Cathie Wood’s singular investing style has generated huge returns for investors of her ARK Invest ETFs during certain periods (such as during the pandemic). However, it’s a strategy that has also been responsible for racking up losses during other times, such as last year’s bear market.

Invest with Confidence:

- Follow TipRanks' Top Wall Street Analysts to uncover their success rate and average return.

- Join thousands of data-driven investors – Build your Smart Portfolio for personalized insights.

Wood’s preference has always been for disruptors – whether in tech, healthcare, or the auto industry – and even in difficult times, she has not deviated from that path. Whatever you make of her stock choices, Wood has shown the nerve to stick to her guns even when the chips are down.

Recently, the CEO of ARK Invest has been out shopping again, loading up on a pair of stocks that fit a certain profile: they offer game-changing potential and they might just be too cheap to ignore. Both stocks are currently trading for under $10, and according to Wall Street analysts, they also exhibit robust upside potential. Let’s take a closer look.

908 Devices (MASS)

For our first Wood-endorsed stock, let’s take a look at a disruptor in the field of chemical analysis and detection technologies: 908 Devices. This company specializes in developing innovative handheld and desktop devices that enable real-time, on-site chemical analysis. Their cutting-edge products utilize high-pressure mass spectrometry (HPMS) technology, which allows for the rapid identification and quantification of various substances in complex mixtures. This technology is particularly useful in a wide range of industries, including safety and security, life sciences, and energy, where accurate and timely chemical analysis is crucial.

Its flagship field forensics device, MX908, is a handheld, battery-powered Mass Spec device intended to quickly analyze gas, liquid, and solid materials of undetermined identity.

The Handheld revenue made up the bulk of sales in the most recently reported quarter, for 1Q23. The segment generated $6.2 million, amounting to a 38% year-over-year increase. The total top-line haul came in at $9.5 million, up 14.3% from the same period a year ago and just edging ahead of the forecast by $0.85 million. However, EPS of -$0.39 fell short of the -$0.36 anticipated by the analysts.

The shares are up by 13% year-to-date but zoom out a bit and it’s a different story. The stock is down by 40% over the past year.

Evidently, the lowered price must be appealing to Wood. Since March, she has purchased 456,342 shares through her ARK Genomic Revolution ETF (ARKG), bringing the total MASS shares in the fund to 4,041,206. These shares are currently worth over $34.75 million.

It’s a purchase that most likely gets the thumbs up from Stifel analyst Daniel Arias, who highlights the stock’s appealing valuation.

“MASS’s 1Q23 was solid with the top-line coming in above the consensus (in-line with Stifel) on a mix that has the handheld business exceeding expectations and helping to backfill on a desktop business that is facing the same headwinds seen across the bioprocessing industry,” Arias said. “Within our coverage universe, MASS handily wins the award for the stock with the strangest trading patterns – so we can’t rule out additional volatility as the year progresses, but with shares trading at just ~1x sales and the balance sheet providing runway for several years, we continue to recommend it for those digging through the smid-cap space.”

These comments underpin Arias’ Buy rating while his $17 price target suggests the shares will climb ~98% higher from the current trading price of $8.60. (To watch Arias’ track record, click here)

And the rest of the Street? All are on board. With a full house of Buys – 5, in total – the analyst consensus rates the stock a Strong Buy. The $17 average target is identical to Arias’ objective. (See MASS stock forecast)

Adaptive Biotechnologies (ADPT)

Next up, Wood has been leaning into a leader in a rapidly emerging field. Adaptive Biotechnologies is a pioneering commercial-stage biotech company at the forefront of immune-driven medicine. By harnessing genetic data stored in our adaptive immune systems, the company has developed technologies that enable the precise characterization and monitoring of the immune response.

The company’s clonoSEQ product is a next-gen sequencing-based assay designed to detect and monitor minimal residual disease (MRD) in patients with hematologic cancers and has been approved by the FDA for use in multiple indications.

In Q1, driven by 57% clonoSEQ volume growth to 12,079 tests, revenue reached $37.6 million, beating the Street’s forecast by $0.69 million. That said, at the other end of the equation, EPS of -$0.40 missed the -0.38 forecast.

Looking ahead, the company reiterated its expectation for full-year 2023 revenue in the range between $205 million to $215 million, compared to consensus at $208.90 million. The company continues to see operating expenses, including cost of revenue, coming in lower than the full year 2022 operating expenses of $385.5 million.

The shares, however, have underperformed the market this year, showing a decline of 17%. Not great for investors, but evidently enticing for Wood. This month, she purchased 558,196 ADPT shares through her ARK Genomic Revolution ETF (ARKG). Total ADPT shares in this fund have now reached 9,554,319, amounting to a market value of more than $62.58 million.

Wood’s confidence is mirrored in J.P. Morgan analyst Julia Qin’s take. She writes: “1Q was another strong quarter with continued ClonoSeq strength, and although management views milestones conservatively and in the NT GM will remain pressured with improvements in 2H, we continue to think that ADPT is a unique play in immune-based diagnostics and therapeutics, with a rich pipeline and meaningful ‘call options’ around drug discovery milestones and royalties.”

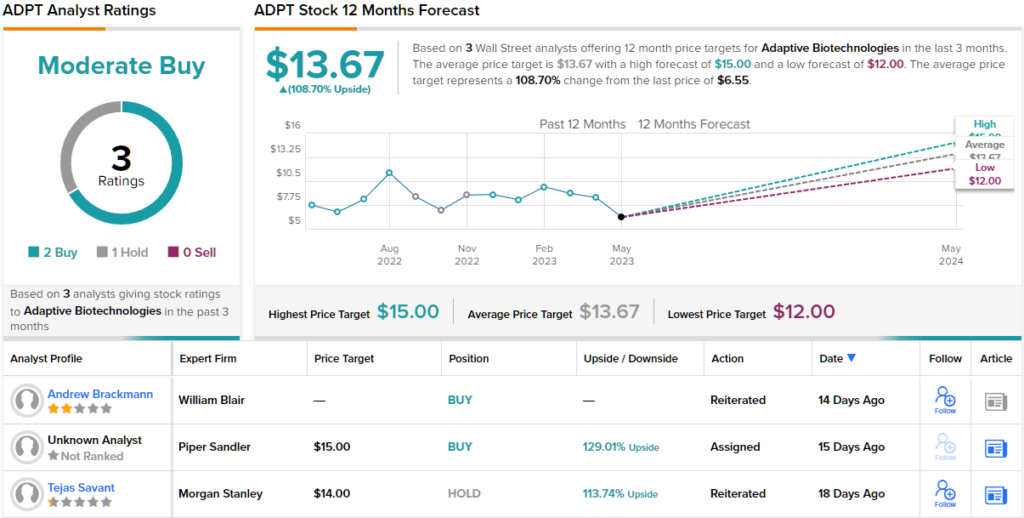

Qin obviously thinks the shares are mighty cheap at their current valuation. Along with an Overweight (i.e., Buy) rating, her $15 price target implies one-year share appreciation of a hefty 129% from the current trading price of $6.55. (To watch Qin’s track record, click here)

Elsewhere on the Street, one other analyst joins Qin in the bull-camp and with 1 additional Hold, the stock claims a Moderate Buy consensus rating. There are plenty of gains projected here; the $13.67 average target makes room for 12-month growth of ~109%. (See ADPT stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.