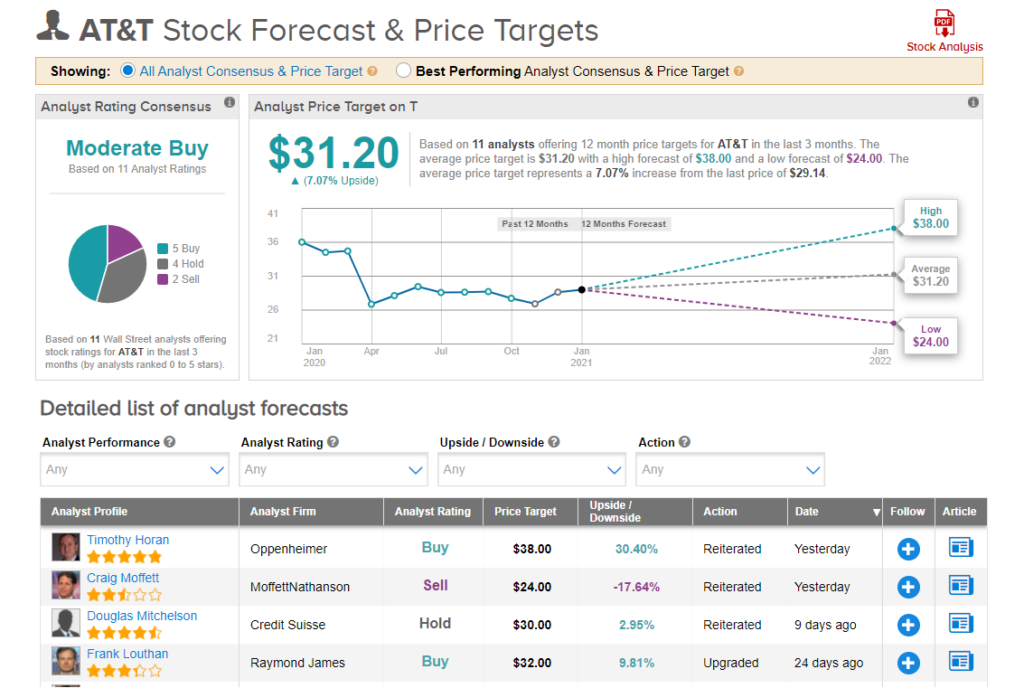

AT&T expects 2021 revenues to grow at a rate of 1% falling short of analysts’ estimates of 1.4%. Shares slipped by 2.1% and closed at $29.14 on Jan. 27.

Discover the Best Stocks and Maximize Your Portfolio:

- See what stocks are receiving strong buy ratings from top-rated analysts.

- Filter, analyze, and streamline your search for investment opportunities with TipRanks’ Stock Screener.

For the fourth quarter, the telecom giant reported revenues of $45.7 billion, exceeding analysts’ estimates of $44.5 billion. AT&T’s (T) posted 4Q earnings of $0.75 per share that came in ahead of analysts’ estimates of $0.73 per share.

The company’s revenues were impacted across most of its business segments due to the Covid-19 pandemic, particularly WarnerMedia and domestic wireless. AT&T’s domestic wireless service revenues generated $14 billion in 4Q20 and were negatively impacted by lower international roaming revenue. Domestic wireless net additions stood at 6 million in the fourth quarter. (See T stock analysis on TipRanks)

AT&T CEO, John Stankey, said, “We ended the year with strong momentum in our market focus areas of broadband connectivity and software-based entertainment. By investing in our high-quality wireless customer base, we had our best full-year of postpaid phone net adds in a decade and our second lowest postpaid phone churn ever.”

“Our fiber broadband net adds passed the 1 million mark for the year. And the release of Wonder Woman 1984 helped drive our domestic HBO Max and HBO subscribers to more than 41 million, a full two years faster than our initial forecast,” Stankey added.

Analysts’ reactions to the 4Q results were mixed. MoffettNathanson analyst Craig Moffett, reiterated a Sell rating with a price target of $24 on the stock. Moffett said that AT&T is moving towards growth over profitability, but in doing that it is also “bumping up against, and through, the ratings agencies’ leverage ceiling.”

The analyst believes that the company’s leverage is “too high for a shrinking company.”

Meanwhile, Oppenheimer analyst Timothy Horan reiterated a Buy rating on the stock and a price target of $38.

“2021 guidance was in line with our estimates with flat rev. and EPS as well as FCF of $26B, on $21B of gross CAPX. Negatively, T will likely sell DTV at a 20% or so FCF yield, and use this to buy ~$20B of spectrum,” Horan wrote in a note to investors.

Wall Street analysts are cautiously optimistic about the stock and the consensus is a Moderate Buy with 5 analysts recommending a Buy, 4 analysts suggesting a Hold, and 2 analysts suggesting a Sell including Moffett’s Sell. The average price target of $31.20 implies 7.1% upside potential to current levels.

Related News:

Verizon Adds Fewer Postpaid Subscribers Than Expected In 4Q; Shares Drop

3M Posts Surprise 4Q Profit Amid Strong Demand For Face Masks

Tilray To Supply Medical Cannabis To France; Shares Gain 14%