Biotech stocks give a whole new meaning to risk/reward plays. Unlike names inhabiting other areas of the market, these tickers can witness explosive movements in the blink of an eye, giving them a Street reputation for their high volatility.

Discover the Best Stocks and Maximize Your Portfolio:

- See what stocks are receiving strong buy ratings from top-rated analysts.

- Filter, analyze, and streamline your search for investment opportunities with TipRanks’ Stock Screener.

Companies in the biotech industry are unique in that their long-term growth prospects don’t necessarily hinge on quarterly profit results. Rather, clinical trial data or verdicts from regulatory bodies can have a more meaningful impact as product approvals indicate vital revenues are on the horizon. This means any positive development can act as a catalyst that sends shares skyrocketing. The flip-side, however, does hold true, so the risk-averse tend to shy away from these names.

So, how are investors supposed to determine which biotech stocks are capable of outperforming the rest? Tracking the analyst community’s activity can be an effective strategy. The pros, who have in-depth knowledge of the industry, offer insight into many biotechs, some of which fly relatively under-the-radar.

Bearing this in mind, we used TipRanks’ database to track down affordable yet compelling biotech plays. After combing through the densely packed sector, we found three going for less than $5 apiece with bullish reviews from Wall Street analysts and over 100% upside potential.

Spectrum Pharmaceuticals (SPPI)

Primarily targeting diseases in hematology and oncology, Spectrum Pharmaceuticals hopes its therapies will be able to address the unmet medical needs of patients. With a $3.08 share price, some analysts believe that now is the ideal time to snap up shares.

Writing for H.C. Wainwright, 5-star analyst Edward White remains focused on its novel long-acting granulocyte colony stimulating factor (GCSF) designed to stimulate neutrophil production for the treatment of chemotherapy induced neutropenia patients, Rolontis. Ahead of the candidate’s October 24 PDUFA date, the analyst highlights that Rolontis isn’t a biosimilar, and calls for 2020 sales of $3 million. Underscoring the huge potential here, he estimates sales will reach $300 million in 2026.

“Pricing in the market seems to be rational with the competition appearing more typical of a branded drug market rather than a generic drug market. Management noted that about 1 million units of GCSF are dispensed per year and that ASP price has been compressing between branded drugs and biosimilars. Despite the COVID-19 pandemic, the company has plenty of inventory available to support the commercial launch of Rolontis,” White commented.

It should also be noted that given the uncertainty surrounding COVID-19, management is planning for both a traditional and a virtual launch. In addition, SPPI is set to have a sufficient sales force on board in time for the commercial launch.

Looking at the clinical trial for Rolontis dosed on the same day as chemotherapy, White argues that the design should bode well for SPPI. “As this is an open-label study, the company can see early data before deciding to continue with development. Though data for a label change are years away, if the data are positive, this study could help dramatically change Rolontis’ market share in the future as we believe same day dosing in a post-COVID-19 world could be a game changer,” he explained.

With ZENITH20 Cohort 1 Poziotinib data at AACR demonstrating “there may be some hope yet”, the deal is sealed for White.

In addition to reiterating a Buy recommendation, he left his price target at $11. This target implies shares could climb 250% higher in the next year. (To watch White’s track record, click here)

Overall, though not many have weighed in with an opinion on SPPI in the last 3 months, those who have are singing its praises loudly. Overall, two analysts rate the stock a Buy, and the $9.50 average price target puts the potential twelve-month gain at 202%. (See SPPI stock analysis on TipRanks)

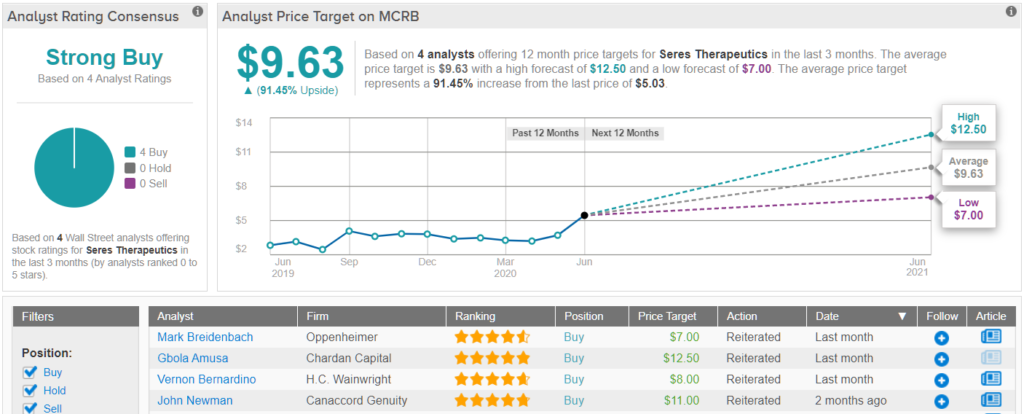

Seres Therapeutics (MCRB)

Taking its place at the forefront of microbiome therapeutics, Seres Therapeutics wants to transform the treatment of a wide range of diseases by modulating the function of the human microbiome.

