Heading into the tail-end of 2023, we can start taking an in-depth look at the year’s big winners, the stocks that have shown strong gains through the year so far. Some of these gains are in the triple digits.

But is it wise to buy in after already delivering such huge year-to-date returns? That may seem like investors have missed the boat – except that the data shows that there are stocks with more room to shine, even after the gains they’ve already posted.

The read-outs from the Smart Score tell the story. This is a data collection and collation tool from TipRanks, designed to cut through the noise generated by thousands of traders dealing in thousands of stocks every day. Those tens of million of daily transactions put up a cloud of raw information; the Smart Score gathers it in and uses sophisticated AI-powered algorithms to rate every stock against a set of eight factors, all known to line up with future outperformance.

The result of that is a single score for every stock, a simple rating on a scale of 1 to 10, based on the data, that gives investors an indication of just where that stock is likely to head in the near future. It’s a strong signal for investors to read.

We’ve gotten a start on the stock picking, opening the TipRanks database to find two top-rated stocks, both Strong Buys with solid year-to-date gains, that have earned the ‘Perfect 10’ from the Smart Score. Here are the details, so you can decide if these stocks are right for you.

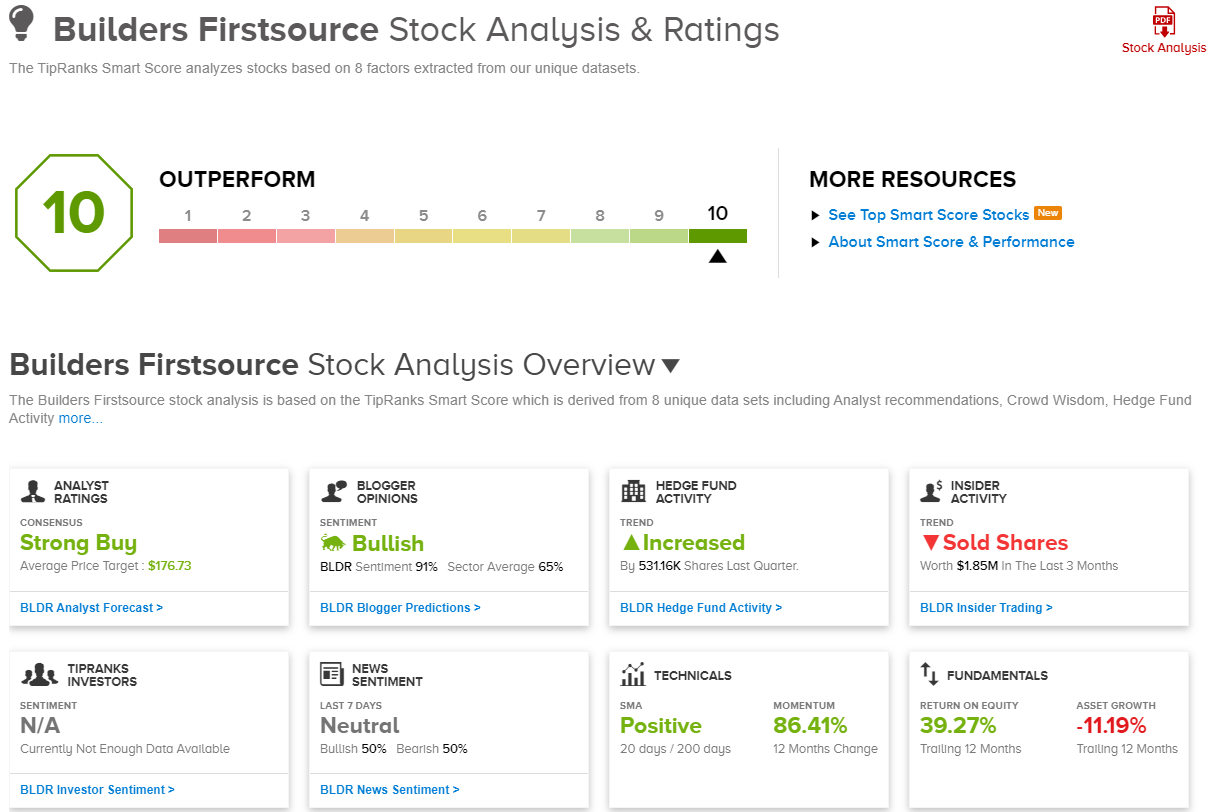

Builders FirstSource (BLDR)

The first stock from our list of Perfect 10s is Builders FirstSource, the largest supplier of structural building products, value-added components, and services in the US market for new residential construction, home repair, and remodeling. The company was founded in 1998, and today operates in 42 states through a network totaling more than 550 manufacturing and distribution locations. Builders FirstSource has the combination of industry expertise, professional talent, and local knowledge necessary to solve its customers’ construction challenges. The company features a number of well-known brands, and boasts it can meet any need, from builders large and small.

