The market provides a vast array of data, the aggregated results of thousands of traders dealing in thousands of public stocks, for millions of daily transactions. This data gives investors all the signals they’ll need to sort through the market and find the right stock, but the sheer volume is an intimidating barrier.

Confident Investing Starts Here:

- Easily unpack a company's performance with TipRanks' new KPI Data for smart investment decisions

- Receive undervalued, market resilient stocks straight to you inbox with TipRanks' Smart Value Newsletter

This is where the Smart Score comes in. Developed by TipRanks, the Smart Score is an AI-powered natural language data-sorting algorithm, purpose-built to gather, collate, and, most importantly, use the volumes of stock market data. The Smart Score uses that data to rate every public stock against a set of factors that are known to correlate with future stock outperformance; in other words, these factors are good predictors of strong stocks. The results of the Smart Score’s data analysis are presented as a simple score for each stock—a single-digit score on a scale of 1 to 10, with a ‘Perfect 10’ denoting a stock that investors should take a closer look at.

We’ve opened up the TipRanks database to find two of these top-scoring ‘Perfect 10’ shares—stocks that are showing strong bullish indicators for investors. These stocks bring plenty of positive attributes to the table, including ‘Strong Buy’ ratings from analysts. Here are the details.

Pinterest (PINS)

We’ll start our look at ‘Perfect 10’ stocks in the digital world, where Pinterest came on the scene in 2009 with a unique, image-centric approach to social media. The San Fran-based company gives its users online bulletin boards, which can be used to display various types of graphic and/or video content. Users publish and share this content, following the usual social media model; boards can be made public or private, as the owner wishes, and can also be sorted into categories for easier browsing.

Pinterest’s graphic orientation has proven strongly compatible with e-commerce, and Pinterest pages are frequently used as online storefronts by both established merchants and small-time sellers. The company is also making heavy investments in AI technology, applying it to the site’s functionality in user searching and in bulletin board sorting and curation. For business users, Pinterest’s Performance+ bundles both AI and automation features, designed to simplify and boost ad management and campaign creation while maximizing impressions.

The user base for Pinterest skews toward both younger and female users, some 42% of the platform’s global audience hailing from Gen Z and 70% being female. The Gen Z age cohort is Pinterest’s fastest growing demographic, within a user base that is, generally, growing rapidly. At the end of 2024, Pinterest reported its global monthly active users (MAU) had reached 553 million, for year-over-year growth of 11%.

Strong user growth has led to solid revenue and earnings growth – although the Q4 results did not fully meet the expectations. Finishing 2024, Pinterest reported $1.15 billion in revenue for Q4 – a figure that was up 17% year-over-year and beat the forecast by $10 million. Full-year revenue for 2024 came to $3.65 billion, up 19% from 2023. At the same time, Pinterest’s 4Q24 non-GAAP earnings of 56 cents per share, while up 3 cents per share from the prior-year quarter, did miss the forecast by 9 cents.

Looking forward, Pinterest management has presented 1Q25 revenue guidance in the range of $837 million to $852 million, which would represent year-over-year growth of 13% to 15%. In addition, the company has stated that it plans to continue its AI development and related product initiatives, including additional Performance+ functionalities scheduled to be rolled out this year.

This social media company has caught the attention of Benchmark analyst Mark Zgutowicz, who notes that while Pinterest has had its share of troubles in the past, the company is on track for continued gains. The 5-star analyst writes, “We have long been challenged by PINS’ inconsistent engagement and monetization dynamics; however, we believe these forces are now in sync, aided by AI efficiencies and 2.5 years (and counting) of lower funnel product maturation. Said differently, PINS historic (monetization) under indexing of its billions of unique 1P data now looks rearview. While UCAN ARPU has lagged Europe and ROW acceleration the past few quarters, total developed market engagement improvement y/y suggests 1QE’s projected revenue acceleration is not temporary. In addition, Performance+ lower funnel optimization/creative products have yet to monetize, suggesting a P+ call option on a compressed share price.”

Based on his upbeat appraisal of the company, Zgutowicz rates Pinterest’s stock as a Buy, with a $55 price target that points toward a one-year gain of 49%. (To watch Zgutowicz’s track record, click here.)

Pinterest has earned a Strong Buy rating from the analyst consensus, based on 30 recent analyst reviews that include 24 to Buy and 6 to Hold. The shares are currently trading for $36.88 and their $46 average target price implies an upside of 25% on the one-year horizon. (See PINS stock forecast.)

