SBA Communications (NASDAQ:SBAC) stock is currently at five-year lows. The telecom REIT, which owns nearly 40,000 cell towers, has seen its shares experience a consistent decline since 2021, currently hovering at levels last seen in early 2019. This can be attributed to high interest rates, which have hindered its growth prospects. Still, SBA has set the stage for another year of record profits, with its business model proving quite resilient against the ongoing headwinds impacting the sector. Thus, I remain bullish on SBAC stock.

SBA’s Core Leasing Business Remains Incredibly Robust

SBA’s core business model, accounting for over 90% of its total revenues, revolves around leasing telecom towers to major industry players. For context, last year, about 67% of SBA’s total revenue came from T-Mobile (NASDAQ:TMUS), AT&T (NYSE:T), and Verizon (NYSE:VZ). SBA’s towers are critical infrastructure for these companies, ensuring reliable signal coverage.

Because of their essential nature, these assets tend to generate highly predictable and resilient cash flow irrespective of the conditions that impact the real estate sector overall. The company’s most recent results illustrated this concept, with Site Leasing revenues in Q1 coming in at $628.3 million, up 1.5% compared to last year.

On the domestic front, which accounts for 73.4% of its total revenues, same-tower Recurring Cash Leasing Revenue grew by 5.9%. On a net basis, same-tower growth came in at 2.3% due to a churn rate of 3.6%. However, note that about $7.5 million of the Q1 churn was related to Sprint’s consolidation with T-Mobile U.S. Thus, churn would have been a negligible 1-2% excluding this development, stressing the mission-critical nature of SBA’s tower infrastructure.

On the international front, which makes up the remaining chunk of SBA’s revenues, same-tower Recurring Cash Leasing revenue growth was 3.3% in constant currency, net. This includes 4.8% of churn. Therefore, the same-tower gross growth would have been 8.1%. The above-average churn is attributed to carrier consolidation in this case, as well. However, the underlying rationale regarding the critical nature of SBA remains the same, shielding its long-term prospects.

If anything, I believe it is commendable that SBA posted growth internationally despite its rates being impacted by a declining local CPI link escalator in Brazil (its largest international market, accounting for about 30% of its total towers).

Rising Rates Hamper SBA, But Capital Allocation Saves the Day

As highlighted in the introduction, the primary challenge that has hampered SBA’s stock price in recent years is that interest rates remain high. This trend echoes across the REIT landscape, as heightened rates adversely affect companies within the sector in two distinct ways.

First, it constrains a REIT’s growth and profitability prospects. This is due to the increased cost of issuing debt, which is essential for financing expansion—in this case, the construction or acquisition of additional towers. Secondly, income-oriented investors, who typically hold towards REITs for their dividends, shift their holdings towards fixed-income securities, as they offer better risk/reward profiles. This leads to further downward pressure on REIT share prices, and SBA has not been an exception.

SBA cannot really do much to impact its share price other than maybe buybacks, which management has been utilizing lately. However, it can do a whole lot more to mitigate the impact of rising interest rates on its profitability. Capitalizing on the qualities of recurring cash flows, SBA has been reducing its net debt while increasing its adjusted EBITDA, thereby reducing its net leverage (see below).

With SBA reducing its debt and the bulk of its borrowings being at fixed rates, the company has more than offset any impact that rising rates would have on its profitability. Evidently, in Q1, SBA registered interest expenses of $89.1 million, down 9.5% compared to last year.

The combination of strong leasing revenue, lower interest expenses, and a slightly lower share count led to adjusted funds from operations per share (AFFO/share, a cash-flow metric used by REITs) coming in at $3.29, up 5.1% compared to last year. Management’s guidance suggests that this trend will be sustained throughout the year. In fact, the midpoint of its AFFO/share outlook, $13.28, points to another record year of profitability.

Is SBAC Stock a Buy, According to Analysts?

Regarding Wall Street’s view on SBA Communications, the stock has attracted a Strong Buy consensus rating based on 10 unanimous Buys assigned in the past three months. At $243, the average SBAC stock price target implies 29.75% upside potential.

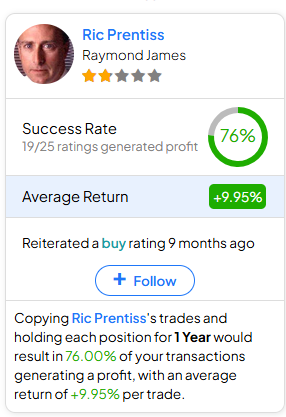

If you’re uncertain which analyst you should follow if you want to buy and sell SBA stock, the most profitable analyst covering the stock (on a one-year timeframe) is Ric Prentiss from Raymond James, boasting an average return of 9.95% per rating and a 76% success rate. Click on the image below to learn more.

The Takeaway

In conclusion, while SBA stock may have experienced a heavy downturn, its fundamental strengths remain intact. The company’s core leasing business, supported by its critical tower infrastructure, continues to generate predictable and resilient cash flows.

In the meantime, despite challenges posed by high interest rates, SBA’s smart capital allocation, including debt reduction, has mitigated these impacts, setting the stage for record AFFO/share this year. With the stock trading at multi-year lows against its financials improving, I remain highly optimistic regarding its overall prospects.