On the surface, Upstart (UPST) is a great idea. Take a lending platform and power it with artificial intelligence (AI) systems that can use a wide range of potential indicators to determine the potential creditworthiness of a loan applicant.

Invest with Confidence:

- Follow TipRanks' Top Wall Street Analysts to uncover their success rate and average return.

- Join thousands of data-driven investors – Build your Smart Portfolio for personalized insights.

That sounds like a good plan, but investors are increasingly unsure. Upstart is currently down a whopping 59% on the day.

However, I’m bullish on Upstart. While this may be a longer-term play, and one that’s definitely going to be hit by a possible upcoming recession, Upstart is a solid idea that should provide value in any kind of decent economy.

The last 12 months for Upstart shares feature two valleys and a peak. The company held fairly closely to around $120 a share for much of June and July 2021 before launching into a massive upward spike.

In October, the company briefly challenged $400 per share. That turned around badly, as the company lost over 90% of its value between there and today, where it trades at around $32 per share.

Meanwhile, the latest news proved little help to Upstart’s sagging share price. The company turned in a win for its first-quarter results earlier this week, but its full-year outlook was a much different story.

The company reduced its total revenue forecast for 2022 from its original $1.4 billion to just $1.25 billion. That’s not exactly a massive drop, but it’s still less than expected.

Further, Upstart looks to turn in a miss on second-quarter revenue figures as well. Upstart expects revenue between $295 million and $305 million. Sounds good, but Refinitiv analysts were looking for $335 million this quarter.

Wall Street’s Take

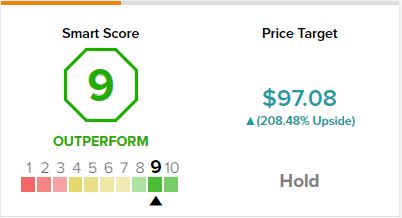

Turning to Wall Street, Upstart has a Hold consensus rating. That’s based on five Buys, five Holds, and two Sells assigned in the past three months. The average Upstart price target of $97.08 implies 202.7% upside potential.

Analyst price targets range from a low of $28 per share to a high of $255 per share.

A Mixed Picture for Investor Sentiment

The investor sentiment picture, meanwhile, is clearly holding out some hope for the company’s future, despite the long, long drop it’s taken over the last few months.

Hedge funds, for example—as based on the TipRanks 13-F Tracker—are increasingly buying in. For the last two quarters, hedge funds have increased their positions in Upstart.

From June 2021 to September 2021, hedge funds upped their involvement from just under 1.7 million shares to just under 4.3 million shares. A much more modest hike followed between September and December, with December coming in at just under 4.86 million shares.

Meanwhile, the insider trading picture at Upstart is much bleaker. “Sell” is the order of the day, as, in the last three months, there have been no buying transactions at all but 14 selling transactions. The full year features 72 selling transactions to just 23 buying transactions.

As for retail investors who hold portfolios on TipRanks, that too is a surprisingly mixed picture. The number of investors on TipRanks whose portfolios hold Upstart is down 0.1% in the last seven days but is up 0.2% in the last 30 days.

Nonetheless, the combination of these factors, as well as other factors, has allowed UPST to achieve a 9 out of 10 Smart Score Rating on TipRanks, implying that the stock can outperform the market from here.

Regarding Upstart’s dividend history, sadly, it does not exist, nor does it look to start any time soon.

Right Place, Wrong Time

There’s good news and bad news when it comes to Upstart. Indeed, that seems to be the case for a lot of financial technology companies right now. Upstart is cratering; we all know that much.

However, we also saw Brazil’s digital bank Nu Holdings (NU) slip in trading yesterday. Further, we saw credit giant Mastercard (MA) slip in yesterday’s trading as well. Both Nu and Mastercard are down today as well, so far.

So what do these three companies have in common? Exposure to lending.

It’s a bad time to be making loans right now. Like Upstart’s CFO Sanjay Datta noted, there are “general macro uncertainties” as well as “the emerging prospect of a recession later this year.” Throw in climbing interest rates, and the picture only worsens from there.

There’s likely to be less lending in general, which hurts Upstart’s primary focus. By using artificial intelligence to analyze potential borrowers’ creditworthiness, it improves the rate at which loans can be approved. It also stands to reason that more of those loans will come back valid.

None of these traits are especially useful when there are fewer loans to make overall. Granted, a better chance of recovering the loan is welcome. However, when no one’s borrowing in the first place, how much good does it do to have a better chance at recovery?

So yes, right now is a bad time for Upstart. It’s likely to see some significant decline in its lending activity going forward as borrowing slows. However, that’s not likely to remain the case forever. If it does, we have much bigger problems to face.

A recovery in the economy, in general, would likely turn the picture around for Upstart and its contemporaries. This rising tide would lift all—or at least most—boats, and Upstart would be back in the thick of it.

Concluding Views

Right now, it may not seem like a great idea to buy in on Upstart. There’s a point there, especially given that the company is about to see some of the worst periods for lending activity in quite some time. However, this isn’t likely to last forever. When its primary stock in trade, high-quality loans, is back in demand again, its share price should climb with it.

The company is currently trading well below even its lowest price targets. A return to its average target represents about a three-bagger, and that’s without even considering the roughly eight-bagger that the highest target would represent.

There are enough reasons to be bullish on Upstart, and anyone who’s willing to stick with it for the long term is likely to be rewarded in the future.

Discover new investment ideas with data you can trust.

Read full Disclaimer & Disclosure