Tesla’s (TSLA) stock has been on a wild ride, and shareholders are getting nervous. After surging in late 2023 following Donald Trump’s election win, shares are now hovering 42% below their December highs. The sell-off has been fueled by a flurry of Elon Musk’s controversies, weakening demand in Europe, and renewed concerns about Tesla’s bloated valuation. However, with Elon Musk’s ambitious targets being actively pursued, 2025 is set to be a blockbuster year for the tech giant.

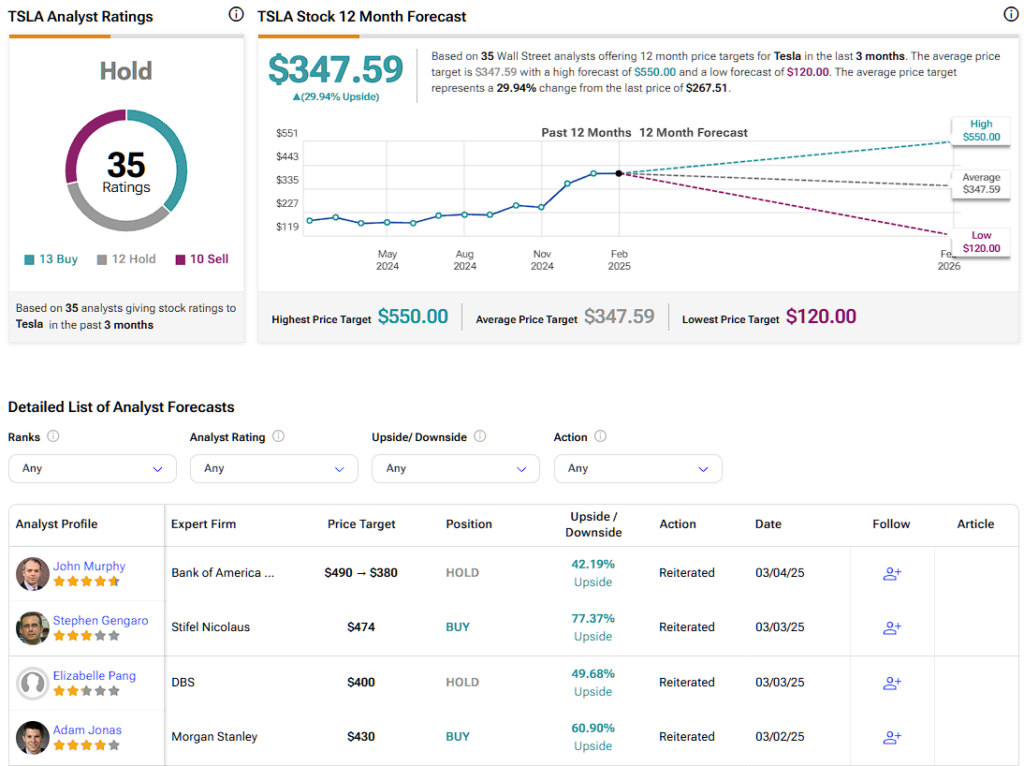

However, while these factors have strained the stock, I believe Tesla’s long-term story remains compelling. If you are willing to look beyond short-term volatility, there are still compelling reasons to stay bullish. That’s the view of several top-tier market analysts on Wall Street, including John Murphy from Bank of America and Elizabeth Pang from DBS—both of whom reiterated their Hold ratings on TSLA stock this week while forecasting in excess of 40% upside for the stock over the coming 12 months.

Elon Musk’s Polarizing Persona Spooks Wall Street

Elon Musk may be a gifted visionary, but his unpredictable behavior has hurt Tesla’s public image and, arguably, the company’s share price. His political comments, controversial posts on X, and ongoing regulatory scrutiny have alienated both customers and investors. To back this up, a recent survey found that 59% of British EV buyers said Musk’s actions would make them reconsider a Tesla. While Tesla remains dominant, its brand loyalty has taken a hit, creating uncertainty for long-term investors.

Another key factor is that while Tesla continues to dominate in the U.S. and China, Europe has been a far tougher battlefield. Tesla’s sales have slumped in some key markets even as general demand for EVs has grown, which is highly discouraging. The competition is heating up, as Volkswagen, BYD, and BMW are launching new EVs at competitive price points, grabbing Tesla’s market share. Tesla’s Model Y is still a top seller, but with over 130 new EV models available in Europe, the days of Tesla dominating unchallenged are over.

