Advanced Micro Devices (AMD) shares have underperformed in recent months — partly because earnings haven’t smashed investor expectations like Nvidia (NVDA) regularly does. The Californian semiconductor giant has been operating well and truly in the shadow of its larger peer. NVDA’s leading position and relative strength have ensured its share price has grossly outperformed AMD’s. NVDA stock is up around 83% over the past 12 months, while AMD’s has sunk 35%.

However, the market overlooks many of AMD’s achievements and fundamental strengths. This is reflected by the company’s attractive price-to-earnings-to-growth (PEG) ratio of 0.53 — a valuation metric determining whether a stock is undervalued by factoring in the company’s earnings growth. A PEG ratio below 1 suggests AMD is undervalued relative to its growth potential.

Once all the relevant factors are considered, AMD may be the better stock pick for avid tech investors looking to back one of these global graphics giants. In fact, Wall St. analysts forecast similar degrees of upside for both companies in 2025.

The DeepSeek Selloff is Overdone

First, addressing the recent selloff in Western tech companies, especially those with exposure to AI development, is essential. According to various market commentators, DeepSeek represents an existential threat to the U.S. tech sector. Suppose a Chinese research lab can deliver a much cheaper large-language model (LLM) for artificial intelligence (AI) than Western rivals. In that case, the future outlook for companies like AMD, NVDA, and Intel (INTC) is somewhat bleak.

However, there are several reasons to believe that the market’s reaction is overblown due to three key misunderstandings. One of which is the economics of training versus inference. DeepSeek R1’s touted $5.6M training cost excludes critical R&D expenses like architecture experimentation, algorithm tuning, and pre-training infrastructure. While this reduces upfront training barriers, inference demands remain GPU/TPU-intensive. For example, R1 requires ~37GB RAM per billion parameters, necessitating high-performance hardware like AMD’s MI300 (384GB HBM3 memory, 5.3TB/s bandwidth).

Then, there’s AMD’s inference advantage. AMD’s MI300 has 1.8x higher memory bandwidth than Nvidia H100, making it ideal for inference workloads, with FireAttention V3 benchmarks showing AMD GPUs achieving 1.4–1.8x better throughput for models like LLaMA 70B. DeepSeek supports AMD consumer GPUs (RX 7000 series) and Ryzen AI CPUs, signaling long-term hardware reliance.

Finally, investors need to consider market misalignment, in that the selloff assumes DeepSeek’s AI progress reduces hardware demand, but inference scalability drives chip demand more than training. In fact, given AMD’s competitive positioning within inference-specific optimizations, the Santa Clara firm could benefit from R1’s proliferation.

AMD’s Incremental Gains

My bullishness is also bolstered by AMD’s meaningful market share gains in critical sectors, particularly within the AI and data center markets. The company’s data center revenue surged 69% YoY to $3.86 billion in Q4 2024, driven by fifth-gen EPYC Turin processors now holding over 50% share at major hyperscalers. While this trails Nvidia’s AI dominance, AMD’s MI300 series GPUs are gaining traction, with cloud providers deploying them for training and inference workloads—supported by $5 billion in 2024 AI revenue.

In the AI GPU market, AMD’s Instinct MI325X (launching Q1 2025) and accelerated MI350 series aim to capture a 5% market share by late 2025, which Baird projects could drive 25% YoY revenue growth. Though Nvidia’s software ecosystem remains superior, AMD’s 1.8x memory bandwidth advantage in MI300 GPUs positions it as a cost-effective inference alternative, with FireAttention V3 benchmarks showing competitive throughput.

Most recent earnings results show AMD’s client segment also advancing, with Ryzen CPU revenue up 58% YoY as PC market share climbed. However, gaming (-59% sales) and embedded (-13%) segments lag, highlighting uneven progress.

However, analysts note AMD’s 2025 AI growth hinges on MI350 adoption and software maturation. While unlikely to dethrone Nvidia, AMD’s diversified AI-CPU strategy and $7.1 billion Q1 2025 revenue guidance suggest incremental gains as enterprises prioritize cost-efficient, hybrid-computer solutions.

