Big changes are taking place on fast-growing tech firm ZoomInfo Technologies’ (ZI) shareholding structure and composition. Early institutional investors in ZoomInfo stock, including the company’s co-founders, are selling huge blocks of stock while taking profits.

ZoomInfo Technologies provides an advanced, cloud-based, machine learning (ML) and artificial intelligence (AI) enhanced go-to-market data, insights, and analytics platform for marketers to efficiently target corporate customers. The company recently went public, in June 2020. Shares have rallied by 109% over the past twelve months, and several insiders are cashing out.

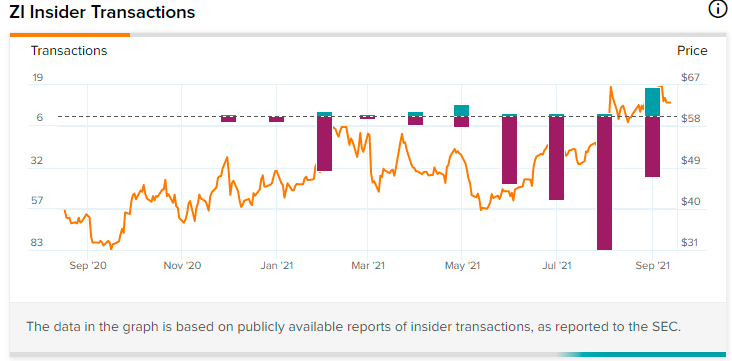

Insiders in the $25 billion company have disposed of more than $7.8 billion worth of ZI common stock during the past three short months. The net selling is significant in light of the company’s total capitalization right now. Should individual investors be concerned? (See ZoomInfo Technologies stock charts on TipRanks)

I am bullish on ZoomInfo stock.

Insider Sales Accelerate on ZoomInfo Stock

Generally, corporate insiders know the company better than any of us “outsiders” can. For this reason, watching and analyzing insider activity can offer important insights when deciding whether to buy, sell or continue holding onto a company’s shares.

We have seen a rapid increase in insider activity on ZI stock lately. Directors, officers, and institutional investment funds were heavy net sellers since June this year.

Should Investors be Concerned?

Given the massive net selling by key insiders on ZoomInfo Technologies stock over the most recent three months, individual investors may be asking: Do these insiders know something we don’t?

Perhaps the most important question would be whether individual investors should follow insiders’ lead, and sell their positions on ZI too.

While the above questions are relevant for anyone invested in ZI stock and to everyone intending to buy the company’s shares today, most transactions were actually “uninformative” as rated by TipRanks, and we may find the recent Buys in September more informative than August Sells.

ZI Insider Sales Less Important than Latest Buying Activity

As recently as Wednesday, September 8, insider net sales amounted to $8.2 billion. The figure included two secondary offerings of 20,000,000 common shares at $63 each and 27,000,000 shares at $55.25 in August for total gross proceeds of $2.75 billion. Investment funds including The Carlyle Group (CG), TA Associates, and 22C Capital and ZI’s co-founders were the selling shareholders.

After funding the riskiest part of a youthful business through its early financing rounds, venture capital and private equity funds employ exit strategies to monetize their holdings and return capital to fund investors. An initial public offering (IPO) is one good exit option, and it’s the most preferred one for liquidity and better price discovery reasons.

Post ZoomInfo’s IPO in June last year, early investors were yet to effectively monetize their positions since a lock-up period that expired on November 29, 2020. They were free to liquidate their holdings soon after the lock-up period expired, yet they have been patient and are taking their time to do so.

Actually, we even saw some significant insider buying activity during the past week. Directors and related investment funds including TA Associates bought millions worth of stock during the past week, as three-month net insider sales declined by $400 million from $8.2 billion to $7.8 billion.

Insiders may sell a stock for several noble reasons, but they usually buy their own company’s shares for one main reason: the potential for lucrative future capital gains.

Are ZI Shares a Good Idea Now?

In September, ZoomInfo committed to removing the complexity in its shareholding structure. The company will eliminate several classes of common shares by converting them all into Class A shares over the next quarter.

The removal of Class B, Class C, and Up-co units gives equal voting power to every common share unit, enhances corporate governance, and allows for easier mergers and acquisitions transactions while reducing administrative costs.

However, that’s not the best part of a Buy thesis on ZI stock right now.

In ZoomInfo, we have a high growth business that reported a 57% year-over-year revenue growth rate for the second quarter of 2021, to $174 million. This followed another strong 50% sales growth rate reported for the first quarter of this year. Profit margins have expanded lately, with a second-quarter gross margin of 86.8% topping records, while free cash flow generation holds strong.

Rapid growth, strong profitability, and enhanced cash flow generation capabilities are what growth investors usually search for, and ZI stock offers all these qualities in good measure.

Analysts expect the company to grow sales by 30.8% in 2022 after an emphatic 48% top-line growth projected for this year. Normalized earnings could grow by nearly 33% after a projected 50% increase for 2021, while free cash flow for 2022 could jump by 36% year-over-year to nearly $370 million.

Despite stretched valuations today, ZoomInfo appears to be a great business to own for the long term.

Analysts’ Take on ZI Stock

Wall Street analysts are currently bullish on ZI stock. Data on TipRanks show consensus analyst rating on ZoomInfo stock at Strong Buy, with an average ZoomInfo price target of $72.17 a share, indicating a potential upside of 7.7% over the next twelve months.

Out of the 12 trained analysts following the company, 10 rate the stock a Buy, two recommend holding existing positions, and none are recommending a sell at the moment.

Investor Takeaway

The recent surge in insider sales on ZoomInfo Technologies stock seems like normal monetizations of long-held positions by investing funds following their mandates. There is no significantly indicative information in them for investors to decode as a Sell signal.

That said, significant insider buys during the past week could only indicate bullishness on the part of well-informed corporate insiders. Perhaps that’s the signal anyone considering buying new shares ought to investigate further.

Disclosure: At the time of publication, Brian Paradza did not have a position in any of the securities mentioned in this article.

Disclaimer: The information contained in this article represents the views and opinion of the writer only, and not the views or opinion of Tipranks or its affiliates, and should be considered for informational purposes only. Tipranks makes no warranties about the completeness, accuracy or reliability of such information. Nothing in this article should be taken as a recommendation or solicitation to purchase or sell securities. Nothing in the article constitutes legal, professional, investment and/or financial advice and/or takes into account the specific needs and/or requirements of an individual, nor does any information in the article constitute a comprehensive or complete statement of the matters or subject discussed therein. Tipranks and its affiliates disclaim all liability or responsibility with respect to the content of the article, and any action taken upon the information in the article is at your own and sole risk. The link to this article does not constitute an endorsement or recommendation by Tipranks or its affiliates. Past performance is not indicative of future results, prices or performance.