Zoom Video Communications (ZM) is one of the leading enterprise video communication companies in the world. Its cloud platform provides mobile and desktop video and audio conferencing, chat, and webinars.

Maximize Your Portfolio with Data Driven Insights:

- Leverage the power of TipRanks' Smart Score, a data-driven tool to help you uncover top performing stocks and make informed investment decisions.

- Monitor your stock picks and compare them to top Wall Street Analysts' recommendations with Your Smart Portfolio

The company benefited from pandemic tailwinds, but it has been losing ground since the economy reopened. The stock has dropped around 71% in the last year and 52% year-to-date. Apart from the changing market dynamics, Zoom appears to be losing steam as a result of increased competition.

Zoom, on the other hand, has been concentrating on the enterprise market. These businesses are responding to the desire of today’s workforce for remote employment. As a result, the organization is making all efforts to improve its offerings for the enterprise segment.

Recent Acquisition

Zoom said last week that it had reached an agreement to buy AI-based support platform Solvvy for an undisclosed sum. Solvvy is a customer-support-focused conversational AI and automation platform.

The agreement will provide improved customer service to a worldwide enterprise workforce. As a result of the agreement, Zoom will be able to add another intriguing product to its already impressive portfolio.

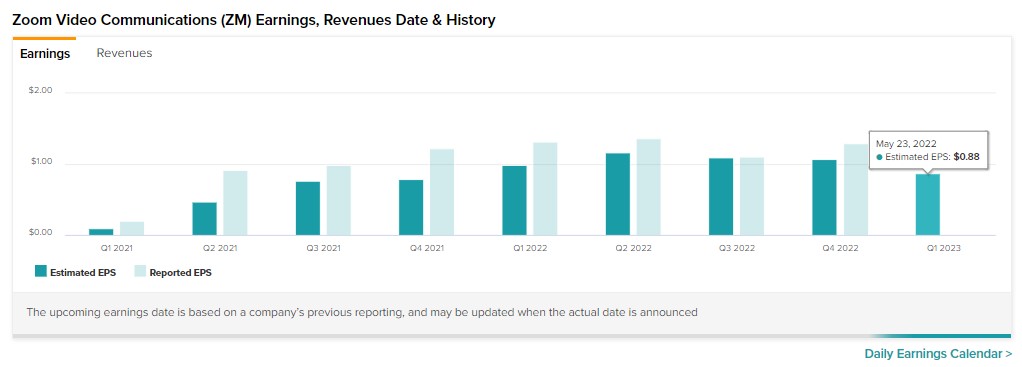

Q1 Results: What to Expect?

As ZM is expected to report its Q1-2023 earnings next week on May 23, let’s take a look at the company’s expectations for the upcoming quarter.

According to analysts, Zoom Video is projected to report adjusted earnings of $0.88 per share in the first quarter. This reflects a decline of 33.3% year-over-year.

Zoom’s fiscal first-quarter revenue is expected to be in the $1.07-$1.075 billion range. Meanwhile, adjusted earnings for the first quarter are expected to range between $0.86 and $0.88 per share.

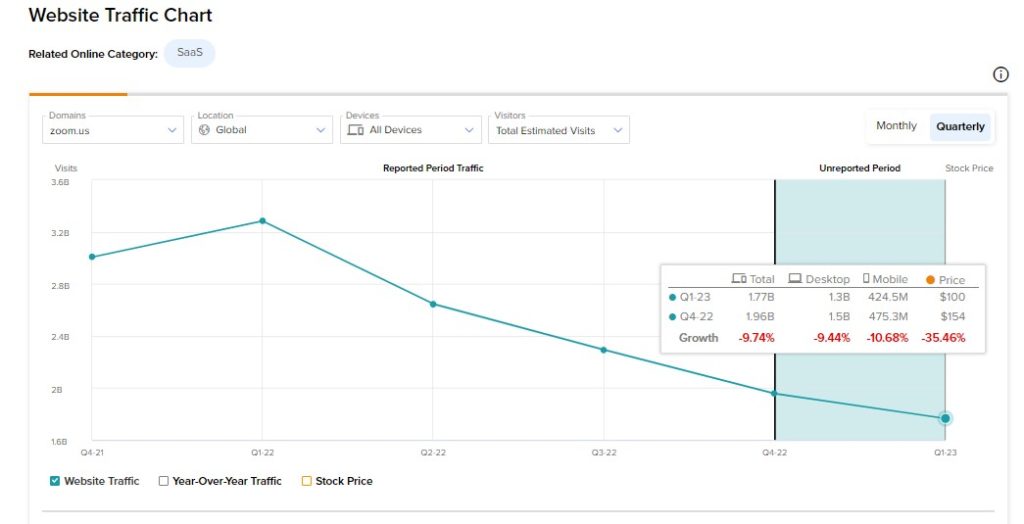

Website Visit Stats Remain Disappointing

As a cloud-based video conferencing provider, tracking user visits to the company’s website is critical for establishing the popularity of its solutions. Because Zoom derives the majority of its money through subscriptions to its communications platform, more visitors might lead to more subscriptions, which would result in more revenues, and vice versa.

As a result, we investigated Zoom’s monthly user data using TipRanks’ new website tool to get a clearer view of the company’s current status ahead of the Q1 print.

The tool revealed that overall expected visitors to the Zoom website decreased in Q1. Notably, the total global visits to zoom.us.com decreased 9.7% sequentially to 1.77 billion in the first quarter.

As shown in the graph above, Zoom’s platform appears to be losing traction as schools and offices have reopened, and the demand for its solutions seems to decline.

Wall Street’s Take

Ahead of the Q1 earnings release, Citigroup analyst Tyler Radke is concerned about the highly competitive landscape and recent high churn rates among consumer and small-business accounts.

He writes, “We have grown more cautious of the competitive landscape based on inputs from partners and customers.”

As a result, Radke maintained a Neutral rating on the stock and decreased the price target to $118 from $139 per share.

On TipRanks, Zoom stock commands a Moderate Buy consensus rating based on 10 Buys and 15 Holds. The average Zoom price target of $153.59 implies upside potential of approximately 74.4% from current levels.

Bottom Line

The changing work environment may keep Zoom’s short-term prospects murky. People are returning to work, and schools have reopened as well. Increased competition from other video conferencing players is also a source of concern.

Despite the aforementioned obstacles, the workplace continues to undergo a digital transformation, and Zoom offers and solutions may continue to be in high demand. As a result, Zoom may still be a good long-term investment.

It will be interesting to see if the company is able to report strong top and bottom-line numbers this quarter.

Learn more about the Website Traffic tool in this video by YouTube sensation Tom Nash.

Discover new investment ideas with data you can trust

Read full Disclaimer & Disclosure