“Can trees grow to the sky?” is a question that Palantir Technologies (PLTR) investors might ask themselves, given the AI software company’s continued impressive performance over the past year without showing any bullish fatigue.

The buzz in the markets is that Palantir stock is unstoppable. After the company delivered a strong Q4 report last week, beating expectations across the board and providing robust guidance again, the stock has surged more than 30% since then.

In fact, Palantir stock has seen a breathtaking 342% increase over the past 12 months. While this rapid rise has stretched its valuation, I still maintain a bullish view, given that Palantir is perfectly positioned at the center of the AI revolution—which is still in its early innings.

Considering the company’s recent developments, there’s plenty more room for upside in Palantir stock, even with seemingly high multiples.

Can PLTR Hit $100 Per Share?

Given the Q4 results, the answer is a tentative yes. The AI software darling Palantir delivered another blowout quarter, with earnings per share coming in at $0.14—beating estimates by $0.03—and revenues hitting $827.52 million, which was $51 million above expectations.

The most significant growth driver was the U.S. commercial segment, which had its strongest quarter yet, posting $83 million in revenue—a 134% year-over-year increase. The total remaining deal value in the U.S. commercial business (i.e., closed contracts yet to be converted into revenue) grew by 99% year-over-year, up 47% from the previous quarter, and the number of customers grew by 73% year-over-year.

On the consolidated side, Palantir ended Q4 with $5.4 billion in total remaining deal value, up 40% from last year and 20% from the previous quarter. Remaining performance obligations stood at $1.73 billion, a 39% year-over-year increase and a 10% increase sequentially. This backlog shows that Palantir is drawing more interest from new customers than it’s fulfilling with existing ones. Revenues are climbing.

In 2024, Palantir ended the year with $2.86 billion in revenues, surpassing its top-end guidance of $2.80 billion, and adjusted income from operations of $1.12 billion, above its highest guidance of $1.05 billion.

Given the company’s outperformance in 2024, analysts now see Palantir’s Q1 2025 guidance as conservative. Palantir expects Q1 to register between $858 million and $862 million in revenue, with analysts revising their expectations upwards to $874 million. Palantir’s management team also expects adjusted income from operations to increase by more than $350 million, with analysts forecasting Q1 EPS of $0.13, a nearly 20% revision above consensus ahead of Q4.

Balance of Growth and Profitability to Catalyze PLTR Stock

Digging deeper into key metrics, the bullishness surrounding Palantir becomes more apparent when you see how the company is managing to grow revenues and margins simultaneously—a rare feat for most companies in their growth stages.

For example, Q4 revenues grew by 36% (with a 6% sequential increase), while adjusted operating margins reached 45%, up from 38% the previous quarter. A standard metric among SaaS (Software as a Service) companies is the Rule of 40, which looks at the balance between growth and profitability. According to this rule, the sum of a company’s revenue growth rate and adjusted operating margin should exceed 40%. In simple terms, if the combined percentage is above this benchmark, the company can remain sustainable even with lower margins as long as it’s growing quickly.

In Palantir’s case, the company’s 36% revenue growth and 45% operating margin in its most recent quarter give it a score of 81%, which is exceptional. For comparison, software giant Microsoft (MSFT) scored 62%, based on its 46% operating margins and 16% revenue growth in its latest quarter.

Maintaining such a high score is tough, but Palantir has increased its Rule of 40 score from 38% in Q2 2023 to 81%. Currently, Palantir could be the SaaS company with the best balance between growth and profitability globally.

PLTR’s Valuation Dilemma

Valuations remain a key point for Palantir skeptics, who argue that the company’s market price doesn’t justify paying 200x forward earnings or 158x forward cash flows. Even if we account for growth, with the projected 25% EPS CAGR over the next five years (which is impressive), that leads to a PEG ratio of 7.8x—a considerable premium compared to other AI leaders like Nvidia (NVDA), which has a PEG of just 1.1x.

That said, Palantir’s valuation multiples have been stretched for a while now, and this isn’t exactly new. If investors had held off on buying Palantir in the past because they thought the premium was unjustifiable, they would have missed out on a big chunk of the considerable gains to date.

Investors should look at what the company has accomplished, and the kind of generational business CEO Alex Karp and Palantir have built. One quote I really agree with when it comes to the valuation debate around Palantir comes from Dan Ives, the perma-bull analyst at Wedbush:

“The transformational tech winners, if you just focus on valuation, you’ve missed all the transformational tech from Apple to Meta to Google to Tesla and others.”

So, following Ives’ line of thinking, looking at the bigger picture in the long term makes more sense than considering whether Palantir can reach $10 billion in revenues or $5 billion in free cash flow over the next three, four or five years.

Where Will Palantir be in 12 Months?

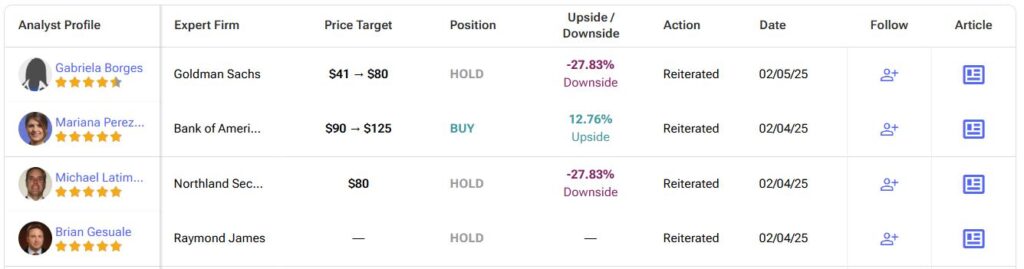

Wall Street isn’t very bullish on Palantir right now. In my view, analysts are overly tentative, given the meteoric rise the stock has endured. Out of 17 analysts covering the stock in the last three months, the consensus rating is a Hold, with only two Buy, ten Hold, and five Sell ratings. The average price target for PLTR stock is $88.60 per share, which suggests a potential downside of 20% from the current share price.

Lukewarm PLTR is Just Getting Started

Palantir is best in class in helping businesses quickly solve complex problems with AI solutions. Recent Q4 results showed no signs of slowing demand for its services. In fact, it was quite the opposite. Demand for AI is climbing, and PLTR is capitalizing. While some bears stay away from the stock due to high valuation multiples and uncertain growth estimates, I believe there’s still plenty of room for Palantir to grow as a transformational tech leader in the long run.