Payments pioneer PayPal Holdings (PYPL) was in rally mode for most of 2024, delivering both price and value for its patient yet loyal shareholders. However, latecomers shouldn’t expect outsized returns, as the stock now trades close to fair value. While I accept that PayPal offers an interesting investment case, the payments giant doesn’t satisfy several key requirements for me to upgrade my bearish outlook. The stock may provide lucrative opportunities for short-term speculators, but I am too long in the tooth to overcommit to a tech company that is still trying to revive market enthusiasm amid a major corporate overhaul aimed at restoring its former dominance.

Confident Investing Starts Here:

- Quickly and easily unpack a company's performance with TipRanks' new KPI Data for smart investment decisions

- Receive undervalued, market resilient stocks straight to you inbox with TipRanks' Smart Value Newsletter

As seasoned tech investors may already know, the payments extraordinaire is currently executing a strategic makeover to enhance profitability and strengthen its position in the fierce digital jungle of payment processing. Something tells me I should take a leaf out of Charlie Munger’s playbook when assessing PayPal’s investment case.

Meet PayPal’s Turnaround Team Driving the Comeback

President and CEO Alex Chriss joined PayPal in September 2023, bringing two decades of experience to steer the company toward innovation and growth. Under his leadership, we’ve seen the introduction of Fastlane—streamlining guest checkouts—and PayPal Ads, which enables merchants to leverage PayPal’s extensive transaction data for targeted marketing.

Alex Chriss isn’t working alone. Mark Grether, Senior Vice President, brings expertise from building Uber’s (UBER) $1 billion advertising business. In addition, Enrique Lores, appointed Chairman in July 2024, brings extensive experience from his tenure as President and CEO of HP (HPQ).

The question is not whether PayPal has talent but whether that talent can continue to drive market-beating returns. After its rampant surge last year, repeating the feat in 2025 is a tough ask.

Slowing Growth and Competitive Pressures Undermine PYPL Stock

PayPal’s growth is slowing, exemplified by its unbranded payment processing segment. In Q4 2024, this segment reported just 2% growth compared to 29% a year earlier. Meanwhile, rivals are catching up. Apple (AAPL) Pay also dominates; it processed a staggering $6 trillion in global payments and generated $1.9 billion in revenue in 2022. As of 2024, Apple Pay serves approximately 640 million users worldwide and is projected to expand to 700 million by 2027. Moreover, perhaps most concerning to PayPal, Apple Pay holds a commanding 54% share of in-store mobile wallet transactions as of 2024, outpacing all other major competitors.

While PayPal may continue to thrive, it is not positioned as a dominant market leader. Therefore, many long-term investors are looking to deploy their cash savings elsewhere now that the stock is trading at a more equitable valuation.

Deflationary Financials Undermine PYPL Stock

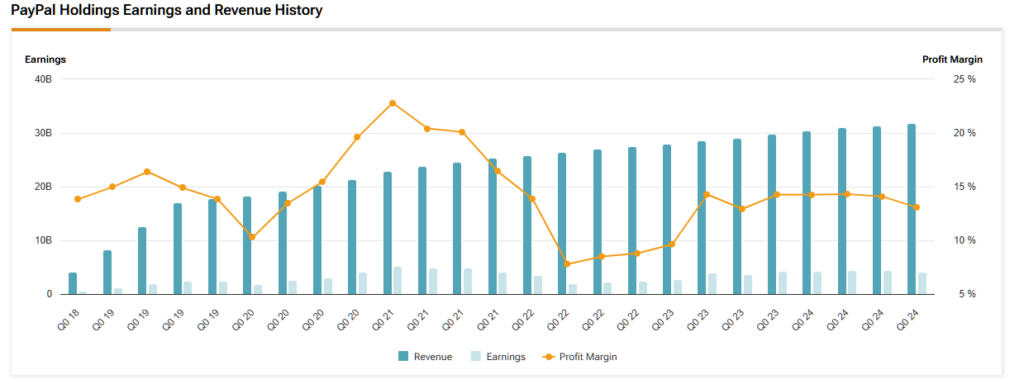

PayPal stock is not exactly geared for growth. Over the last 12 months, the company has delivered only a 6.8% year-over-year revenue growth rate, with earnings per share up just 3.9%. Just because management is revitalizing the business does not mean we can regularly expect double-digit growth in financials—especially in a saturated and fiercely competitive market.