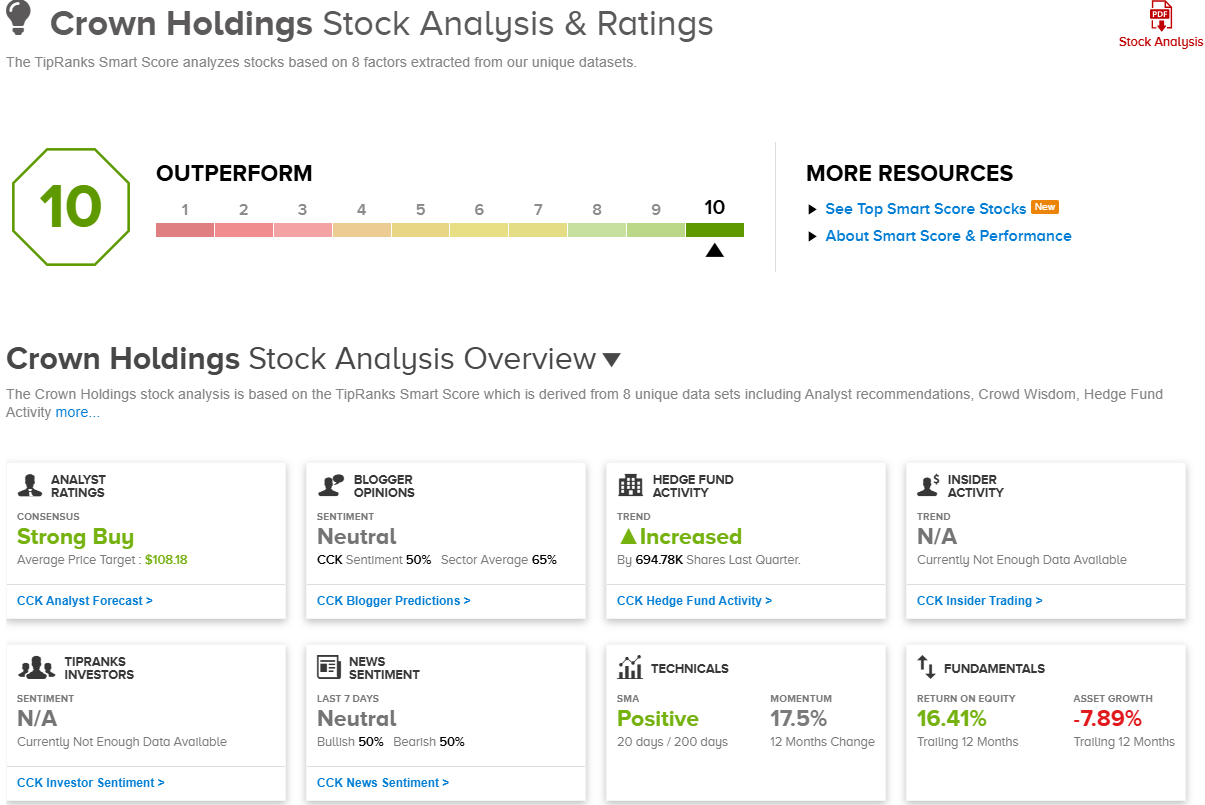

Crown Holdings (CCK)

Next on our list of ‘Perfect 10s’ is a stock that has probably slipped under your radar – but most of us have used its products. Crown Holdings traces its roots back to 1892, and from its Florida headquarters, the company oversees a network of 195 facilities in 39 countries around the world – manufacturing, marketing, and distributing a wide range of metal packaging products, including food and beverage cans, aerosol containers, and various specialty packaging, including metal closures. Crown’s products are widespread – if you’ve ever popped open a beer or a can of soda or opened up a can of soup, there’s a good chance that you’ve used one of this company’s metal cans.

Food packaging is hardly an industry that anyone would ever call exciting, but it is ubiquitous, and a successful packaging manufacturer can build both a solid reputation and a solid sales base. Crown has both.

That is evident in the numbers. In 4Q24, Crown beat the forecasts for both revenue and earnings in the quarter. Quarterly revenue came in at $2.9 billion, for a modest 1.4% year-over-year gain and beating the estimates by $10 million, while the non-GAAP EPS in Q4, at $1.59, was 8 cents better than had been anticipated – and was up 28% year-over-year.

Of particular interest to investors, Crown’s full-year 2024 operating cash flow came to $1.19 billion, and the adjusted free cash flow of $814 million was a company record. Management has stated that it expects the 2025 full-year free cash flow to remain at high levels and expects to see approximately $800 million in FCF this year. In recent years, the company has made a commitment to give cash back to shareholders and in the past year has made a sharp increase in share repurchases.

Analyst Ghansham Panjabi covers this stock for Baird. He has taken note of the company’s combination of modest growth and sound returns – and sees it as an attractive profile. Panjabi writes of CCK, “While the operating model for Crown Holdings is once again gravitating around low growth and productivity/cash flow maximization, we believe that the latter, with an overlay of disproportionate return of cash flow to shareholders 2025 onwards, underpins an attractive and defensive investment profile—with management consistently executing on the operations relative to mixed performance across the peer group… We believe that boring is good in the case of the metal beverage can industry, with Crown in the early stages of returning significant cash to shareholders.”

Panjabi goes on to rate CCK shares as Outperform (Buy), and he puts a $105 price target here, suggesting that the stock has a 19% upside potential for the coming year. (To watch Panjabi’s track record, click here.)

The 12 recent analyst reviews on Crown’s stock break down to 10 Buys and 2 Holds, for a Strong Buy consensus rating. The shares are priced at $88.06 and have an average target price of $108.18, implying a potential one-year upside of 23%. (See CCK stock forecast.)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.

Looking for a trading platform? Check out TipRanks' Best Online Brokers , and find the ideal broker for your trades.

Report an Issue