Builders FirstSource has shown variable revenues and earnings over the past couple of years, with both typically peaking in Q2 and dropping off in the winter. The company’s most recent quarterly results are from 2Q23, when the top line was $4.5 billion, down 34.6% year-over-year. At the same time, that figure was $290 million above expectations. The firm’s earning’s were reported as a non-GAAP EPS of $3.89 per diluted share. While down sharply y/y, this result was a solid $1.30 better than the forecast. We should note here that, even after recent pullbacks, BLDR shares are up by 78% for this year to date.

In coverage for Barclays, 5-star analyst Matthew Bouley explains why he believes Builders is a solid choice, from its ability to maintain margins to its prospects next year as construction firms work through their backlogs. Bouley says, “On distributors, we continue to prefer BLDR. Though we expect gross margins to normalize into the second half after achieving 35%+ margins last quarter, we still see room for near-term upside particularly as management has consistently managed investor expectations. We think BLDR has proven structurally stronger margins and we expect management to highlight this in the upcoming December Investor Day, as [a] 75 bps move in rates is seemingly causing investors to re-think everything. We also view big builders’ 2024 volume outlooks as a positive read-through for BLDR.”

Looking forward, Bouley goes on to give the shares an Overweight (Buy) rating, with a $175 price target to indicate his confidence in a 50% potential upside on the one-year time horizon. (To watch Bouley’s track record, click here)

Overall, the 11 recent analyst reviews on BLDR include 9 Buys and 2 Holds, to support the Strong Buy consensus rating. The shares are trading for $116.27 and their $176.73 average price target suggests they’ll appreciate by 52% in the coming year. (See BLDR stock forecast)