Based on the multiple catalysts slated for 2020 as well as its $4.73 share price, it’s no wonder MCRB is getting glowing reviews from several members of the Street.

Standing squarely in the bull camp is 5-star analyst Gbola Amusa, of Chardan Capital. He points out that enrollment for the Phase 3 ECOSPOR III trial evaluating SER-109’s ability to prevent recurrent C. difficile infection (rCDI) is complete, with the candidate already receiving Breakthrough Therapy Designation.

As for the implications of this development, Amusa noted, “With positive results on the expected mid-2022 readout, ECOSPOR III has the potential to be a single pivotal study for the FDA; Seres plans to initiate a SER-109 Expanded Access Program.”

Adding to the good news, the company has taken strides forward when it comes to the advancement of the clinical development for its rationally-designed, fermented microbiome medicine, SER-155, for the prevention of mortality due to gastrointestinal infections, bacteremia and graft versus host disease (GvHD) in immunocompromised patients.

It should be noted that management told investors COVID-19 could impact its SER-287 Phase 2b and SER-401 Phase 1b clinical readouts. This is because the pandemic has put non-essential procedures including endoscopies on hold, and thus, it has been challenging to reach enrollment targets on time. That being said, the company doesn’t believe the availability of its product candidates for ongoing studies will experience any disruptions.

While a potential data readout delay has alarmed some investors, Amusa remains unphased. “Even with Covid-19-related uncertainties on SER-287 and SER-401, we continue to see 2020 as a catalyst rich year for Seres on the ECOSPOR III results alone, which with positive results could lead to SER-109 becoming the first FDA-approved microbiome medicine. Even with recent movements, the current MCRB market cap of $334 million to us is still modest in relation to the risk-adjusted opportunities represented by the pipeline,” he explained.

In line with his optimistic take, Amusa rates MCRB a Buy along with a $12.50 price target. This leaves room for shares to soar 151% in the next year. (To watch Amusa’s track record, click here)

Do other analysts agree with Amusa? They do. Only Buy ratings, 4, in fact, have been issued in the last three months, so the consensus rating is a Strong Buy. At $9.63, the average price target puts the potential twelve-month gain at 91%. (See MCRB stock analysis on TipRanks)

Akari Therapeutics (AKTX)

Last up to bat we have Akari Therapeutics, which develops innovative treatments for autoinflammatory diseases involving the complement (C5) and leukotriene (LTB4) pathways. Given its strong execution and share price of only $2.14, is now the right time to get in on the action?

According to B.Riley FBR’s Mayank Mamtani, the answer is a resounding yes. At the end of May, the company provided an update on the progress of the clinical trials for bullous pemphigoid (BP), atopic keratoconjunctivitis (AKC) and pediatric transplant-induced thrombotic microangiopathy (HSCT-TMA) indications for its lead program, nomacopan. The candidate is also getting attention for its potential as a therapeutic option for COVID-19 patients.

The 5-star analyst thinks the full Phase 2 BP study results, as well as an orphan designation granted by the FDA and EMA, free AKTX up to kick off end-of-Phase 2 meetings with the FDA and EMA in Q3 2020 to discuss the pivotal Phase 3 trial design. These meetings would address important considerations including enrolling severe patients in addition to mild and moderate, increasing treatment duration from 1.5 to 6 months, an option to dose at 30 mg-plus levels and a choice of active versus comparator arms, including possibly combining or sequencing with steroids.

“There were no treatment-related serious AEs, in line with the favorable tolerability profile noted in other indications (e.g., PNH), highlighting further differentiation relative to steroid standard of care,” Mamtani stated.

However, Mamtani doesn’t dispute the fact that the COVID-19 pandemic has delayed site initiation activities for the Phase 3 HSCT-TMA trial to later in 2020 and the enrollment for the Part B placebo-controlled efficacy cohort of the Phase 1/2 study in severe AKC patients has been halted. That said, Mamtani notes “the interim update remains on track for mid-2020 in ~2/3rd of the targeted 16 patients already enrolled in the study.” He added, “The prior open-label data of nomacopan eye drops demonstrated in three severe atopic keratoconjunctivitis (AKC) patients rapid overall improvement in composite clinical scores of symptoms and signs.”

On top of this, preclinical data has found complement (C5) and leukotriene (LTB-4) pathways may play a role in severe lung inflammation and microthrombi and organ damage associated with COVID-19. This creates an opportunity for nomacopan as it has been shown to produce a “profound and broad-acting anti-inflammatory effect.”

To wrap it all up, Mamtani commented, “We believe AKTX has held up well in the volatile macro environment as investors look to take advantage of the depressed stock levels for this late-stage biotech supported by robust clinical data generated in earlier-stage trials, with incremental Phase 1/2 severe AKC placebo-controlled data anticipated in mid-2020.”

Everything the company has going for it prompted Mamtani to stay with the bulls. Along with a Buy rating, he kept his $5 price target as is, bringing the upside potential to 134%. (To watch Mamtani’s track record, click here)

Turning now to the rest of the Street, it has been quiet when it comes to other analyst activity. Mamtani’s call was the only one issued recently.

To find good ideas for biotech stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.