Investors secured strong returns over the past 12 months because the company was previously undervalued. When the market recognized this discrepancy upon management’s turnaround, the valuation was adjusted to more accurately reflect the financials.

With a price-to-sales ratio of 2.5—lower than the sector median of 3—and revenue growth exceeding the sector median of 6%, there appears to be some upside for value investors. However, profitability concerns weigh on the outlook. The company’s price-to-earnings ratio stands at 16, compared with a sector median of 12, and earnings growth is just 4% year-over-year versus 6% for the sector. Given these financials, I am not a buyer of PayPal stock at today’s valuation.

However, management has recently addressed growing concerns about profitability. It expects low teens+ non-GAAP earnings per share growth by 2027 and strives for 20%+ earnings per share growth in the long term. However, this is some way off, and I’m looking for a little more evidence in the near term before I’d be happy to pull the trigger on PayPal stock as a medium-term or long-term holding.

Short-Term Volatility Means Opportunity

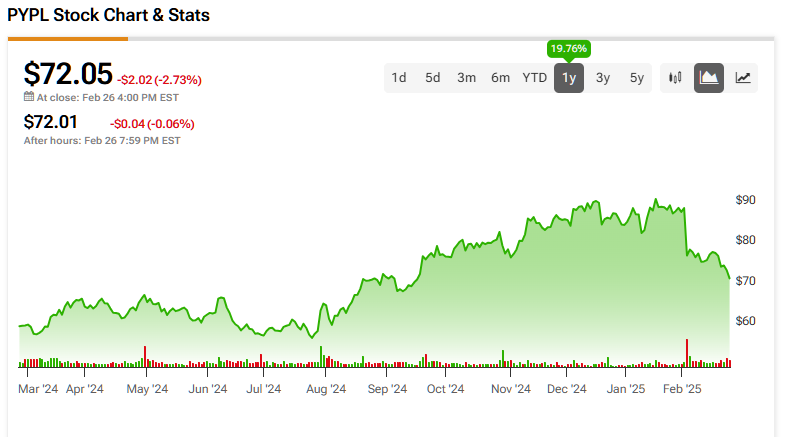

From a technical standpoint, this is not the worst short-term entry point for a trade. However, long-term value investors like myself, who seek investments with more sustained upside, are unlikely to buy at current levels. The weekly chart shows the 14-week Relative Strength Index (RSI) at approximately 40. While this indicates weakness and relatively good value, it is not the ideal entry point—my view is that an RSI below 30 would be preferable.

Looking at the daily chart, there appears to be slightly more opportunity. The 14-day RSI is just over 30, suggesting that buying now may offer substantial short-term upside. However, as with many short-term trades, I would only hold the stock for a few months until the RSI reaches 60–70; at this point, I would sell and redeploy my capital into other, more lucrative, long-term investments. That’s unless those double-digit earnings growth rates start to become more tenable, of course.

Is PayPal a Buy, Sell, or Hold?

