Today was a big day for discount bulk retailer Costco (NASDAQ: COST). The company announced Q4-2022 earnings, and the results were solid all around. Oddly enough, they weren’t sufficiently solid to keep investors happy. The company is down modestly in after-hours trading. Investors were apparently irked by how narrow, overall, the win was.

Confident Investing Starts Here:

- Quickly and easily unpack a company's performance with TipRanks' new KPI Data for smart investment decisions

- Receive undervalued, market resilient stocks straight to you inbox with TipRanks' Smart Value Newsletter

TipRanks estimates looked for Costco to turn in earnings of $4.17 per share. Costco beat that figure, coming in with $4.20 per share. Costco also posted a win on revenue, posting $72.09 billion in revenue against estimates calling for $71.84 billion.

Though Costco’s win was far from a blowout, it was a win nonetheless. Better yet, Costco has an excellent value proposition that should not only keep shoppers coming back but also keep investors happy. They may not seem all that happy about Costco’s narrow win, but a win is a win, and that kind of winning helps keep me bullish on Costco.

The last 12 months for Costco shares have been extremely volatile, with three major run-ups followed by three major declines. Costco shares reached peaks in January, April, and August before backtracking on each peak. Currently, Costco is off its August peak, dropping from around $560 per share to just under $475 in after-hours trading.

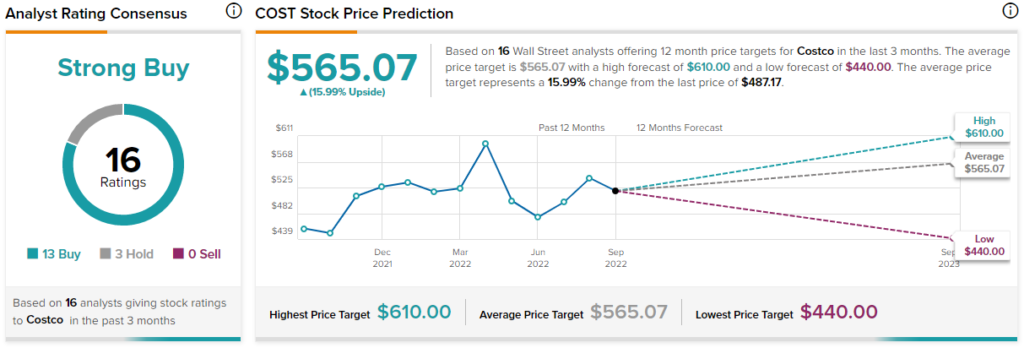

What is the Prediction for COST Stock?

Turning to Wall Street, Costco has a Strong Buy consensus rating. That’s based on 13 Buys and three Holds assigned in the past three months. The average Costco price target of $565.07 implies 16% upside potential from its closing price of $487.17.

Analyst price targets range from a low of $440 per share to a high of $565 per share.

Costco’s Investor Sentiment is a Mixed Picture

There are parts of investor sentiment right now that couldn’t look much better. Other parts, meanwhile, are a disaster in the making. Two metrics will demonstrate that dichotomy nicely.

First, Costco has a ‘Perfect 10’ Smart Score on TipRanks. That’s the highest score a stock can get and the highest level of “outperform.” Clearly, expectations are high for Costco to ultimately outperform the market.

Costco’s insiders, however, are absolutely not convinced. In both the aggregate and in informative selling and buying, insider trading at Costco is very much Sell-weighted. In the last three months, Costco’s corporate insiders sold $2.6 million worth of stock. As for the aggregate figures, insiders staged 11 Sell transactions to seven Buy transactions, demonstrating a clear interest in selling.

Meanwhile, the last 12 months also demonstrate a lack of support from Costco insiders. While insiders bought Costco shares 22 times in the last 12 months, they sold them 30 times.

A Down Retail Market, but Likely Less Down at Costco

Make no mistake: Costco will suffer as part of an overall economic downturn. Virtually all retailers will. That’s just how an economic downturn hits things. However, Costco will likely be spared the worst of an economic downturn just by the nature of its operations.

Since Costco focuses on necessities—food, toiletries, and so on—it’s likely to see less damage. Of course, people will scale back on some things. They’ll buy less of some foods. They’ll step down a bit in the quality of their toiletries. Still, it’s a safe bet that people will buy food. If people ever stopped buying food, we’d have much, much bigger problems than Costco’s earnings report.

Further, Costco has an unusual value proposition: its bulk sales. This leaves it with few competitors, chief among which is Walmart (NYSE: WMT) and its Sam’s Club imprint. There are a few others, of course, though all are significantly smaller than Walmart.

There are also some signs that Sam’s Club may have the edge in discount pricing as well. A recent Yahoo Finance study found an array of fall-friendly treats that were cheaper at Sam’s Club.

Costco made a particular name for itself during the pandemic as a “stock-up” point. People could buy in large quantities at reasonable prices so they wouldn’t have to leave the house so often. Though the prices have likely increased, and some things are just unavailable, it’s a safe bet that people will still buy in bulk just to outwit the next wave of shortages.

Costco also offers an unexpected range of luxury goods. Are you interested in a nearly-$50,000 wedding ring? You can get it at Costco. A $20,000 golf simulator? Ditto. Costco could make a play to be the staycation experts as well as a stock-up alternative par excellence.

So, there’s a nice formula at work for Costco. Take Costco’s established presence as a means to potentially get out in front of future price hikes. Then, add it to Costco’s potential to upgrade home spaces in place of a vacation, and suddenly, the company looks pretty sharp.

There were some rumors of potential membership price hikes, but current reports suggest those aren’t likely to go through.

Count that as further good news; if Costco did hike prices, it would have to work that much harder to pull in potentially interested customers. While Costco has a solid value proposition behind it, forcing customers to pay more for access to deals really only works as long as you’re a clear winner on prices.

Conclusion: Options and Macroeconomics Could Work for Costco

There’s no doubt that Costco will suffer in the short term. Almost every retail operation will. Nonetheless, since Costco customers tend to be higher-income shoppers, an economic downturn will commonly hit them less.

It’s already a haven for bulk buyers and those who want to fill their basements with supplies ahead of a potential job loss or the like. Now, it can make a case as a money-saving alternative to travel, which will likely be welcome by more people in the near future.

Throw in the fact that Costco stock is already attractively-priced, and that only makes it better. It’s selling much closer to its lowest targets than its average, which offers plenty of upside potential. The losses today help make for a sound buy-in point for those interested in owning a piece of the bulk retailer.

The end result is an extremely attractive stock with multiple value propositions. Is it any wonder I’m bullish on Costco, which will likely be one of the last retailers hurt by a serious economic downturn?