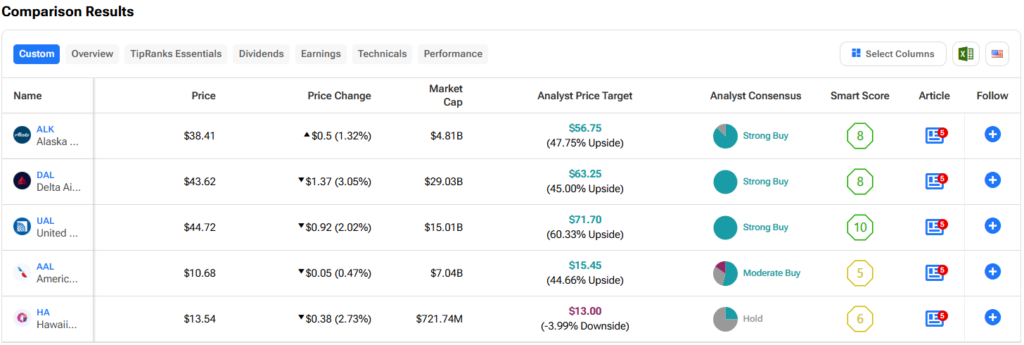

Alaska Air Group (NYSE:ALK) stands out in the airline industry as a U.S. legacy carrier with the cost structure of a low-cost airline. The airline’s robust balance sheet with low leverage positions it well for strategic acquisitions like Hawaiian Holdings (NASDAQ:HA), which is why I’m bullish on ALK. These factors combined suggest that the stock could surge over 47%, according to Wall Street consensus.

Don't Miss our Black Friday Offers:

- Unlock your investing potential with TipRanks Premium - Now At 40% OFF!

- Make smarter investments with weekly expert stock picks from the Smart Investor Newsletter

Despite recent underperformance, largely attributed to operational issues beyond its control, I anticipate a strong Q2 for Alaska Air, with the Hawaiian Airlines acquisition serving as a short-term catalyst.

Factors Leading to ALK’s Underperformance

Alaska Air stock has underperformed most U.S. legacy airlines over the last 12 months, with a devaluation of more than 32%. Despite this, its performance this year has been relatively stable, declining by 2.5%.

In my opinion, the main reasons behind this underperformance could be related to the following:

- The grounding of the Boeing 737 MAX 9 fleet after a mid-air incident in January lasted until February, affecting 65 of Alaska Air’s Boeing 737 aircraft. This led to significant operational disruptions and financial losses ($132 million in net losses in Q1), despite Boeing (NYSE:BA) compensating Alaska Air with $162 million.

- Financial struggles were exacerbated by fluctuating fuel costs and varying demand for air travel. Alaska Air pays higher fuel costs than average due to its West Coast operations.

- Labor costs increased in Q1 due to new labor agreements, including substantial pay raises for the crew.

- Uncertainties surrounding the acquisition of Hawaiian Airlines and regulatory challenges have further dampened Alaska Air’s stock performance in recent months.

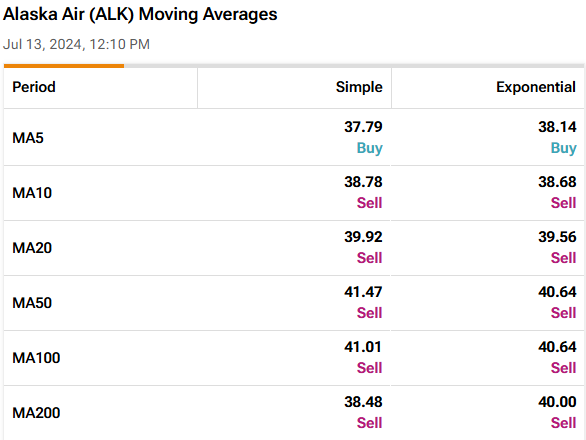

Taking a quick peek at ALK stock’s technical setup, ALK is currently trading below all significant moving averages. This typically suggests it’s near or below its support levels and encountering resistance. In simpler terms, the 50-day, 100-day, and 200-day simple moving averages are at $41.47, $41.01, and $38.48, respectively. These levels could act as barriers that the stock needs to surpass to signal a potential turnaround or upward momentum.

