President Trump will take office next week, and he’s not wasting time publicizing his plans for his non-consecutive second term. Prominent among those plans is DOGE, the Department of Government Efficiency, to be headed by Elon Musk and Vivek Ramaswamy. Their mandate: to cut as much as possible from the Federal Government’s expenditures. They’ve already talked about trimming $2 trillion worth of fat.

Discover the Best Stocks and Maximize Your Portfolio:

- See what stocks are receiving strong buy ratings from top-rated analysts.

- Filter, analyze, and streamline your search for investment opportunities with TipRanks’ Stock Screener.

While there’s no guarantee that Musk and Ramaswamy will find $2 trillion to cut, just that prospect has investors worried about defense industry stocks. The Pentagon has always been a target when it comes to trimming government waste (remember the $600 hammer?), and recent costly—and high-profile—programs such as the F-35 fighter jet or the Navy’s Littoral Combat Ship have been rife with cost overruns, delays, and even flat-out performance failures.

So maybe it’s no surprise that Truist analyst Michael Ciarmoli has homed in on the pullback in defense-related stocks in recent weeks. At the same time, the 5-star analyst points out that the aerospace sector offers a compelling point of entry for investors.

“In a sense 2025 feels a bit like groundhog day — entering 2024 investors’ sentiment was bullish on an aero OEM production recovery while turning bearish on the aftermarket rally. The setup for 2025 looks and feels eerily similar. However, while aircraft production is likely to improve in 2025 off an easy comp planned production rates increases are not materializing as fast as expected and we think the aftermarket still has legs. Within the defense sector the November Election and announcement of DOGE eviscerated performance but we believe the sell-off has created an attractive entry point,” Ciarmoli opined.

So, which stocks should investors grab during this dip? Ciarmoli has two clear favorites, and we’ve turned to the TipRanks platform to uncover what makes these picks stand out from the rest. Let’s dive in.

Lockheed Martin (LMT)

First up is Lockheed Martin, based in Bethesda, Maryland, and acting as the modern incarnation of two venerable names in the aerospace field: Lockheed and Martin Marietta. The modern company was established through their merger in 1995, and today boasts a $114-plus billion market cap.

Lockheed Martin is also the manufacturer of some of the military’s most important combat platforms, such as the F-16 and F-35 combat jets and the C-130 transport aircraft, along with a wide range of communications and surveillance satellites—and that is just the tip of this company’s iceberg. Lockheed Martin also works with various US-aligned militaries around the world, adapting US systems to their needs—or even producing local variants on American gear.

Like most aerospace/defense firms, this company is also deeply involved in the research and development of new technologies, weapons systems, and air and spacecraft. The company’s R&D arm is embodied in its famous Skunk Works, the semi-secret operation that develops new tech for everything from intelligence and surveillance to hypersonic flight to digital design prototyping—and those are just some of the things that the public knows about.

On the financial side, Lockheed Martin has proven itself profitable, and has a history of returning capital to shareholders. In its last reported quarter, 3Q24, the company generated $17.1 billion in total revenue, up 1.3% year-over-year, although it missed the forecast by $270 million. At the bottom line, LMT realized a non-GAAP EPS of $6.84, up 7 cents per share from 3Q23 and some 40 cents ahead of the estimates. The company has maintained its capital returns, and in Q3 increased its share repurchase authorization by $3 billion to a new total of $10.3 billion. The company also increased its common share dividend, bumping it up by 5% to $3.30 per share. The dividend was paid on December 27; the annualized rate of $13.20 gives a forward yield of 2.7%.

We should note here that shares in LMT are down in recent months. The shares peaked at more than $614 back in October; since then, the stock has fallen more than 20%.

For Truist’s Ciarmoli, who ranks in the top 2% of Wall Street stock experts, the two key points here are the reduced share price and the likelihood that the DOGE-related worries are more hype than substance. He says of Lockheed Martin, “We believe LMT’s recent pullback off its recent high has created a compelling entry point. Ultimately we believe DOGE related fears are overblown, investors must realize that this is not Sequestration 2.0, the threat level remains elevated and U.S. Defense/NATO defense spending will continue to rise in the coming periods. Admittedly the F-35 has a bulls-eye on its back, but we see a low probability of the prgm being cancelled/curtailed in the NT, and we believe mgmt’s growth framework will prove conservative, with missile related revs pacing growth and FCF being revised higher.”

Based on this, Ciarmoli puts a Buy rating on LMT, along with a $579 price target that implies a one-year gain for the stock of 19.5%. (To watch Ciarmoli’s track record, click here)

Lockheed Martin has a Moderate Buy rating from the Street’s analyst consensus, based on an almost even split in the 15 recent reviews, 7 to Buy and 8 to Hold. The shares are priced at $483.97 and have an average target price of $571.87, indicating a 12-month gain of 18%. (See LMT stock forecast)

Northrop Grumman Corporation (NOC)

Next up is another company formed through the merger of storied aerospace names. Northrop Grumman combines the legacies of two famous aircraft designers, Northrop and Grumman, that were active in the years prior to the Second World War and during the war produced some of the US military’s most iconic aircraft. Grumman built its reputation as a major supplier of Navy combat planes in the Pacific, while Northrop was more active in experimental designs.

