The markets are on a solid upward trend this year, with the S&P 500’s year-to-date gain nearing 16%. Improved investor sentiment has been fueling the gains – but behind that, strategists are seeing a set of important tailwinds.

Maximize Your Portfolio with Data Driven Insights:

- Leverage the power of TipRanks' Smart Score, a data-driven tool to help you uncover top performing stocks and make informed investment decisions.

- Monitor your stock picks and compare them to top Wall Street Analysts' recommendations with Your Smart Portfolio

According to Evercore ISI’s chief equity strategist, Julian Emanuel, these include general economic resilience, sound corporate earnings, the expanding AI boom, and the combination of slowing inflation and the consequent shift by the Federal Reserve toward interest rate cuts. Emanuel sees these factors pushing the S&P up to 6,000 by year’s end, a jump of ~9% from current levels.

The clear bullish trend is fueling a growing investor appetite for risk – a willingness to take longer chances in pursuit of solid rewards. This sentiment could prove especially beneficial for higher-risk stock segments, particularly penny stocks. Priced below $5 per share, these low-cost stocks embody risk/reward calculations and offer potential for substantial returns.

While incredibly enticing, Wall Street analysts recommend doing some due diligence before taking action, noting that not all penny stocks are bound for greatness.

Bearing this in mind, we’ve used TipRanks’ database to uncover two compelling penny stocks that have earned Strong Buy ratings from the analyst community. According to the pros, these tickers may rally as high as $10 – or even more. We’re talking about triple-digit upside potential here.

Poseida Therapeutics (PSTX)

We’ll start with Poseida, a clinical-stage biotherapeutic company focusing on new treatments for various cancers and rare diseases. Poseida is advancing differentiated treatments, intended to set new paradigms for life-threatening conditions with high unmet medical needs. The company sees cell and gene therapies as the future in the medical field, and is working to realize it now.

Poseida is advancing its pipeline with a focus on hematologic (heme) malignancies and solid tumors. Under heme malignancies, the company is advancing two phase 1 therapies in collaboration with Roche: P-BCMA-ALLO1 for multiple myeloma and P-CD19CD20-ALLO1 for B-cell malignancies. Clinical updates for both are expected in the second half of 2024, pending coordination with Roche. For solid tumors, Poseida is conducting a phase 1 study of P-MUC1C-ALLO1, an allogeneic CAR-T therapy for advanced or metastatic solid tumors, with a clinical update slated for the second half of 2024.

In an important development, Poseida announced last month that it had entered into a new collaboration and license agreement with Japanese pharmaceutical giant Astellas for the development of novel CAR-T therapies against solid tumor cancers. The terms of the agreement, which Astellas will conduct through its Xyphos subsidiary, involve a $50 million upfront fee to Poseida. Astellas has pledged up to $550 million in contingent payments for development and sales. Poseida also stands to receive tiered royalties on net sales.

This agreement marks the second such deal between Poseida and Astellas. The previous agreement, dating to August of last year, involved a $50 million investment in Poseida, to support earlier work in cancer cell therapeutics.

The partnership programs are important revenue drivers for Poseida, which reported bringing in $95 million in total milestone payments during the first quarter of this year.

Standing squarely in the bull camp, 5-star analyst Justin Zelin, of BTIG, cites several reasons to support his optimistic stance.

“A combination of multiple advantages through all parts of the gene modification process (insertion, editing, delivery, and manufacturing) along with multiple pipeline programs makes Poseida a differentiated CAR-T company with runway for partnerships, licensing, and development of potentially best-in-class CAR-Ts and in our view an exciting long-term play in cell and gene therapy,” Zelin opined.

“In a macro environment where we see large pharma players pulling out of cell therapy deals, we see PSTX’s second deal with Astellas speaking to the potential of the co’s allogeneic T cell therapy platform and potential in solid tumors while extending PSTX’s cash runway through non-dilutive financing,” the analyst added.