AMD’s Valuation is Highly Enticing

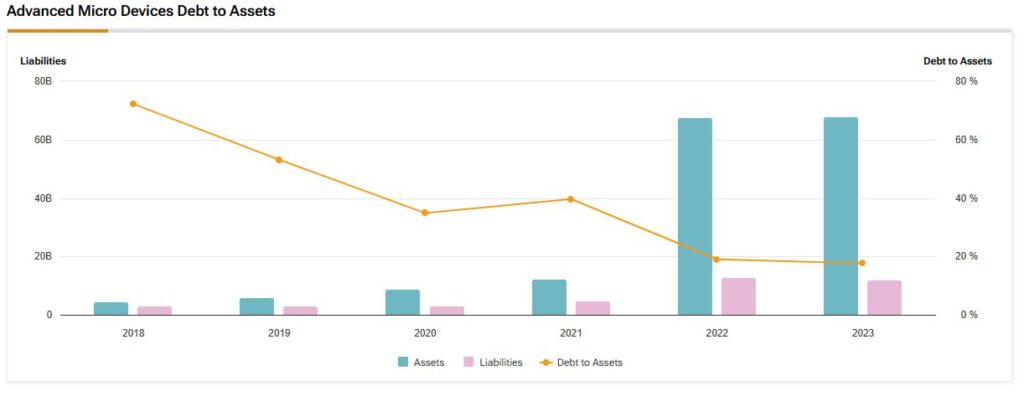

At current prices, AMD’s valuation looks very attractive. The company’s financial position remains robust, with a net cash position of $2.8 billion, providing flexibility for future investments and growth initiatives. Meanwhile, the company’s forward price-to-earnings (P/E) ratios indicate an intriguing trajectory being forecast by AMD’s management, falling from 22.7x this year to around 11x by 2028.

This downward trend indicates strong earnings growth expectations. Compared to the sector median forward P/E of 25.50x, AMD’s 2025 forward P/E of 22.66x represents an 11.13% discount, suggesting undervaluation relative to peers despite this impressive growth rate.

The price-to-earnings-to-growth (PEG) ratio, a key valuation metric considering growth, also stands out. AMD’s forward PEG is an impressive 0.53, significantly below the sector median of 1.83 (-71.1% difference), indicating that AMD’s stock is potentially undervalued given its growth prospects.

Is AMD a Good Long-Term Investment?

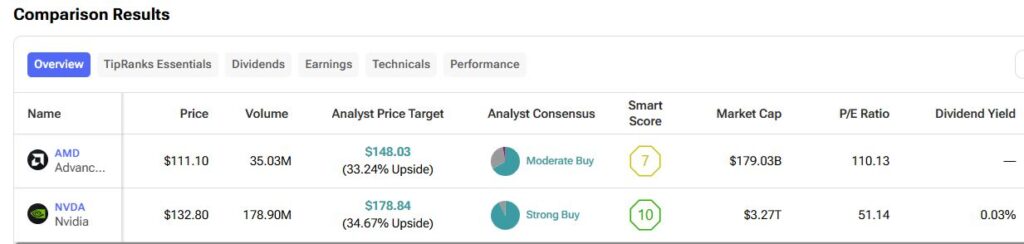

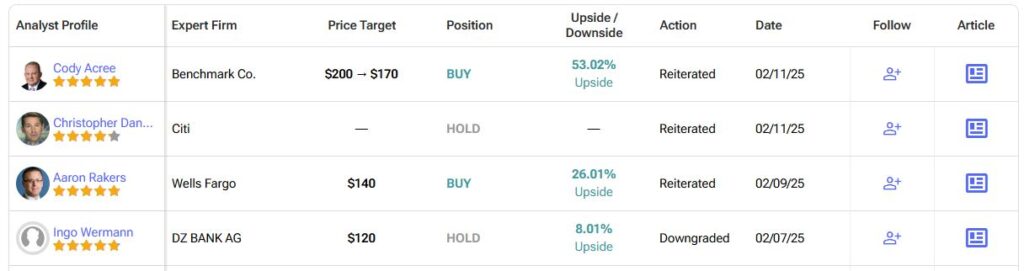

On Wall Street, AMD stock carries a Moderate Buy consensus rating based on 24 Buy, 11 Hold, and one Sell rating over the past three months. AMD’s average price target of $148.03 per share implies a 33% upside potential compared to current levels.

AMD is Set to Outshine Intel in 2025

I’m bullish on AMD because the recent selloff seems excessive, while its long-term growth prospects remain strong. The company’s momentum in AI and data centers and attractive valuation—especially a low PEG ratio of 0.53—points to significant upside potential.

Although Nvidia leads the market, AMD’s MI300 GPUs are making strong progress and winning over customers, albeit gradually. Meanwhile, AMD’s diversified strategy adds stability. With analysts forecasting strong earnings growth and price targets around $150 per share in 2025, AMD appears well-positioned for a revaluation as market sentiment improves.

Questions or Comments about the article? Write to editor@tipranks.com