For a day that marked Tesla’s (TSLA) fifth straight quarter of reporting positive profits, last week’s 0.7% increase in the share price of Tesla stock seemed somewhat underwhelming.

Invest with Confidence:

- Follow TipRanks' Top Wall Street Analysts to uncover their success rate and average return.

- Join thousands of data-driven investors – Build your Smart Portfolio for personalized insights.

Reporting earnings Wednesday night, Tesla closed trading Thursday up only modestly, and really, only barely outperforming the S&P 500’s overall 0.5% move. Tesla called Q3 its “best quarter in history,” with pro forma earnings coming in 36% ahead of expectations at $0.76 per share, sales of $8.8 billion about 6% better than predicted, and free cash flowing strongly — $1.9 billion over the past 12 months.

Tesla told investors Wednesday that it remains on target to produce and deliver half a million electric cars this year, despite the fact that “this goal has become more difficult” to achieve in the face of Covid-19. Cybertruck deliveries are expected to begin late next year. Even Tesla’s “energy” business — solar roofs and solar storage — looks “poised for strong growth,” said the company.

Much of Wall Street applauded the news, with R.W. Baird and JMP Securities both upgrading Tesla shares to “outperform” and Piper Sandler calling Tesla a “must-own” stock, and as both Oppenheimer and RBC Capital raised price targets on the shares. One analyst, however, stood out from the crowd for his continued pessimism on Tesla:

Gordon Johnson of GLJ Research says Tesla is still a “sell.”

Urging investors not to forget the forest for the trees, Johnson reminds Elon Musk fans that Tesla continues to rely heavily upon taxpayer-funded subsidies in the form of tax credits for the production of zero-emission vehicles (ZEV). With automotive giants such as Ford (F), General Motors (GM), and Volkswagen all ramping up their own sales of electric cars, though, soon they will not need to buy ZEV credits from Tesla to hit their fuel efficiency targets set by California and other “green” states. And this could become a problem for Tesla, says Johnson, because the sale of ZEV credits continues to make up literally all of money that has kept Tesla’s profits positive these past five quarters.

Ultimately, the 100%-profit revenues generated from the sale of ZEV credits will disappear, warns Johnson, noting that “TSLA, itself, describes credit sales as non-recurring in nature.” Although the analyst admits that Tesla’s gross margins have grown nicely, hitting 25% in the third quarter even discounting the effect of ZEV credit sales, trouble emerges a bit closer to the bottom line. Johnson notes that the company remains GAAP unprofitable but for the effect of ZEV credits. Back them out, and Tesla would have lost $97 million in Q3. Indeed, back them out and… “TSLA hasn’t been profitable …since 3Q19.”

Of course, Tesla is famously viewed by investors as a growth stock. So isn’t it possible Tesla can just grow its way out of this problem? Sell more cars, and become so profitable that it no longer needs ZEVs?

Maybe. But Johnson isn’t optimistic.

From Q2 2020 to Q3 2020, Tesla has grown its ability to produce cars to a stated capacity of 840,000 vehicles per year. Despite the added capacity, however, Tesla is only predicting that it might sell 500,000 cars this year. This seems to speak to a lack of demand for the product even at present production levels, and in Johnson’s view, this lack of demand explains why Tesla has cut its prices “now 13 times in 2020 alone.”

Conclusion: Johnson disagrees with those who call Tesla “fairly valued” or even “undervalued” at its current P/E of more than 1,000 times trailing earnings. The analyst rates Tesla stock a sell, and continues to predict a 90% share price decline. (To watch Johnson’s track record, click here)

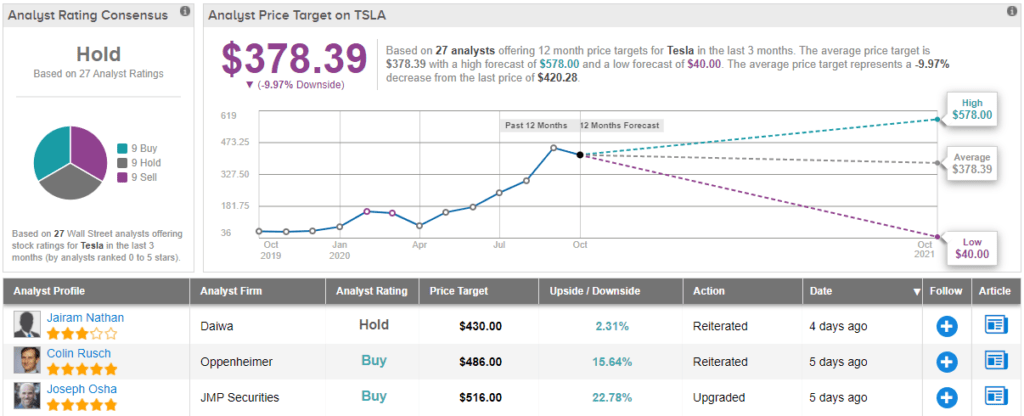

Overall, Wall Street is not as bearish on TSLA as Johnson, but is not convinced on this stock, either. TSLA holds a Moderate Buy from the analyst consensus, based on 9 “buy” ratings – but also 9 “holds” and 9 “sells.” Shares sell for $420.28, and the $378.39 average price target suggests a 10% downside from current levels. (See TSLA stock analysis on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.