The last few trading sessions have been harsh, showing sudden, steep losses after some Big Tech earnings reports failed to impress investors. These losses, along with the shift in sentiment, threaten to undermine the generally positive market outlook that was established during the strong bullish run earlier this year.

Discover the Best Stocks and Maximize Your Portfolio:

- See what stocks are receiving strong buy ratings from top-rated analysts.

- Filter, analyze, and streamline your search for investment opportunities with TipRanks’ Stock Screener.

At the same time, not every stock sector is performing poorly. Tom Lee, who is monitoring the situation from Fundstrat, sees evidence that industrial stocks are gearing up for a surge towards the end of the year.

Lee points out a lesser-known factor that supports the case for industrial stocks: The sector’s credit default swaps (CDS) have been outperforming the broader CDS market since last month. This measure reflects liquidity and credit risk and is currently showing strength. Lee notes, “Industrials CDS moves tend to lead Industrial equities by 90 days. Thus, this suggests that we should see relatively improving performance soon.”

However, other factors are also at play, which the TipRanks Smart Score can identify. The AI algorithm collects data from millions of daily stock trades and rates each stock based on eight factors that align with future outperformance. It assigns each stock a single score based on this analysis. The ‘Perfect 10’ score highlights stocks that are poised to surge.

Some of those ‘Perfect 10s’ are industrial-sector stocks, the very area that Tom Lee is telling us to look at. So, let’s use the TipRanks data to look under the hoot at two top-rated industrial stocks, with ‘Perfect 10s’ from the Smart Score and ‘Strong Buys’ from the analysts. Here they are.

Don’t miss

- Bank of America Says Contrarian Buy Signal Could Push Stocks Higher; Here Are 2 Names the Banking Giant Likes Right Now

- Morgan Stanley Predicts at Least 70% Upside for These 2 High-Conviction Stocks — They Have Upcoming Catalysts and Strong Growth Prospects

- ‘Stay Cautious,’ Says Billionaire Leon Cooperman About the Stock Market — Here Are 2 High-Yield Dividend Stocks He’s Using for Protection

Vertiv Holdings (VRT)

First up is Vertiv Holdings, an IT company that offers product lines and solutions in hardware, software, analytics, and service & support, all to enable smooth and continuous operations in its customers’ vital applications. That’s a mouthful, but to make it short, Vertiv solves problems. The company’s products allow customers to meet the challenges inherent in running data centers, communications networks, and commercial and industrial facilities.

The product portfolio that makes this possible includes IT infrastructure, power and cooling solutions, and edge and cloud computing and networking. The Ohio-based company has a truly global footprint, with offices and operations in over 130 countries, and a few numbers will show the scale of its operations.

Vertiv can boast some 750,000 customer sites connected, and it serves more than 75% of the Fortune 500 companies. Its global network includes 24 manufacturing centers, 19 customer experience centers, and 27,000 employees. Intellectual property is important, and Vertiv protects that with 2,740 global patents – and another 770 or more patent applications pending.

That’s the foundation for Vertiv’s business, which has been delivering generally increasing results for investors for the past several years. So far this year, VRT shares are up an impressive 164%, far outpacing the overall markets. In the company’s financial results, both revenues and earnings are trending upward.

For 3Q23, the last quarter reported, Vertiv had a top line of $1.74 billion. While this missed the forecast by $7.6 million (a miss of just 0.4%), the top line was up 18% year-over-year. The firm’s EPS also came in below the forecast, with the 24-cent earnings per share missing by 8 cents. Despite the misses for Q3, Vertiv raised its Q4 revenue guidance to the range of $1.83 billion to $1.85 billion, compared to the Street’s consensus of $1.82 billion.

This stock caught the eye of Deutsche Bank’s 5-star analyst, Nicole DeBlase, who likes the company’s prospects for growth. DeBlase writes, “VRT continues to be one of our favorite ideas within the MI/EE space, given its nearly pure-play exposure to an attractive medium-term data center capex growth trajectory (we continue to project a HSD-LDD revenue CAGR for the foreseeable future) coupled with significant operating margin/FCF improvement opportunity. Our model forecasts 20%+ average annual EPS growth through 2025, the highest within our coverage universe by far. And yet the stock is now trading in line with the MI/EE peer group, at ~18x 2024 consensus EPS. We view today’s underperformance as a buying opportunity.”