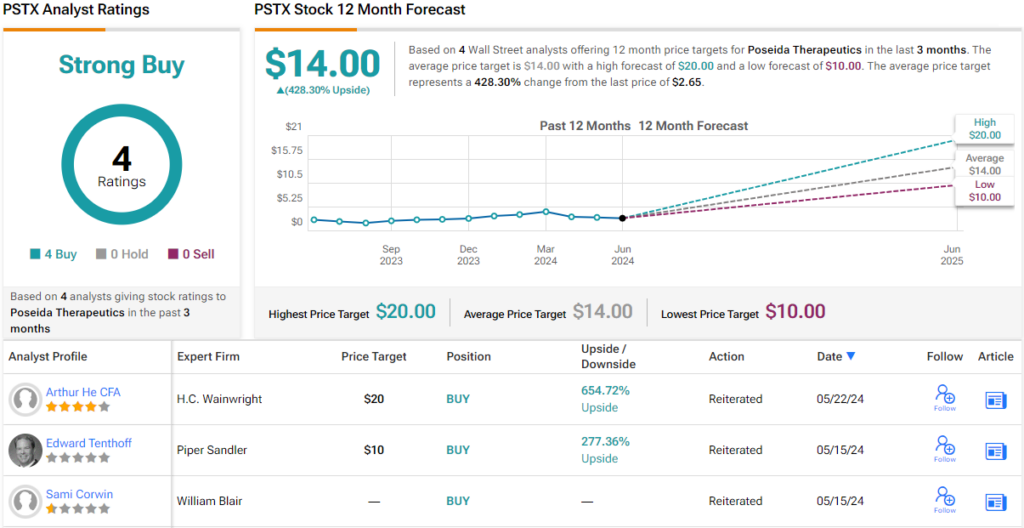

These factors induced Zelin to give PSTX stock a Buy rating, and his $12 price target implies that the shares will gain ~353% in the next 12 months. (To watch Zelin’s track record, click here)

Overall, Wall Street is bullish on this biotech. PSTX stock has 4 recent positive reviews, for a unanimous Strong Buy consensus rating, and the $14 average price target suggests a one-year upside of 428% from the current $2.65 trading price. (See PSTX stock forecast)

Rezolute (RZLT)

Next, we have Rezolute, a clinical-stage biopharmaceutical company dedicated to developing new medications for the treatment of debilitating metabolic diseases. The company is following novel approaches to overcome the deficiencies in current treatment regimens, with the long-term aim of improving clinical outcomes for patients suffering from severe disease conditions.

Currently, the company is working on treatments for two conditions – diabetic macular edema (DME) and hyperinsulinism (HI). The first of these is a serious, vision-threatening complication caused by diabetes – and is a leading cause of blindness in diabetic patients. Rezolute is working on a new drug candidate, RZ402, to treat this condition. The second indication in the company’s pipeline, HI, is often associated with Type 2 diabetes; it is characterized by higher-than-normal levels of insulin in the bloodstream and can severely affect the patient’s ability to properly metabolize sugars. Rezolute is working to treat two types of HI, congenital and tumor, with the drug candidate RZ358.

On May 21 of this year, the company released important data from the Phase 2 proof of concept study of RZ402. This drug, targeting DME, met the primary study endpoints and showed a good safety profile. The study data showed a significant reduction in central subfield thickness – that is, reversal of DME damage to the retina – in patients ‘who are naïve to or have received limited anti-vascular growth factor (anti-VEGF) injections.’ RZ402 is the first oral therapy to demonstrate such a reduction in clinical signs of DME.

In another important development, Rezolute has started enrolling patients in the Phase 3 sunRIZE clinical study, a trial of RZ358 in patients with congenital HI. The company expects to have topline data from the study available for release in the middle of next year.

In short, Rezolute is a clinical-stage biotech with two promising drug candidates moving through the pipeline – and that attracted the attention of Craig-Hallum analyst Albert Lowe.

“We view lead asset RZ358 as a novel therapy with a significant opportunity in congenital hyperinsulinism (CHI)… Phase IIb data showed robust efficacy with favorable tolerability that gives confidence to a positive outcome in the Phase III sunRIZE study, which is ongoing in ex-US geographies. In our view, RZ358’s risk/benefit profile supports lifting the partial clinical hold to allow enrollment in the US, and notwithstanding, we believe the RZLT shares are undervalued considering RZ358’s ex-US CHI opportunity along with WW tumor hyperinsulinism,” Lowe opined.

He added, turning to RZ402, “In addition, we believe clinical proof of concept data supports RZ402’s potential to shift the treatment paradigm for DME as an oral plasma kallikrein inhibitor. We see opportunity for continued share appreciation driven by positive clinical and regulatory milestones.”

This is a sound foundation for Lowe’s Buy rating here, and his $14 price target suggests that the stock will appreciate by ~265% by this time next year. (To watch Lowe’s track record, click here)

Overall, there are 6 recent analyst reviews here, all positive, giving RZLT shares a Strong Buy consensus rating. The stock’s average price target of $10.33 implies a 169% upside potential from the current trading price of $3.84. (See RZLT stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.