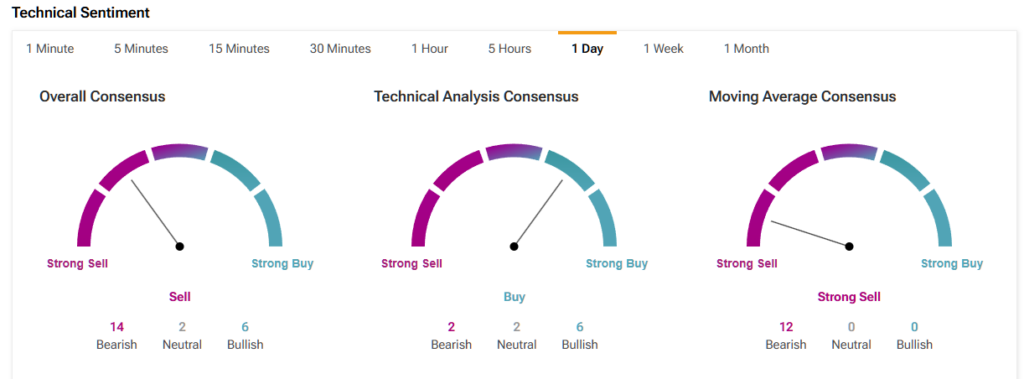

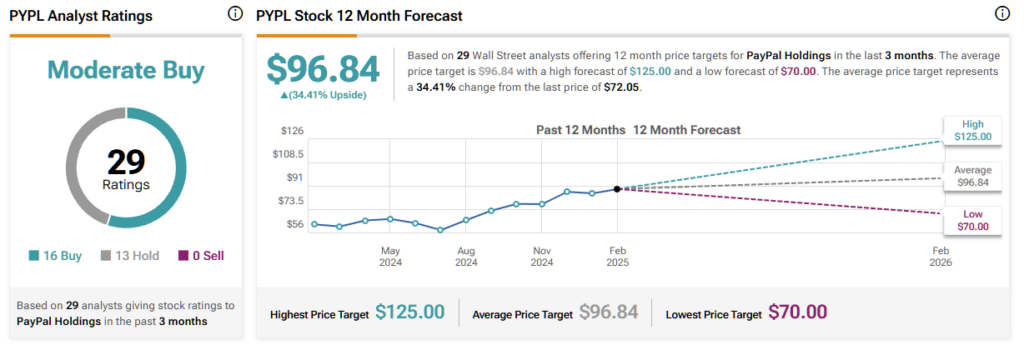

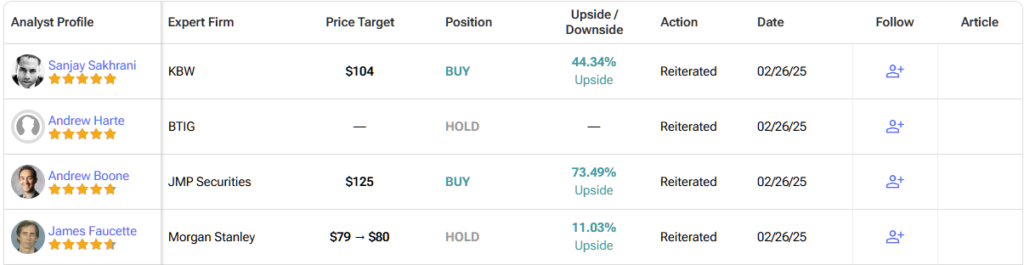

On Wall Street, PayPal holds a consensus Moderate Buy rating based on 16 Buy, 13 Hold, and zero Sell ratings over the past three months. The average PYPL price target of $96.84 suggests a 35% upside potential over the coming year. This indicates that the stock is still positioned opportunistically; however, as I mentioned, this upside is unlikely to persist and is vulnerable to shifts in sentiment due to weaknesses in the stock’s financials relative to the broader sector.

PayPal Isn’t the Only Fish in the Payments Ocean

While PayPal offers exposure to a reasonable valuation and boasts a strong management team working diligently to help shareholders thrive, its return prospects are hindered by moderate financial growth for now. Although PayPal stock might be a good buy over the next few months based on technical indicators and sentiment, this approach remains risky and most suitable for investors with a strong risk appetite only.

I prefer strong sentiment indicators, robust and expanding growth rates, and an expansive market opportunity with an enduring competitive moat. PayPal falls short of being one of the best-in-class stocks I typically invest in. Maybe famous wealth manager Charlie Munger says it best: “The big money is not in the buying and selling, but in the waiting.”