In this piece, I evaluated two poultry and meat producer stocks, Tyson Foods (NYSE:TSN) and Pilgrim’s Pride (NASDAQ:PPC), using TipRanks’ comparison tool to determine which is better.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Tyson is a multi-national, protein-focused food company that produces about 20% of the beef, pork, and chicken in the U.S. and many food products under its well-known brands like Hillshire Farm and Jimmy Dean. Pilgrim’s Pride delivers fresh and value-added or prepared poultry products under its well-known brands, like Pilgrim’s Chicken and Country Pride, in over 100 countries.

Neither stock is holding up particularly well, although Tyson Foods is doing far worse than Pilgrim’s Pride. Tyson is off almost 38% for the last year, including a 19% year-to-date plunge, while Pilgrim’s Price has tumbled 24% over the last 12 months, including a decline of 5% year-to-date.

The U.S. food industry is trading at around its three-year average price-to-earnings (P/E) ratio of 21.6, although its three-year average price-to-sales (P/S) ratio of 1.2 is slightly higher than the current ratio of 1.1. Tyson and Pilgrim’s Pride are both trading at extremely depressed valuations compared to their sector, so a closer look is needed to determine the reasons for that.

Tyson Foods (NYSE:TSN)

Tyson is trading at a P/E of 12 and a P/S of 0.3, although its five-year mean P/E is 10.9, and its five-year mean P/S is 0.6, so it always trades at a deep discount to the food industry. However, given its recent sell-off and long-term track record, Tyson Foods looks like a buy-the-dip opportunity, suggesting a bullish view.

Tyson has had a bumpy few years, but its stock is trading at the bottom of its range since December 2015, and it’s a solid long-term performer. Interestingly, insiders scooped up some shares about a month ago — right around the time Tyson released its last earnings report.

Nonetheless, the company swung to a surprise net loss that caused its stock to plummet sharply and shed about $10 a share. However, the company’s sales were flat year-over-year, and it has the staying power to last through these challenging times.

Finally, Tyson has a dividend yield of 3.8%, so it could be worth adding to a dividend portfolio.

What is the Price Target for TSN Stock?

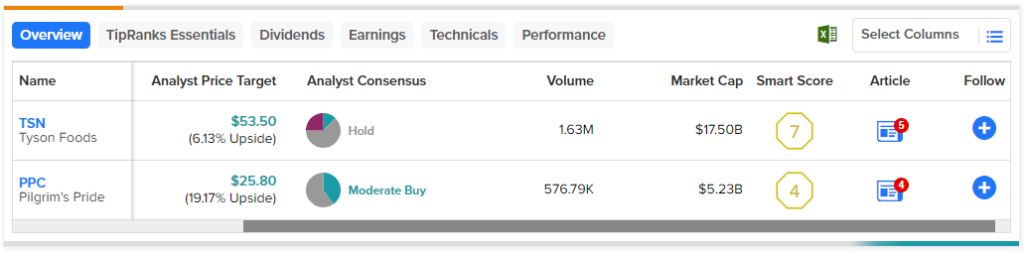

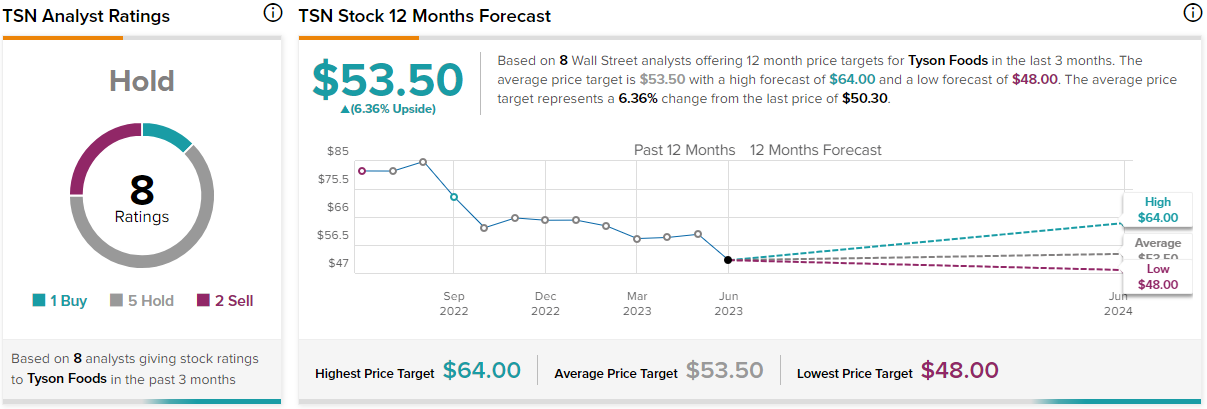

Tyson Foods has a Hold consensus rating based on one Buy, five Holds, and two Sell ratings assigned over the last three months. At $53.50, the average Tyson Foods stock price target implies upside potential of 6.4%.

Pilgrim’s Pride (NASDAQ:PPC)

At a P/E of 11.3 and a P/S of 0.3, Pilgrim’s Pride is trading slightly below to in line with Tyson. However, the company is much smaller than Tyson, and over the long term, it hasn’t performed as well, suggesting a neutral view could be appropriate at current levels.

Pilgrim’s Pride’s five-year mean P/E is negative due to the steep losses it racked up in late 2021 and early 2022. However, over the last five years, Pilgrim’s Pride has generally been trading at a P/E between eight and 41. Additionally, its five-year mean P/S is 0.5, although it traded as high as 0.7 in early 2020. Still, in the last five years, the company has traded as low as $16 in 2020, so it simply isn’t attractive at current levels (near $22).

Just recently, prominent hedge fund Appian Way more than quadrupled its stake in Pilgrim’s Pride, making it the fund’s fourth-largest position. Thus, the company could be worth watching for a better entry point, although its balance sheet has become somewhat concerning, especially considering the negative $256 million in free cash flow it has accumulated over the last 12 months.

Finally, unlike Tyson, Pilgrim’s Pride doesn’t pay dividends, so it isn’t even a dividend play.

What is the Price Target for PPC Stock?

Pilgrim’s Pride has a Moderate Buy consensus rating based on two Buys, three Holds, and zero Sell ratings assigned over the last three months. At $25.80, the average Pilgrim’s Pride stock price target implies upside potential of 19%.

Conclusion: Bullish on TSN, Neutral on PPC

While Tyson’s has sold off much more than Pilgrim’s Pride, that plunge has created a nice buy-the-dip opportunity in a company that’s now trading at the bottom of its range since 2015. Additionally, Tyson is in a better long-term position with a debt/equity ratio of 45.7%, versus Pilgrim’s Pride at 121%, making Tyson the better choice between the two.