VeriSign (NASDAQ:VRSN) is arguably the chubbiest cash cow in the tech sector, with its one-of-a-kind characteristics having formed an extremely durable business model with incredible predictability prospects.

In this article, we will go over:

- VeriSign’s outstanding qualities

- How its qualities are reflected in its financial results

- VeriSign’s unique capital allocation strategy (buybacks)

- and whether the stock could be an attractive investment.

Nonetheless, I am neutral on the stock for the time being.

VeriSign’s Outstanding Qualities

VeriSign operates the registry for .com and .net domains, a business model that comes with an outstanding set of qualities and competitive advantages. Let’s explore them!

A Virtual Monopoly

The .com and .net top-level domains are the most widely used domain extensions in the world, which means that VeriSign essentially has exclusive control over the internet’s most critical infrastructure. The monopolistic nature of the registration and management of these domains provides VeriSign with a distinctive moat. VeriSign faces essentially no competition.

The Critical Nature of Its Business Model

As mentioned, the .com and .net domains are critical to the functioning of the internet, and VeriSign’s role in managing and operating these domains makes it a crucial player in the industry. The most important websites in the world run on these two domain platforms, and they need to operate with nearly 100% uptime.

The result of this is that VeriSign enjoys extremely reliable cash flows. Sure, a small churn in domain names is possible as a number of websites come and go. But generally, the recurring annual fees that VeriSign collects for hosting pretty much the entire commercial internet lead to a highly-predictable revenue stream with no notable risks attached.

Sustainable Organic Growth

VeriSign is able to achieve highly-sustainable organic growth in two ways — rate hikes and a growing number of domain names hosted.

As you can imagine, hosting the majority of commercial internet comes with massive advantages and responsibilities, and so VeriSign is highly regulated. Can you imagine if VeriSign forced everyone to pay ridiculous amounts for hosting their highly-vital domain names? This is why VeriSign is regulated by the Internet Corporation for Assigned Names and Numbers (ICANN).

Nevertheless, this gives the company the ability to request rate hikes for its services. These rate hikes are subject to review and approval by ICANN, but they can contribute significantly to the company’s revenue growth. In fact, a few days ago, VeriSign announced a 7% increase in .com prices to take effect on September 1, 2023, in line with to regulators’ prior approval for VeriSign to increase prices by 7% per annum over six years.

Now, combine these price hikes with a gradually growing number of .com and .net domain names that come online, and you can see why VeriSign enjoys highly-sustainable organic growth. For context, the company has gone from hosting just under 150 million domain names at the start of 2018 to 173.8 million names at the end of 2022.

VeriSign’s Qualities are Reflected in Its Financials

The most evident impact that VeriSign’s qualities have in its results is predictable cash flows and sustainable organic growth, as just mentioned.

However, another great outcome is massive profit margins. This is because hosting all these domain names is a very passive operation that doesn’t require meaningful expenses or future investments (CapEx). Therefore, as the company gradually grows its revenues while undertaking little to incremental expenses, its margins tend to expand over time.

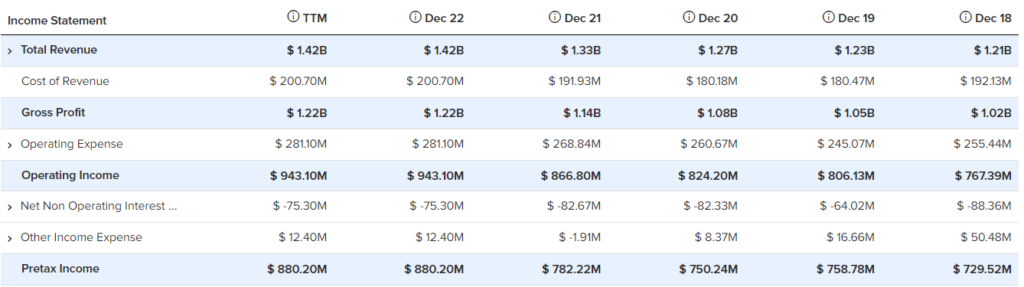

These attributes were once again displayed in VeriSign’s 2022 results. Specifically, revenues came in at $1.42 billion for the year, up 7.3% from FY-2021, while VeriSign’s operating margin was 66.2%, up from 65.3% in FY-2021.

How VeriSign Became a Stock Buyback Machine

As just explained, VeriSign has limited expenses, doesn’t need to allocate capital to grow, and generates tons of cash. So what do they do with all this cash? They return it back to shareholders in the form of buybacks. Every single dollar the company generates is essentially used to buy back stock.

To give you an idea of how consistent and considerable VeriSign’s buybacks are, over the past 18 years, the company has reduced its share count by 60%, and this includes a share count hike of 27% in 2018 as part of M&A.

Is VRSN Stock a Buy, According to Analysts?

Turning to Wall Street, VeriSign has a Moderate Buy consensus rating based on two unanimous Buy ratings assigned in the past three months. At $258.50, the average Verisign stock forecast implies 21% upside potential.

Takeaway: Is VeriSign Stock Actually Worth Investing In?

As highlighted in this article, VeriSign has multiple extraordinary attributes that differentiate it as a company and as a potential investment. Its highly-predictable cash flows, organic growth prospects, and invariable focus on creating value for shareholders are certainly worth considering.

That said, precisely because the market highly appreciates these qualities, shares of VeriSign are trading at a steep valuation multiple. The stock is currently trading at a forward P/E ratio of just under 31.

The combination of top-line growth and buybacks makes it highly likely that VeriSign will keep growing its earnings per share in the double-digits for the foreseeable future, which sort of justifies a rich valuation.

Nevertheless, such a high P/E could limit investors’ future total returns, which is something to have in mind before deciding whether VeriSign is actually worth investing in.