DeBlase quantifies this buying opportunity with a Buy rating on Vertiv shares and a $48 price target that suggests a one-year upside potential of 33%. (To watch DeBlase’s track record, click here)

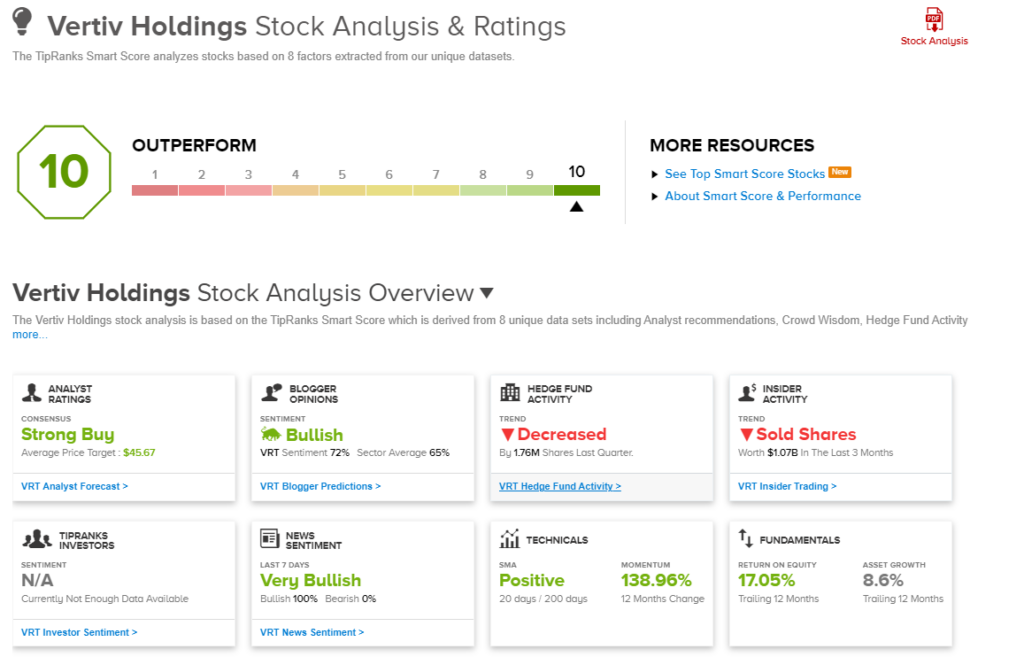

When we turn to the Smart Score, we find that Vertiv has bullish sentiment from the Wall Street analysts. The stock gets a Strong Buy consensus rating, based on 8 analyst reviews that break down 7 to 1 in favor of Buys over Holds. The shares are selling for $36.18 and their $45.63 average price target implies a gain of 26% in the next 12 months. (See Vertiv stock analysis)

CECO Environmental (CECO)

The second ‘perfect 10’ stock is CECO Environmental, a ‘new tech’ firm that is developing and creating the technologies we’ll need to control environmental air pollution, promote clean and efficient energy, and maintain environmentally sound handling and filtration of various fluids. CECO also offers on-site installation of these technologies and support to maintain them in practical use. The company boasts a wide-ranging customer base, including firms in the aerospace, automotive, cement, chemicals, and fuel sectors, and its products are even found in specialty niches like noise control and glass manufacturing.

Last month, CECO announced it had completed its acquisition of Kemco, a water recycling and energy conservation firm. The Kemco move was completed on August 23 and brings a new set of services and solutions into CECO’s portfolio. Based on the acquisition and Kemco’s ability to generate results through its existing network, CECO revised its 2023 full-year revenue guidance upward to $525 million. Hitting that level will give CECO 24% year-over-year top-line growth.

So, CECO is a tech/industrial firm with plenty of potential for investors. The last reported set of quarterly results bears this out. For 2Q23, the bottom-line earnings, at 15 cents per share by non-GAAP measures, were in line with expectations. At the top line, however, the company reported revenue of $129.2 million, $11.4 million better than expected and some 23% up from the prior-year result. The company’s revenue gains were powered by a 44% year-over-year increase in quarterly orders, totaling $162.9 million, and looking ahead, CECO has a work backlog totaling $391 million.

On the analyst side, Aaron Spychalla from Craig-Hallum, lays out several reasons to feel upbeat on this stock: “CECO continues to build a more predictable, diversified, and higher-margin business targeting clean air, clean water, and the energy transition and pursues its goal of $600M+ in revenue and 15%+ EBITDA margin in 2025…”

“With strong fundamentals and increased visibility into continued improvement, a combination of company-specific and secular growth drivers (reshoring/re-industrialization, energy transition, stricter regulatory standards, still early in CHIPS Act and Infrastructure Bill funding), a strong leadership team and reinvigorated culture, a manageable balance sheet and prudent capital allocation, and modest valuation (on numbers that likely continue to prove conservative, in our view), we reiterate our Buy rating and continue to see opportunity for a much larger stock over time,” Spychalla added.

This Buy rating is backed up by a price target of $23, implying an upside potential of 47% in the year ahead. (To watch Spychalla’s track record, click here)

Overall, this company’s ‘Perfect 10’ Smart Score receives strong support from Wall Street. CECO gets a unanimously positive Strong Buy consensus rating, based on 5 recent ‘Buy’ analyst reviews. The $15.65 trading price here is complemented by a $21.20 average target price; together they point toward a 35% upside potential. (See CECO stock analysis)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.