The markets are doing well in November. Powered by the conclusion (albeit controversial) of the election results and by the enthusiasm around potential vaccine for COVID 19, the S&P 500 soared more than 10% this month.

Are there any more high profile news stories left to drive the markets higher or do we go down from here?

According to Marko Kolanovic, JPMorgan’s global head of macro quantitative and derivatives strategy, there is plenty of room for the market to run. The strategist described the election outcome of a Democratic president and Republican controlled Senate as “likely the best of both worlds for stocks.” A Joe Biden presidency means investors can anticipate an easing of the trade wars while a Republican controlled Senate will likely keep President Trump’s business-friendly policies in place.

To get a head start on the anticipated market strength ahead we tapped three JPMorgan analysts who are recommending three stocks that they believe are poised to go higher. We also ran the three through TipRanks database to see what other Wall Street’s analysts have to say about them.

Aligos Therapeutics (ALGS)

To start us off we have Aligos Therapeutics, a biotechnology company that develops medications for liver and viral ailments with a focus on curing chronic Hepatitis B (CHB). CHB is still a widespread cause of liver disease despite modern society’s growing rates of immunization.

J.P. Morgan analyst Eric Joseph takes the view that the company’s Phase I drug candidate ALG-010133 is a possible game changer, “we see Aligos’s clinical-stage STOPs platform on a compelling, differentiated path toward the goal of bringing functional cures to a majority of CHB patients.”

Joseph acknowledges that there is work to do and there are challenges along the road, however, the analyst believes the company is on the path to achieving success.

“Meeting this goal is likely to take a multi-modal combination approach. With a diversified pipeline targeting various points of the HBV lifecycle (multiple candidates with best-in-class potential), we see Aligos having the greatest flexibility in developing and commercializing a curative treatment regimen,” Joseph wrote.

The analyst concluded, “Backed by favorable preclinical data for its CAM (‘184) and ASO/siRNA (‘572/‘097) molecules, we see a strong positioning for the planned combo regimen.”

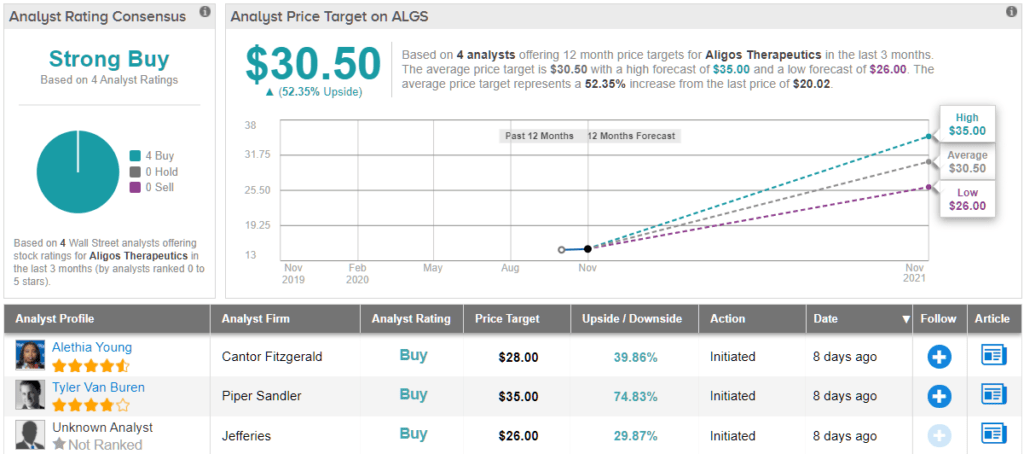

To this end, Joseph rates ALGS an Overweight rating (i.e. Buy) along with a $33 price target. This translates to a healthy 65% upside potential for the next 12 months. (To watch Joseph’s track record, click here)

The rest of the street is on board with Joseph’s opinion. 4 Buys and no Holds or Sells add up to a Strong Buy consensus rating. The average price target of $30.50 provides upside potential of 52%. (See ALGS stock analysis on TipRanks)

Plantronics (PLT)

Next up we have electronics company Plantronics, operating under the Poly brand, which provides business and personal headsets as well as video-conferencing technology.

Plantronics has taken shareholders on a roller coaster ride this year, with shares plunging as much as 80% between January and March, before surging a whopping 310% in the following months.

The stock is now on the positive side of that trend following tremendous second fiscal quarter results. Specifically, the company reported adjusted EPS of $0.93, which beat the consensus earnings estimate by a huge 107%.

Among the fans is J.P. Morgan analyst Paul Coster who sees more growth ahead.

“PLT is seeing strong demand for headsets for work-from-home, remote learning, and remote healthcare administration. The surprising recovery in headset demand in June quarter carried over into F2Q21 and the F3Q guide points to a return to about 10% year over year growth,” Coster noted.

Another important factor which has the J.P. Morgan analyst bullish on the stock is the company’s performance under the new CEO.

“The firm seems to be turning a corner, capitalizing on demand, re-engaging with the channel, resolving supply chain constraints, cutting costs and prioritizing the repayment of debt […] “We are incrementally constructive on the story owing to strengthening demand for the company’s,” the analyst concluded.

