Banco BBVA Argentina (BBAR) stock has exploded 670% over the past three years. Fueled by President Javier Milei’s sweeping reforms enacted in 2023, Argentine businesses are thriving again following multiple grueling recessions that left Argentina on its knees. Amid the macroeconomic renaissance, BBAR is a banking stock that has benefitted dramatically from renewed confidence, improved capital flows, and foreign investment. Morgan Stanley has a $27 price target on BBAR and expects a 42% further upside before the end of this year, indicating that BBAR stock is currently bathed in bullish sentiment.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

However, the impressive surge in its share price comes with high valuation multiples and inherent risks in the Argentine economic landscape. I’m concerned that the stock has gone too high too quickly, leaving BBAR overpriced — even with its $1.4 billion war chest of cash reserves. Meanwhile, Argentina as a nation remains an inherently risky prospect, with inflation still elevated following several recessions that are still taking their toll and mass privatizations that could yet include the country’s national bank.

As a result, I remain bearish on BBAR despite all its plaudits.

Why BBAR Has Picked Up So Much Momentum

BBVA Argentina’s surge can largely be attributed to a confluence of strong financial fundamentals, favorable market dynamics, and earnings growth. The primary driver is a sudden surge in Argentina’s economic recovery under President Javier Milei’s pro-business policies. Milei’s reforms, including cutting public spending, reducing taxes, and stabilizing the Argentinian Peso, have led to a dramatic improvement in Argentina’s economy, including core sectors like banking, construction, and defense. This positive economic environment has created fertile ground for BBVA Argentina to thrive and expand its operations.

The bank’s financial performance has been particularly noteworthy. In 2024, BBVA Argentina posted a net attributable profit of ARS 99.2 billion in the third quarter, representing a staggering 224.8% increase compared to the same period in 2023. This exceptional growth in profitability has been accompanied by substantial increases in loans and deposits, as well as a reduction in non-performing loans, indicating a strong foundation for future growth.

In broad terms, Argentina’s GDP is expected to rebound by 5.5% in 2025, driven by private consumption and investment. This economic resurgence will likely increase demand for banking services, further bolstering BBVA Argentina’s growth prospects.

Banco BBVA’s Valuation Demands Caution

Despite the impressive surge in BBVA Argentina’s performance and stock price, there are concerns that the valuation may be running too high. The bank’s current price-to-earnings (P/E) ratio is 19.8x, 57.3% higher than the sector median of 12.6x. This significant premium suggests investors may be overly optimistic about the bank’s future prospects.

Moreover, when compared to its own historical valuation, BBVA Argentina’s current P/E ratio is 306.9% higher than its 5-year average of 4.8x. This dramatic increase in valuation multiples raises questions about the sustainability of the current stock price levels. Additionally, the stock’s forward P/E ratio, based on estimated earnings for 2024, is 15x, which is still 28.9% higher than the sector median. While this indicates some expected moderation in the valuation, it remains elevated compared to industry peers.

The significant divergence between BBVA Argentina’s current valuation and its historical averages and sector benchmarks suggests that investors should approach the stock cautiously. Given the strong run-up to current price levels, there may be limited upside potential.

Moreover, with Milei’s Argentina open for business and the privatization of public sector assets becoming routine, competition within Argentina’s banking sector is already heating up. Just recently, Milei signed a decree to privatize Argentina’s largest bank, Banco Nación, indicating that BBAR may be more challenged in attracting customers and investors than first thought.

Microeconomic Stumbling Blocks for BBVA

The bank’s net interest income declined by 39.5% in Q3 2024 to ARS 460.3 billion, a steeper drop than the 1.5% decrease seen in Q2. This significant decline can be attributed to lower interest income, which fell by 30.3% quarter-over-quarter to ARS 760.2 billion.

Likewise, the bank’s efficiency ratio deteriorated further in Q3 2024, reaching 59.7%, up from 55.3% in Q2. This increase indicates a worsening cost-to-income ratio, potentially signaling operational challenges. Top-performing banks aim to keep their ratio under 60%, ideally below 50%. Compared to competitors like Banco Macro (BMA), which maintains an adjusted efficiency ratio of around 30%, BBVA Argentina’s performance appears less favorable.

According to the company’s latest figures, BBVA Argentina’s return on equity (ROE), a key profitability metric, stands at 16.9%. While this outperforms some top-tier European banks—a positive sign—it falls short of the 27% average among its Argentine peers, which is a concern. This gap, combined with a rising efficiency ratio, indicates potential challenges for BBAR in sustaining profitability and operational efficiency amid the current economic climate.

Is Banco BBVA a Good Stock to Buy?

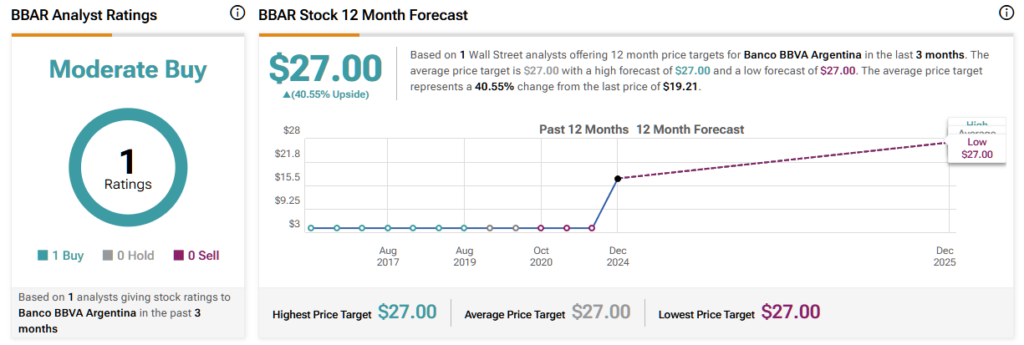

On TipRanks, BBAR is covered by one analyst: Jorge Kuri from Morgan Stanley. In December 2024, Kuri rated Banco Argentina as a Moderate Buy with an accompanying price target of $27 per share. With BBAR’s stock price roughly the same then as it is now, Kuri’s forecast targets a 40% upside for BBAR stock over the next 12 months.

BBVA Argentina Flies Too High

I’m bearish on BBVA Argentina at its current valuation. While the bank has delivered outstanding financial performance, its valuation multiples appear stretched, trading well above historical and sector averages. The root cause for BBAR’s rapid resurgence has undoubtedly been political change and the pro-business policies and reforms enacted by the country’s charismatic new President, Javier Milei.

Those reforms have also enabled greater competition, especially in banking, which means companies like BBAR must fend off more rivals to stay competitive. In the first stages of mass privatization, almost everyone benefits. But after a while, when competition becomes fierce and margins are compressed, only the efficient firms remain.

Argentina’s economic resurgence is promising, but the reemergence of capital flight and inflation. Meanwhile, BBAR’s metrics are relatively good compared to foreign banks but relatively bad compared to domestic peers like Banco Marco, which suggests its current market position is overvalued.