Retail giants Walmart (NYSE:WMT) and Target (NYSE:TGT) both delivered top-line and EPS beats in their quarterly earnings last week. Further inspection, however, reveals a much different story for the companies, providing a reason for Walmart’s recent outperformance over Target, both of which endure varying effects from the macroeconomic climate.

Confident Investing Starts Here:

- Quickly and easily unpack a company's performance with TipRanks' new KPI Data for smart investment decisions

- Receive undervalued, market resilient stocks straight to you inbox with TipRanks' Smart Value Newsletter

Over the past year, Walmart’s 21.6% gain has surpassed both the S&P 500’s (SPX) 4.4% return and Target’s 3.5% decline. Year-to-date, while Walmart has continued to perform better than Target, with a 3.6% return compared to a 4.5% decline, the S&P 500 surpassed both with a gain of 7.2%.

Both businesses are generally similar, begging the question of why the stocks have performed so differently.

The answer lies in the continuing inflationary macroeconomic environment, weak consumer, and the different audiences targeted by each store’s offerings. As evident in its stock performance, Walmart has positioned itself to exploit such trends, reinforcing its already established sustainable competitive advantages and creating a positive outlook.

I’m bullish on Walmart and neutral on Target.

Contrasting Fundamentals

Walmart’s Recent Results

Walmart’s superior performance is apparent in its fundamentals, contrary to Target. Walmart’s total revenue increased by 7.6% year-over-year in Fiscal Q1 2024, supported by an increase in U.S. comparable sales of 7.4%, and operating income followed suit, increasing by 17.3% year-over-year. GAAP EPS decreased from $0.74 to $0.62, though adjusted EPS, which excludes the effects of losses on equity and other investments, increased by 13.1%. Although the firm’s gross margin fell 18 basis points amid higher inflation, some of this was offset due to improving supply-chain conditions and the normalization of shipping costs in the U.S.

ROA (return on assets) and ROI (return on investment) for the quarter were 4.5% and 12.7%, respectively, and the company has continued its dedication to returning wealth to shareholders through the repurchase of 4.8 million shares.

President and CEO Doug McMillon was pleased with the results, stating, “We had a strong quarter. Comp sales were strong globally with eCommerce up 26%. We leveraged expenses, expanded operating margin, and grew profit ahead of sales.”

Concurrently, the company raised its guidance for Fiscal Year 2024, expecting an increase of approximately 3.5% in consolidated net sales, 4% to 4.5% in consolidated operating income, and adjusted EPS of $6.10 to $6.20.

Target’s Recent Results

Such positivity does not continue into Target’s earnings, recognizing an “increasingly challenging environment” from the outset.

Comparable sales remained unchanged year-over-year, while revenue grew only 0.6%. Operating income decreased 1.4% compared to last year, shrinking its operating margin from 5.3% to 5.2%.

Somewhat surprisingly, unlike Walmart, Target’s gross margin actually improved slightly from 25.7% to 26.3% thanks to lower shipping costs and pricing power.

Nevertheless, both first-quarter GAAP EPS and adjusted EPS were down 4.8% year-over-year and 6.2% year-over-year, respectively.

As such, while the company maintains its full-year guidance of comparable sales in a range of a low-single-digit decline to a low single-digit increase, it expects a low single-digit decline in comparable sales in the next quarter resulting from weaker sales trends in the first quarter.

Exploiting the Macroeconomic Environment Bodes Well for Walmart

Walmart’s slogan of “Save Money. Live Better” may never have been as prevalent as in post-pandemic times.

It is no secret that the historical inflation endured as a result of demand-pull and cost-push inflation drastically affected food prices. It did not stop there, however, as drastic increases in energy, shelter, and other services diminished the spending power of consumers. Unfortunately, such detrimental effects did not end there.

Perhaps perceived as a necessary evil, the consequent action of the Fed to reduce inflation through restrictive monetary policy also depressed the finances of consumers, now facing elevated interest rates and tightening credit conditions.