Northrop Grumman, their modern corporate descendant, was formed through a 1994 merger and is involved in numerous high-profile military aircraft programs, including the B-2 stealth bomber, the Navy’s E-2 airborne radar aircraft, and the Air Force’s T-38 supersonic advanced trainer. In addition, the company is developing the B-21 bomber, the planned successor to the B-2.

Aerospace is only part of Northrop Grumman’s activities. The company is also deeply involved in such fields as electronic warfare, directed energy weapons, and even unmanned submersible minehunters. Outside of military programs, the company is working with NASA on the Artemis launch system. All of this makes Northrop Grumman one of the main contractors for the US defense establishment, as well as a large number of foreign military agencies.

Turning to financial results, we find that Northrop Grumman brought in $10 billion during its last reported quarter, 3Q24. While that missed the forecast by $170 million, it was up 2% from the prior year period. The company’s bottom-line EPS of $7 was up 13% year-over-year and came in 94 cents per share better than expected. During the quarter, Northrop Grumman received net awards of $11.7 billion and has reported a record work backlog of $85 billion.

Like its peer Lockheed Martin, above, Northrop Grumman has seen its share price fall in recent months. The stock was trading as high as $543 at the beginning of October, and today the shares are down to $472.

In his coverage of Northrop Grumman, Ciarmoli points out several reasons why the stock is deserving of a premium valuation and again notes that the shares’ recent decline presents an opportunity. “First and foremost, based on mgmt guidance we believe the company will grow its annual FCF at a mid-teens rate through 2028 which is almost double the growth rate of its peers. Second, we believe the company’s franchise nuclear triad programs will act as pillars of stability and revenue growth drivers while being nearly untouchable from any DOGE related funding cuts should they materialize. Third, we believe NOC’s overall revenue growth has the potential to accelerate to a MSD rate in the coming years amid strong weapons recapitalization demand, NATO related spending, and a recovering space segment,” the top analyst explained. “We believe NOC’s recent pullback off its late 2024 high has created a compelling entry point.”

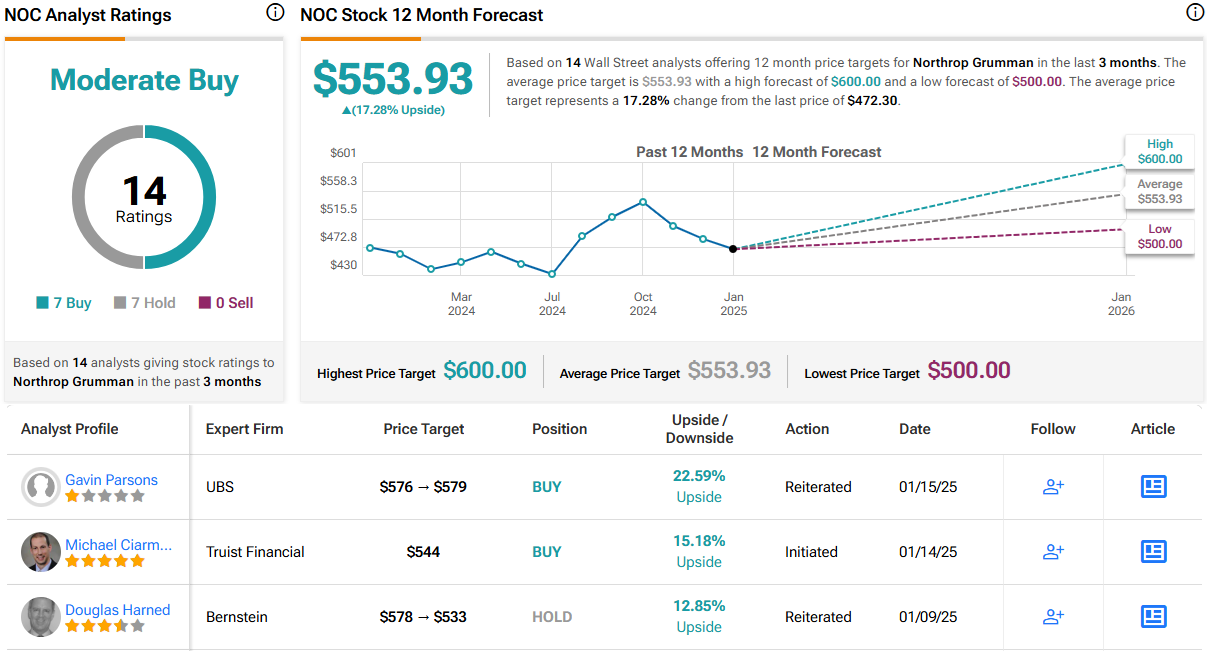

Quantifying his stance, Ciarmoli puts a Buy rating here with a $544 price target to suggest a share appreciation of 15% on the one-year horizon.

This stock also claims a Moderate Buy consensus rating, based on 14 reviews split evenly between 7 Buys and 7 Holds. The shares are priced at $472.30 and have an average target price of $553.93, implying that a one-year gain of 17% is in store for the year ahead. (See NOC stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.