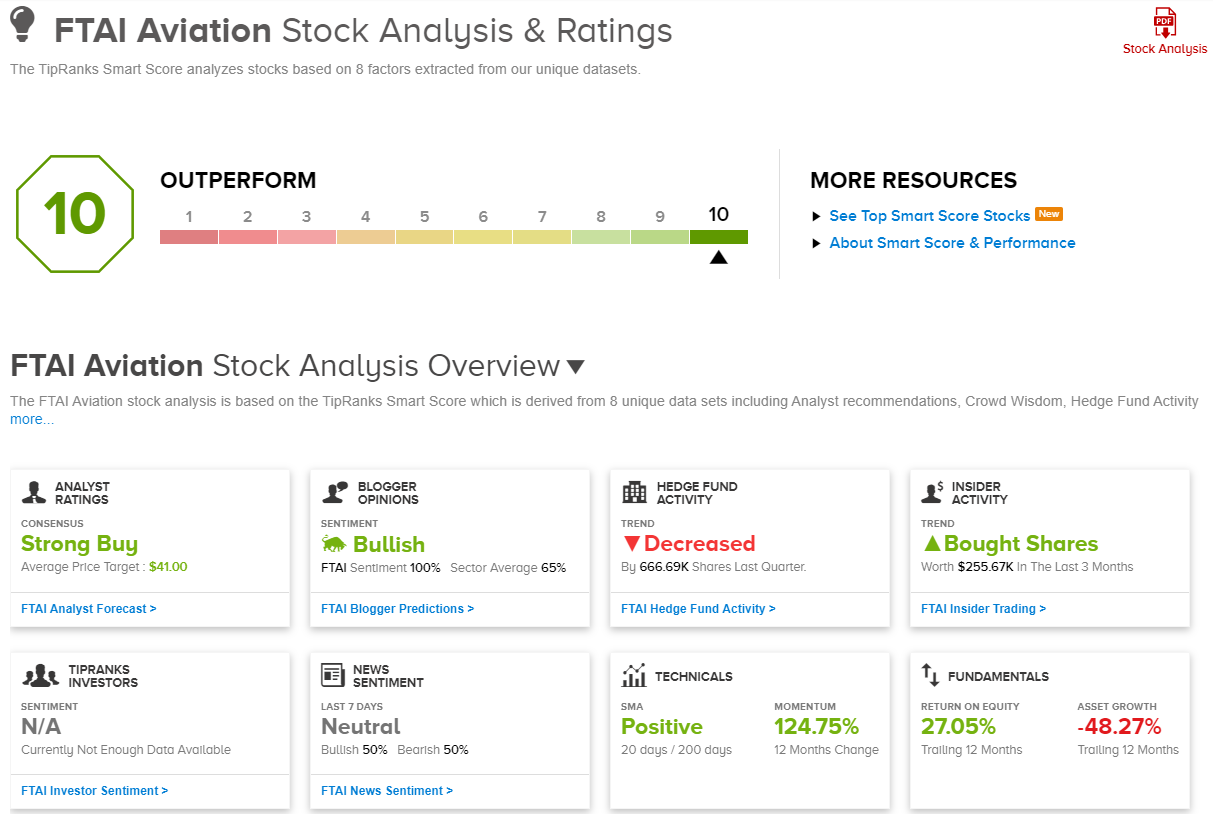

FTAI Aviation (FTAI)

We’ll now shift our focus from construction to the airline industry and take a closer look at FTAI Aviation, formerly known as Fortress Transportation. In addition to the name change, this company had an interesting restructuring in the second half of last year, changing its make-up from a partnership to a corporation, through a merger transaction. The transaction, which was conducted entirely in stock, was closed last November.

In its current form, Fortress Aviation owns and maintains commercial jet engines – specifically, the company is an ‘industry-leading supplier’ of high-end CFM56 engines, modules, materials, and complementary products. The company’s service is designed to ameliorate engine maintenance issues, the costliest burden of aircraft operations. FTAI leases its jet engines to airlines and other commercial jet operators, who can choose from a portfolio featuring more than 200 engine models. In addition, FTAI can lease out several models of 737 aircraft. The business model allows operators to swap out engines and aircraft as needed, avoiding declines in operational tempos.

Since its restructuring, FTAI Aviation’s stock has truly taken off, far outperforming the NASDAQ index where it is listed. Year-to-date, the NASDAQ is up some 30%; FTAI shares have gained much more than that, rising by an impressive 104%.

The share gains have come alongside generally rising revenues and earnings over the past several quarters – although we should note that the most recent quarter reported, 2Q23, showed a potential blip in that trend. In 2Q23 FTAI’s top line came to $274.3 million; this was down from $296.7 million in Q1, and missed the forecast by almost $13 million, nevertheless it was up a hefty 144% year-over-year. At the bottom line, the 46-cent EPS was up from 39 cents in the prior-year quarter, and came in 14 cents per share ahead of the estimates.

The EPS fully covered the company’s 30-cent common share dividend, declared on July 28 and paid out on August 29. The dividend annualizes to $1.20 and yields 3.4%, almost enough to match the current annualized rate of inflation.

Compass Point analyst Giuliano Bologna lays out the bullish case for this stock, pointing out the company’s growth and customer demand as important support: “While FTAI shares have performed extremely well YTD, the potential for PMA approval over the next couple of quarters is a transformative catalyst that could enable a blue sky scenario where FTAI could potentially reach ~$1B of EBITDA in FY26. As a provider of cost and time saving solutions in the CFM56-5B/7B market, the macro backdrop remains favorable due to a shortage of engine supply and continued issues with newer engine variants creating a setup where supply would remain constrained for the next 2+ years.”

Bologna goes on to explain why he believes there is still strong upside left for this stock, writing, “At the same time, FTAI has significantly outperformed expectations in the company’s aerospace products segment which should continue to drive EBITDA growth and improve FCF conversion before potential upside related to PMA… Putting all the pieces together, despite FTAI’s strong performance YTD, we do not believe the current share price reflects the company’s continued outperformance and the potential for a transformative future growth catalyst.”

Quantifying his stance, Bologna rates these shares as a Buy, with a $46 price target that implies a one-year upside potential of 36%. (To watch Bologna’s track record, click here)

FTAI Aviation holds a Strong Buy consensus rating from the Street’s analysts, and it is unanimous, based on 9 recent positive reviews. The shares are trading for $33.87, and their $41 average target price suggests an increase of 21% over the next 12 months. (See FTAI stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.

Questions or Comments about the article? Write to editor@tipranks.com