JPMorgan (JPM) is America’s largest investment banking stock by market cap.

Discover the Best Stocks and Maximize Your Portfolio:

- See what stocks are receiving strong buy ratings from top-rated analysts.

- Filter, analyze, and streamline your search for investment opportunities with TipRanks’ Stock Screener.

Led by Jamie Dimon, the firm has achieved tremendous success in recent times through offerings in investment banking, trading, loan origination, related consumer products, and more. I am bullish on the stock.

Viva Wallet Acquisition

JPMorgan has agreed a deal to acquire 49% of a European cloud-based payments company, Viva Wallet. The acquisition reiterates the bank’s emphasis on speeding up its payment solutions by expanding its omnichannel strategy. Furthermore, Viva Wallet adds scope to JPMorgan’s European operation, proving potential for growth synergies in the firm’s EMEA business unit.

There’s a strategic shift in big bank acquisitions, with popularity growing in buy now pay later and alternative payment systems. Companies such as Block (SQ), and PayPal (PYPL) have given banks such as JPMorgan a run for their money, and it seems as though it’s a case of, “If you can’t beat them, join them” for the big banks.

How this Will Affect JPMorgan

A critical aspect for investors to look at here is the recognition of the investment’s potential gains/losses on JPMorgan’s financial statements. JPMorgan Europe will be required to report under European accounting standards, but these will likely be converted to U.S. accounting standards at discrete periods.

Seeing as JPMorgan owns more than 20% of the firm but less than 50%, this investment will be recognized as an Investment in Associates type, in which the proportionate share of the subsidiary’s earnings will be reported on the investor’s balance sheet under the investment account line item. Furthermore, Viva Wallet’s earnings will be recognized proportionately on JPMorgan’s income statement; however, any dividends paid will be deducted from the gains realized from earnings increases.

It’s doubtful that JPMorgan will report under the proportionate consolidation method because this requires a majority influence on Viva Wallet’s daily operations. We’re thus unlikely to see JPMorgan report any of the subsidiary’s assets, liabilities, or minority interests on its balance sheet.

So, in a nutshell, JPMorgan will reap the benefits of Viva Wallet’s earnings and not hold liability on the subsidiary’s risk profile, making this a very lucrative investment for JPMorgan’s shareholders.

Valuation

I thought it would be productive to run through JPMorgan’s valuation metrics to provide some market context. The stock is still undervalued despite the popularity of banking stocks the past year, which saw JPMorgan gain 15.8%.

JPMorgan is trading at a price-to-earnings discount worth 25.3%, and if we combine this with its PEG ratio of 0.13, it’s safe to conclude that we’re looking at an undervalued stock here.

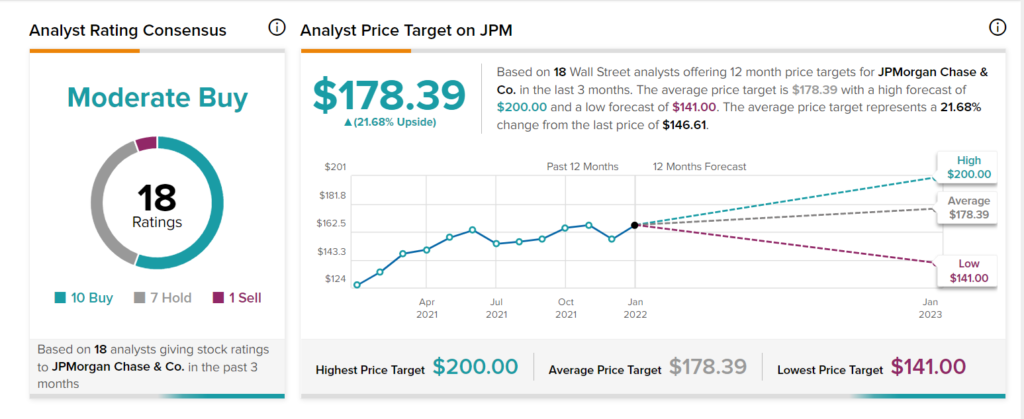

Wall Street’s Take

Turning to Wall Street, JPMorgan has a Moderate Buy consensus rating, based on ten Buys, seven Holds, and one Sell assigned in the past ten months.

The average JPMorgan price target of $178.39 implies 21.7% upside potential.

Concluding Thoughts

JPMorgan is expanding its footprint in the digital space, which is encouraging to see. The acquisition of Viva Wallet is a good move, especially considering its financial reporting benefits.

Download the mobile app now, available on iOS and Android

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Read full Disclaimer & Disclosure