In such times, consumer spending turns from elastic goods, or discretionary items, to goods of inelastic nature (essentials), regardless of price.

Even before the pandemic, Walmart was the textbook example of achieving economies of scale and scope, offering a wide variety of products on such a large scale to reduce prices. Offering inelastic goods such as food, health, and wellness products in a value-oriented nature is not only what is attracting the weak consumer to Walmart stores, but it’s facilitating Target’s struggles.

Rather than concentrating on essentials, Target has been attempting to differentiate itself by expanding its discretionary items, such as clothing and home products. In a similar token, it is spending a great deal on remodeling approximately 175 stores this year. While these initiatives may positively impact the company in the long run, it has simply exacerbated Target’s issues in the near future, as seen in its excess inventory woes, as demand for such discretionary items did not exist.

As with all decisions, Target encountered an opportunity cost, and in the near term, that cost is quite high. In turn, however, this cost to Target is Walmart’s gain.

Walmart’s Grocery category experienced low double-digit growth, with food units sold increasing year-over-year, and there was strength in the Pet and Personal Care segment as well. In a similar manner, Health and Wellness experienced growth in the high teens. Although General Merchandise had mid-single-digit declines, in which demand for discretionary items like electronics was weak, this decrease was not as pronounced as that experienced by Target.

Despite the likely peak of inflation and possible pause of the Fed and its tightening, such trends are likely to continue throughout the coming year, especially when the lagged effects of monetary tightening, such as increased unemployment, come to fruition eventually with the potential climax of a recession.

In such a case, home products and remodeled stores will not fulfill the demand of struggling consumers for low-cost inelastic goods.

Are WMT and TGT Worth Buying, According to Analysts?

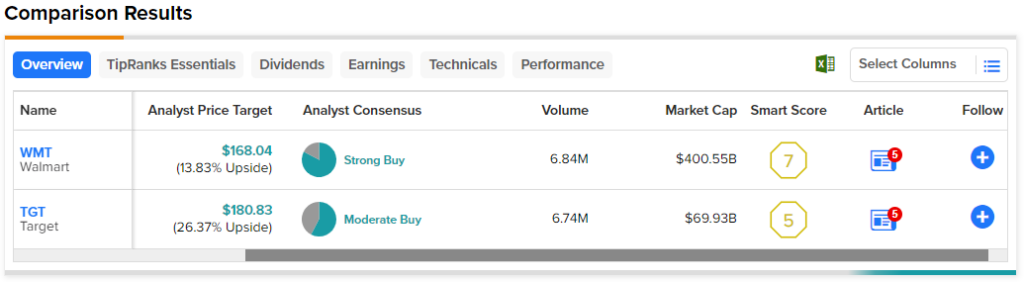

Given a shorter time horizon, Wall Street seems to concur. Walmart currently has a Strong Buy rating based on 24 Buys, five Holds, and zero Sells. The average WMT stock price target of $165.64 suggests 12.2% upside potential.

On the other hand, Target currently has a Moderate Buy rating based on 14 Buys, 10 Holds, and zero Sells, indicating a preference toward longer-term performance. The average TGT stock price target of $180.83 suggests 26.4% upside potential from there.

Conclusion

Walmart and Target have always battled for market share, trying to outdo one another. Despite their core businesses being rooted in solid fundamentals and enjoying the benefits of economies of scale and scope, Walmart’s focus on the lower-income consumer fares well in the current macroeconomic climate. This is especially true as even higher-income consumers search for cost-effective alternatives.

While not perfectly positioned to take full advantage of a value-oriented consumer, Target is committed to adapting to the needs of its customers and supplying the products in demand, both now and in the future.

While the winner is evident in the near term, such is not as clear with a longer time horizon in which the economy stabilizes and the consumer strengthens. In such a case, investors may consider adding both stocks to their portfolios, exploiting Target’s undervalued nature.

With such fierce competition, both companies will be forced to continue innovating and improving. The winner? Perhaps both. Only time will tell.