Pascal Desroches, AT&T’s (T) Chief Financial Officer, provided shareholders with a business update yesterday at the Credit Suisse Communications conference.

Discover the Best Stocks and Maximize Your Portfolio:

- See what stocks are receiving strong buy ratings from top-rated analysts.

- Filter, analyze, and streamline your search for investment opportunities with TipRanks’ Stock Screener.

AT&T is the world’s largest telecommunications company and the second largest provider of mobile telephone services. (See AT&T stock charts on TipRanks)

AT&T will report its second-quarter 2021 results on July 22, before the market opens. The company reiterated its previous long-term guidance for 2022 – 2024 of low-single-digit revenue CAGR and mid-single-digit adjusted EBITDA and adjusted EPS CAGR, subject to completion of the deal with WarnerMedia.

Regarding WarnerMedia, it expects Q2 results to improve compared to the year-ago quarter, which was the worst hit by the pandemic. The company is looking forward to the international launch of HBO Max and expects to meet its guidance of 67 to 70 million HBO Max customers by the end of 2021.

The company reaffirmed that the current dividend will not be reset before the completion of the WarnerMedia deal. However, Desroches added that after the completion of the deal, the dividend will deliver an attractive yield in the 95th percentile of the dividend-yielding stocks.

Desroches commented that the company has successfully reversed previous subscriber losses driven by its mobility strategy of focusing on the long-term value of its high-value customer base.

Furthermore, management remains confident of posting growth in post-paid subscribers based on current trends and reducing costs by transforming its distribution channels.

AT&T will accelerate its deployment of the C-band spectrum and hopes to cover 200 million people by the end of 2023.

Moving forward, it will also strengthen its network to keep up with the increasing demand for 5G and provide a higher average speed.

In addition, the company plans to double its fiber footprint to around 30 million customer locations by the end of 2025.

New Street analyst Jonathan Chaplin recently upgraded AT&T to Buy from Hold and increased the price target from $29 to $35 (19.5% upside potential).

Chaplin believes that the dividend cut and increase in capital expenditure should create incremental value for the company in the coming years.

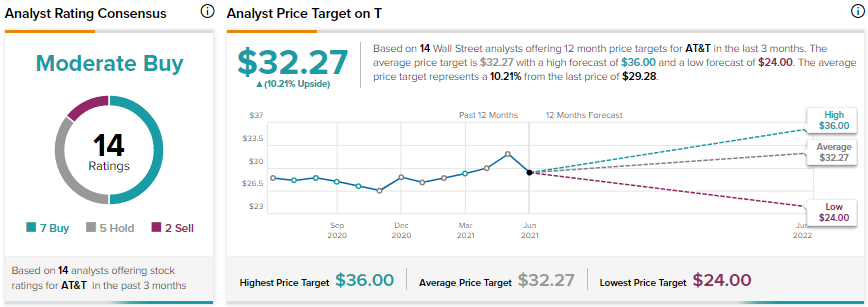

Overall, the stock has a Moderate Buy consensus rating based on 7 Buys, 5 Holds, and 2 Sells. The AT&T average analyst price target of $32.27 implies 10.2% upside potential from current levels.

Related News:

Clean Energy Reveals Plans to Develop Natural Gas From Dairies; Shares Roar

Bentley Systems Snaps Up SPIDA to Accelerate its Grid Resilience

Bank of America Expands Financial Centers in Kentucky