However, the green light from the U.S. Department of Justice (DOJ) for the acquisition of Hawaiian Airlines could serve as a significant short-term catalyst for the stock to break this resistance.

Alaska Air’s Business Fundamentals

When we dig into Alaska Air’s fundamentals, we see that despite being a legacy airline, it operates with a typical low-cost carrier cost structure.

Taking a look at the CASM-ex metric, which measures operating costs per available mile excluding fuel and specials, gives us a clearer picture of the airline’s performance independent of fuel costs, which are not within its control.

Throughout 2023, Alaska Air reported a CASM-ex of 10.14 cents. These operational costs were lower than those reported by the big three legacy U.S. airlines last year: Delta Air Lines (NYSE:DAL) reported 13.17 cents, United (NASDAQ:UAL) 12.03 cents, and American Airlines (NASDAQ:AAL) 13.15 cents. They were also lower than the largest U.S. low-cost carrier, Southwest Airlines (NYSE:LUV), which reported a CASM-ex of 11.08 cents last year.

Alaska Air’s ability to control operating costs can be attributed to its efficient fleet of Boeing 737s and Embraer 175s. These aircraft are known for their above-average fuel efficiency and lower maintenance costs. Another key factor is Alaska’s focus on point-to-point routes, which eliminates the need for centralized hubs and improves aircraft utilization rates.

One of Alaska Air’s main competitive advantages over its U.S. legacy peers is its limited competition on its routes, particularly in the Pacific Northwest. This advantage is expected to strengthen with the completion of the acquisition of Hawaiian Airlines, which will solidify Alaska Air’s prominent position in West Coast routes.

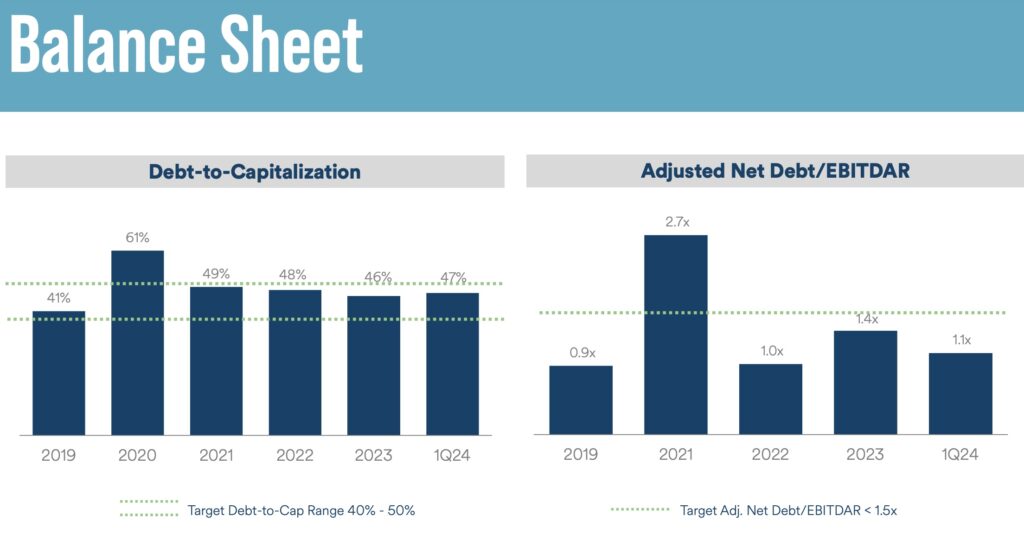

Alaska’s strong balance sheet supports this acquisition. The airline’s net leverage (adjusted net debt/EBITDAR where “R” stands for rent) is currently at just 1.1x, indicating a robust financial position compared to its peers. This demonstrates a solid financial foundation and room for strategic expansions like acquisitions.

Interestingly, despite recent fluctuations in Alaska’s stock price, its multiples valuation appears attractive to me. ALK trades at a forward P/E ratio of 8x, which is 20% below its five-year average. While it trades at a premium compared to the big three legacy U.S. peers (and twice that of United), I believe this premium is justified by ALK’s strong balance sheet and cost structure, which align more closely with that of a low-cost carrier.

