Pieris Pharmaceuticals (NASDAQ: PIRS) is a clinical-stage biotechnology company whose pipeline includes locally-activated bispecifics for immuno-oncology and proprietary Anticalin proteins, a novel class of therapeutics that can be inhaled for the treatment of respiratory diseases.

Don't Miss our Black Friday Offers:

- Unlock your investing potential with TipRanks Premium - Now At 40% OFF!

- Make smarter investments with weekly expert stock picks from the Smart Investor Newsletter

In Q1, PIRS earned revenues of $15.6 million, mainly from its license and collaboration agreements with its partners. The company reported a net loss of $0.07 per share, the same as the first quarter of last year.

PRS-343

Yesterday, the company announced that its cinrebafusp alfa (PRS-343) had been granted orphan drug designation by the U.S. Food and Drug Administration (FDA). According to Pieris, the FDA grants orphan drug designation “to promote the development of a drug that targets a condition affecting 200,000 or fewer U.S. patients annually.”

This designation will result in Pieris getting development and commercial incentives, FDA assistance in the design of clinical trials, tax credits for eligible clinical trials, application fee waivers, and following FDA approval, market exclusivity for 7 years.

Cinrebafusp alfa (PRS-343) is a 4-1BB/HER2 fusion protein used in the treatment of gastric cancer, and after encouraging Phase 1 results, PIRS is now working towards initiating a Phase 2 study.

In March this year, Pieris announced the amendment of its previous agreement with Seagen (SGEN) and said that SGEN had made a strategic equity investment in the company. As part of a combination study agreement, the Phase 2 study of PRS-343 will be combined with Seagen’s tucatinib, a small-molecule tyrosine kinase HER2 inhibitor.

Late last month, H.C Wainwright analyst Joseph Pantginis reiterated a Buy on the stock with a price target of $9 (~106% upside potential).

Commenting on the amended agreement with Seagen, Pantginis told investors, “Pieris now has a co-promotion option in the U.S. with Seagen being wholly responsible for development beyond the Phase 2; if the option is exercised, Pieris would be entitled to increased royalties (we would project low double-digits)…We are encouraged by this announcement as it provides a broadening profile for PRS-343 in gastric cancer and beyond.”

Collaboration with Genentech

Late last month, PIRS announced its collaboration with Genentech, a member of Roche Holding AG (UK:0QOK), to develop, discover, and commercialize “locally delivered respiratory and ophthalmology therapies that leverage Pieris’ proprietary Anticalin technology.”

As a part of the agreement, Pieris will receive an upfront payment of $20 million and could be eligible to receive in excess of $1.4 billion in incremental milestone payments across multiple programs and tiered royalties for commercialized programs.

Under the terms of the agreement, while PIRS will be responsible for the discovery and early preclinical development, Genentech will be responsible for Investigational New Drug (IND)-enabling activities, clinical development, and commercialization of those programs. (See Pieris stock chart on TipRanks)

Pantginis commented on this agreement, “We continue to be impressed with Pieris’ business development capabilities as interest around the Anticalin platform continues to grow. We look forward to additional visibility around assets that are developed through this new partnership.”

PRS-060

The company stated in its Q1 press release that dosing had started as part of the global phase 2a study of PRS-060/AZD1402, an inhaled IL-4 receptor alpha inhibitor that is currently being developed with AstraZeneca (AZN) for the treatment of moderate-to-severe asthma. Data from the Phase 2a study is expected to be announced next year.

In addition, as part of its agreement with AstraZeneca, PIRS also received a milestone payment of $13 million in Q1. Pieris will have the option to co-develop and commercialize PRS-060/AZD1402 in the United States.

Valuation of PIRS

Analyst Pantginis’ valuation of PIRS is “currently based on PRS-060 (23% contribution) and PRS-343 (77% contribution). Our price target is based on our clinical net present value (NPV) model, which allows us to flex multiple assumptions affecting a drug’s potential commercial profile.”

“Factors which could impede reaching our price target include failed or inconclusive clinical trials or inability of the company to secure adequate funding to progress its drugs through the development pathway,” the analyst added.

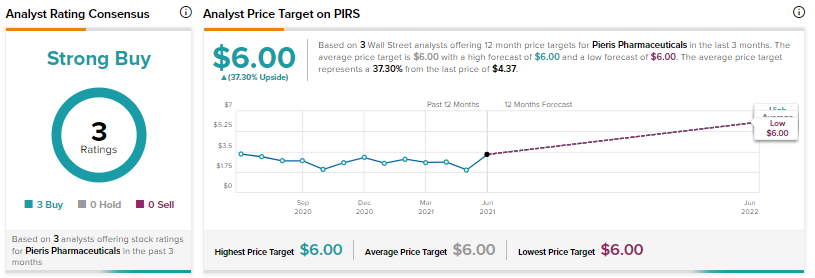

Consensus among analysts on Wall Street is a Strong Buy based on 3 Buys. The average Peiris Pharmaceuticals analyst price target of $6 implies approximately 37.3% upside potential to current levels.

Disclaimer: The information contained herein is for informational purposes only. Nothing in this article should be taken as a solicitation to purchase or sell securities.