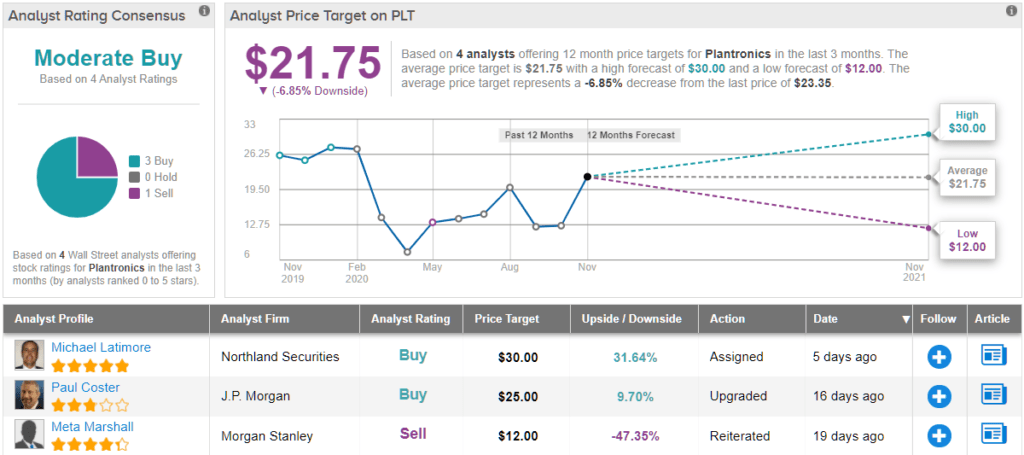

It’s not surprising, then, why Coster rates PLT an Overweight (i.e. Buy). The analyst has a price target of $25 which implies a modest 7% upside. (To watch Coster’s track record, click here)

Turning to the rest of the Street, the opinions are mixed. 3 Buys and 1 Sell assigned in the last three months add up to a Moderate Buy consensus rating. The average price target is $21.75, which is below the current price of $23.35 (See PLT stock analysis on TipRanks)

Eargo (EAR)

Last but not least we have Eargo, which sells in-ear canal hearing aids in the US. The company sells its products directly to consumers through its website.

J.P. Morgan analyst Robbie Marcus is excited about Eargo’s future prospects, predicting a handsome 5-year CAGR of about 40%. The 5-Star analyst believes the company’s technology is quite simply better than the competition.

“…when choosing a hearing aid, consumers are often forced to make trade-offs between a more discreet in-ear option that distorts sound quality and is generally uncomfortable or a behind-the-ear option with better acoustics.The Eargo solution, however, marries near-invisibility with a feature-rich offering,” Marcus commented.

Moreover, the J.P. Morgan analyst is of the opinion that Eargo’s direct to consumer business model gives it a leg up on the competition: “This model allows the company to generate above-average industry margins as the only vertically integrated DTC hearing aid company by eliminating the significant mark-ups that audiologists normally charge.”

The US hearing aid market is about $30 Billion so there is lots of room to expand. In addition, Eargo will benefit from the growth in online sales. The J.P. Morgan analyst pointed out, “With strong adoption trends heading into COVID-19, and now a significantly faster migration online in today’s environment, we see a clear path for Eargo to grow at the upper end of its high-growth peers.”

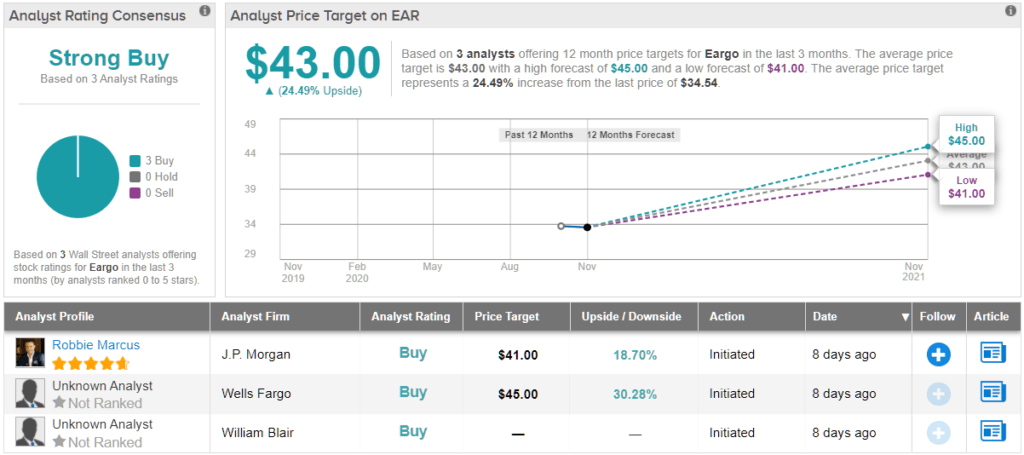

Based on the above, Marcus recently initiated coverage on Eargo shares with an Overweight (i.e. Buy) rating and a $41 prices target, representing upside potential of ~19%. (To watch Marcus’ track record, click here)

There are two other analysts who cover the company and both are in agreement with Marcus. 3 Buys and no Holds or Sells add up to a Strong Buy consensus rating. The average price target of $43 implies a potential upsisde of 24%. (See Eargo stock analysis on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.