What to Expect for Q2 Earnings

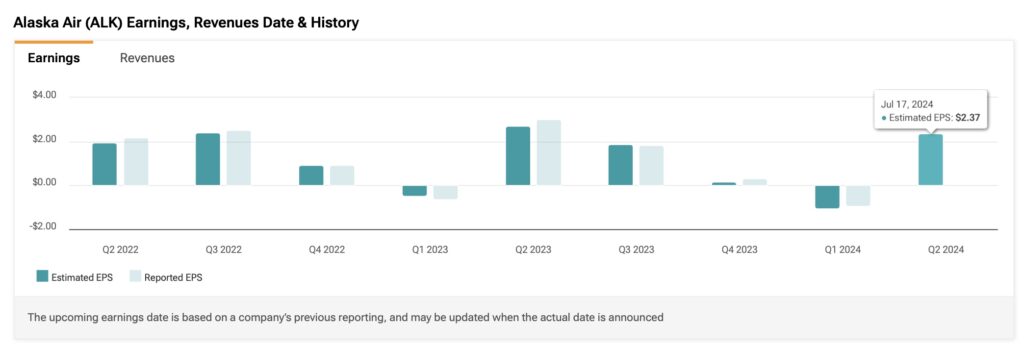

Alaska Air’s second-quarter earnings are just around the corner, scheduled for July 25. With the Boeing aircraft issues behind it, Alaska Air expects to gradually increase its capacity in Q2 and continue with small increases throughout 2024. The airline also anticipates that June could be its peak season for the year and potentially its strongest month.

The airline is expected to report a capacity increase of 5% to 7% year-over-year in Q2, with the lower end of the range being conservative due to uncertain aircraft deliveries. In Q1, Alaska anticipated strong Q2 bookings, with healthy yields observed in April.

Analysts forecast EPS of $2.37 for Q2 2024 compared to an expectation of $3 per share in Q2 2023. Revenue expectations for the quarter stand at $2.95 billion, indicating a roughly 4% annual increase.

Is ALK Stock a Buy, According to Analysts?

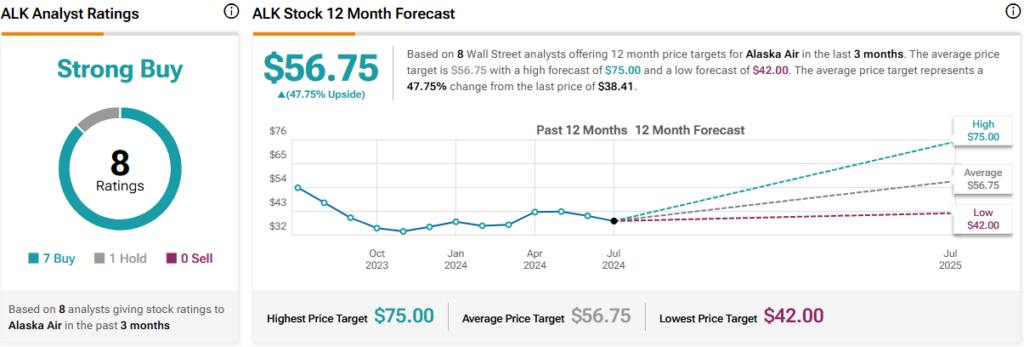

Wall Street experts are overwhelmingly bullish on ALK stock, giving it a Strong Buy rating. Out of eight analysts covering the stock, only one has a Hold position, with the remaining all recommending ALK as a Buy. The average ALK stock price target is $56.75, indicating significant upside potential of 47.75%. Click the image below to learn more.

The Takeaway

Alaska Air’s investment thesis stands out for being a legacy U.S. airline with an excellent balance sheet, cost structure, and geographic competitive advantages. Despite recent operational challenges beyond its control, I believe the stock has the potential to rebound strongly in Q2, with the airline likely reporting a net profit.

In the volatile and risky airline industry, I consider Alaska Air one of the less risky investments at the moment, which is why I maintain a bullish stance on the airline.