around 6%, it made little sense for investors to take on additional risk with the stock when similar returns were available from lower-risk investment options, such as 30-year Treasury bonds. There was also skepticism about whether cash flows would improve enough to ensure dividend safety, as well as how long these bonds would continue to yield higher returns.

However, since hitting that low, AT&T’s shares have experienced a robust rally that continues to this day.

In 2023, AT&T generated $16.8 billion in free cash flow (FCF) and paid out $8.13 billion in dividends, meaning that only 48% of FCF was used for dividends. This was enough to rebuild income-seekers’ confidence in T stock. With management guiding for a mid-point FCF of $17.5 billion this year, the improvement in FCF is on track, especially after a strong Q2 performance. This naturally explains the favorable impetus for the stock’s appreciation following the Q2 results.

Today, with a dividend yield of 5.9%—still attractive compared to the historically high 30-year Treasury rate of 4.5% but much more stable than last year—there are reasons to believe T investors might see even more dividend increases in the near future.

AT&T’s management is aiming to reduce leverage (net debt to EBITDA) to 2.5x by the first half of 2025. This ambitious goal may signal confidence in continued strong cash flows in the second half of 2024 and could potentially lead to a dividend hike review starting in 2025, assuming the target is achieved.

Is T Stock a Buy, According to Analysts?

After Q2 earnings, analysts mostly remained bullish on AT&T stock, maintaining their previous ratings and forming a Moderate Buy consensus rating. 11 analysts have Buy ratings, while four have Hold ratings. Many have also upgraded their price targets for the stock. Overall, the average price target for T stock is $21.71, which suggests 14.9% upside potential from current levels.

Even analysts who are neutral on T, like Evercore ISI’s Vijay Jayant, raised his price target to $19 from $18, mentioning the in-line Q2 results and the reiterated 2024 outlook.

The Takeaway

AT&T’s Q2 results delivered exactly what income-focused investors wanted: a secure dividend as the company increases free cash flow and reduces debt. This trend is likely to continue until at least mid-2025, with investor confidence in the dividend thesis fully restored. As long as this pattern persists, the stock is expected to rise and, ultimately, increase its dividends, especially as it reaches its deleverage targets.