Valuation and Margin Concerns

Tesla’s valuation has long been a lightning rod, and with growth slowing, many wonder if it still justifies a sky-high multiple. Price cuts intended to stimulate demand have weighed on margins, which dropped to 16.3% in Q4, shaking investor confidence. Tesla still enjoys a cost advantage over competitors. Still, if margins keep shrinking, investors may struggle to justify Tesla trading at 100x this year’s expected earnings (even after its stock slump).

Four Reasons Why TSLA Bulls Should Stay Bullish

Possibly the leading factor behind TSLA’s bullish case is the company’s full self-driving (FSD) software, which is now a market reality. For several years, naysayers refused to believe TSLA could achieve the feat of automating all car journeys. Now that TSLA has executed its ambitions in reality, the EV giant has logged over three billion miles on FSD, and Musk has announced plans to launch a paid robotaxi service in Austin, Texas, later this year.

If Tesla successfully deploys a robotaxi network, it could unlock a multi-billion-dollar market comparable to Uber without paying human drivers. Musk has even claimed Tesla’s fleet could eventually generate more profit from autonomy than from selling cars. While skeptics remain (myself included), FSD is making headway that tops expectations and the revenue potential is massive.

Energy Storage is Booming

Tesla’s ambitions stretch beyond cars. Its energy arm (especially its utility-scale battery storage) has been registering rapid growth lately. Megapacks command long waitlists, and new factories are being built to meet surging demand. In Q4, energy storage deployments surged 244% year-over-year, setting new records.

Tesla’s Megapacks (large-scale battery storage for utilities) are in extreme demand, with a backlog stretching over a year. With the company accelerating production, this segment could become a major growth driver. As the world shifts to renewable energy, Tesla’s ability to provide grid-scale storage gives it a unique edge that most automakers don’t have.

TSLA’s New EV Models

Tesla’s bread-and-butter, EV cars, is also making progress. TSLA’s glitziest new product, the Cybertruck, has been on the market for a while and performing well. But what’s even more exciting is Tesla’s plan for a more affordable EV. Musk has hinted at a new platform that could cut production costs in half, aiming for a retail price between $25,000 and $30,000 for an upcoming mid-range model.

If Tesla succeeds, it will attract a whole new crowd of buyers and really push electric cars into the mainstream. Meanwhile, Tesla’s new Texas, Germany, and Mexico factories are kicking into gear, helping the company ramp up production and cut costs.

TSLA’s Robotics Wildcard

Tesla’s most significant long-term opportunity, and its most speculative, is not cars but robots. The company’s Optimus humanoid robot seems to be progressing faster than most analysts expected. Musk has suggested that Tesla could deploy 10,000 Optimus robots by next year to handle repetitive factory tasks.

If Tesla can monetize its robotics angle, the competitive moat will be wide and clear for years. Musk has even hinted that Optimus could become a more significant business unit than EV, with applications in warehousing, manufacturing, logistics, and the list could go on. Of course, it’s still early days. But if you take a step back, it’s fair to argue that Tesla is in an excellent position to make this a reality, thanks to its AI and cutting-edge battery technology expertise.

Is Tesla a Buy, Sell, or Hold?

Wall Street analysts have mixed feelings about TSLA stock, with Tesla featuring a Hold consensus rating. This comprises 13 Buy, 12 Hold, and 10 Sell ratings assigned in the past three months. Tesla’s average price target of $347.59 per share suggests a potential 30% upside over the coming twelve months.

As Tesla’s Challenges Mount, Innovation the EV Maker Raceworthy

Tesla’s recent slump reflects tangible challenges from Musk’s unpredictable public persona to intensifying European competition and valuation debates. Yet, after years of observing Tesla’s evolution, I’ve repeatedly seen the company overcome obstacles. Whether it was “production hell” with the Model 3 or skepticism around the Model S, Tesla has a track record of pushing beyond boundaries and making it stick by consolidating.

That doesn’t mean it’s smooth sailing ahead. Musk’s controversial remarks won’t vanish, and European/Chinese automakers are only growing more capable. Still, the stock remains a compelling bet for those who believe in Tesla’s innovation capacity and can handle the inevitable ups and downs. With fresh models, a surging energy division, and AI and robotics ambitions, Tesla stands out as a driving force in an industry undergoing radical transformation.