Package delivery service United Parcel Service (UPS) has made quite a name for itself over the years. It’s one of a handful of companies that keeps the e-commerce movement alive and well.

Maximize Your Portfolio with Data Driven Insights:

- Leverage the power of TipRanks' Smart Score, a data-driven tool to help you uncover top performing stocks and make informed investment decisions.

- Monitor your stock picks and compare them to top Wall Street Analysts' recommendations with Your Smart Portfolio

During the pandemic it was a godsend, connecting people to goods without having to actually go anywhere. Now, some new love from the analyst sector is giving UPS a fresh lease on life. I’m also bullish on UPS, because this company has already demonstrated just how effective it can be.

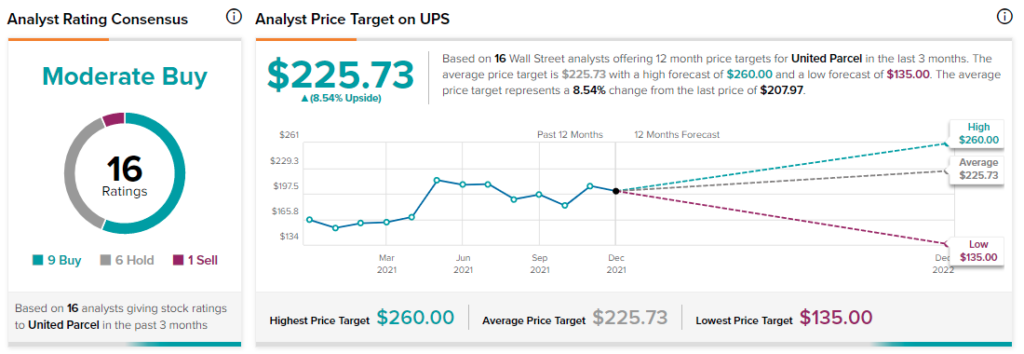

Based on the year in UPS stock prices so far, UPS has had a banner year. It spent most of the first quarter of 2021 plateaued down around the $150 mark. As March ended, so too began a new renaissance for UPS. The company started climbing, slowly at first, then with surprising alacrity.

By late April, the company’s share price breached the $200 mark, and didn’t stop there. May saw the company plateau around the $210 mark, before a small slip in June brought the share price under $200 briefly.

July was back to form, until another slip put the company back under the $200 mark, and largely kept it there for most of three months. October brought a Halloween surprise that sent the company back up over $200 once more, where it has remained ever since. Except, that is, for one short-lived dip in November.

The latest news should prove particularly helpful. Two analysts have recently modified their opinions on UPS, with closely named UBS leading off. UBS declared UPS stock a “top pick” thanks to two main factors.

One, UBS asserts that UPS is likely to benefit from increases in consumer spending. Two, UBS notes that UPS has a greater chance of seeing margin expansions than the various other package handlers out there.

The second analyst chipping in was from Citigroup (C). Citi not only upgraded the company to a Buy, but also put it ahead of FedEx (FDX) in its rankings. A recent union contract should help insulate the company from labor costs hiking. As well, increases in consumer spending are likely to give UPS more to deliver in general.

Wall Street’s Take

Turning to Wall Street, UPS has a Moderate Buy consensus rating. That’s based on nine Buys, six Holds, and one Sell assigned in the past three months. The average UPS price target of $225.73 implies 8.5% upside potential.

Analyst price targets range from a low of $135 per share to a high of $260 per share.

Can It Go Higher?

Granted, there’s a bit of bad news for UPS right out of the gate. The company is currently trading a shade under its average price target. It’s also running about $60 shy of its highest price targets. A reversion to the lowest price target seems unlikely. However, there isn’t a lot of room for further gains unless the company starts shattering price targets. That is also unlikely.

There’s an old saying: “Once is happenstance. Twice is a coincidence. Third is a pattern.” The original sentiment replaces “a pattern” with “enemy action.” However, since the concept applies well beyond military applications, it works just as well for our purposes. We’re already up to a coincidence, so let me go ahead and turn this into a pattern.

We know consumer spending is up. Also, we know that it’s up at a level that doesn’t account for inflation alone, though inflation is definitely contributing.

Just to top it off, UPS is also a great income stock to consider. The company’s dividend has been increasing regularly for the last two years. That, when combined with the company’s performance, suggests a safe and stable dividend calendar.

Granted, the share prices are kind of high to make this a dividend stock for most. By all indications however, UPS shareholders will enjoy a stable long-term dividend.

Concluding Views

UPS is in a great position going forward. It’s taking advantage of the holiday shopping season to ramp up deliveries. It’s delivering more in general thanks to improved shopping rates.

UPS can even hold its costs in line thanks to a new labor contract. That ensures greater profitability; reducing costs and raising revenues is the gold standard formula for increasing profits.

When multiple analysts can see a path to better profitability for a company, it’s hard not to be bullish. With UPS’ fortunes improving, it’s a safe bet that this company will keep right on producing.

Disclosure: At the time of publication, Steve Anderson did not have a position in any of the securities mentioned in this article.

Disclaimer: The information contained in this article represents the views and opinion of the writer only, and not the views or opinion of TipRanks or its affiliates. Read full disclaimer >