Let’s talk about finding returns – the primary goal of every investor in the market. At base, there are two ways to set up a profitable stock portfolio. Investors can seek stocks poised for appreciation, or those providing reliable income through dividends. Preferably, investors can find both.

Discover the Best Stocks and Maximize Your Portfolio:

- See what stocks are receiving strong buy ratings from top-rated analysts.

- Filter, analyze, and streamline your search for investment opportunities with TipRanks’ Stock Screener.

Watching current market conditions for Bank of America, analyst Noah Hungness is recommending two dividend stocks that look attractive right now. Notably, both stocks have recently dipped from their peak 52-week values, presenting an attractive combination of dividend yield and potential for upside, bolstered by discounted pricing.

We’ve used the TipRanks database to look up the broader Street-level view on Hungness’ picks and found that both get ‘Strong Buy’ ratings – and that both are offering double-digit upside potential. Here are the details.

Permian Resources (PR)

The first stock we’ll look at is Permian Resources, one of the many independent oil and natural gas exploration and production companies working the Texas oil patch. Permian’s name is the giveaway here; the company is one of the largest of the pure-play E&P’s in the rich Permian Basin, the geological formation that, in recent decades, has put Texas back on the world map of energy producers. Permian Resources holds extensive acreage – on the order of 400,000 net leasehold and 68,000 royalty acres – in the Midland Basin of the larger Permian, and in the Delaware Basin that straddles the Texas-New Mexico boundary.

Permian focuses on acquiring and developing high-return oil and gas properties within these formations, with the goal of driving returns for investors. The company uses a combination of technical expertise and operational flexibility to ensure that its holdings are optimized to generate those high returns over a productive lifespan, seeing this approach as the key to a successful and disciplined operation. Permian Resources is based out of Midland, Texas, and boasts a market cap of nearly $12 billion.

In its last reported quarter, 1Q24, Permian described its results as ‘strong,’ with a top line of $1.24 billion. This was up 101% year-over-year, and beat the forecast by $30 million. At the bottom line, EPS of $0.25 was less impressive, missing the forecast by 14 cents per share.

These numbers were supported by strong increases in oil and natural gas output from the prior year. In 1Q24, Permian reported crude oil production of 151.8 MBbls/d, and a total average production (oil and natural gas) of 319.5 Mboe/d. These figures were approximately double the production reported in 1Q23.

Permian has a commitment to capital returns for shareholders, and in Q1 the company spent $31 million to buy back 2 million shares – and increased the dividend payment. The base dividend was bumped up by 20% to 6 cents per common share, and was paid out on May 29 in tandem with a variable dividend of 14 cents per share. The combined 20-cent payment gives an annualized rate of 80 cents, and a yield of 5.2%, well above the current rate of inflation. The company has a history of paying out variable dividends alongside its regular dividend payment.

We should note here that Permian’s stock is down 16% from the 52-week peak value it reached in April of this year. A chunk of that slide occurred after the company announced, on May 13, a secondary stock offering totaling more than 51 million shares by several large private shareholders.

Turning to the Bank of America view, we find that analyst Hungness is upbeat, noting multiple advantages in the company’s business operation. He writes, “We believe the combination of PR’s operational execution, premium multiple, and low leverage has positioned the company well to continue its consolidation strategy but the company has seen a recent pull back… that we see providing an attractive entry point to the best performing stock in the sector since the start of 2023.”

Hungness also notes that Permian has been realizing benefits from its acquisition, last year, of Earthstone, and sees the company in a position to continue realizing financial windfalls from M&A activity: “Meanwhile accretive M&A has helped grow production and deepen inventory most notably with the $4.5bn Earthstone acquisition that added 133 kboed (41% oil)… given how unconsolidated the Delaware is we see potential for deals to continue adding runway around PR’s core acreage.”

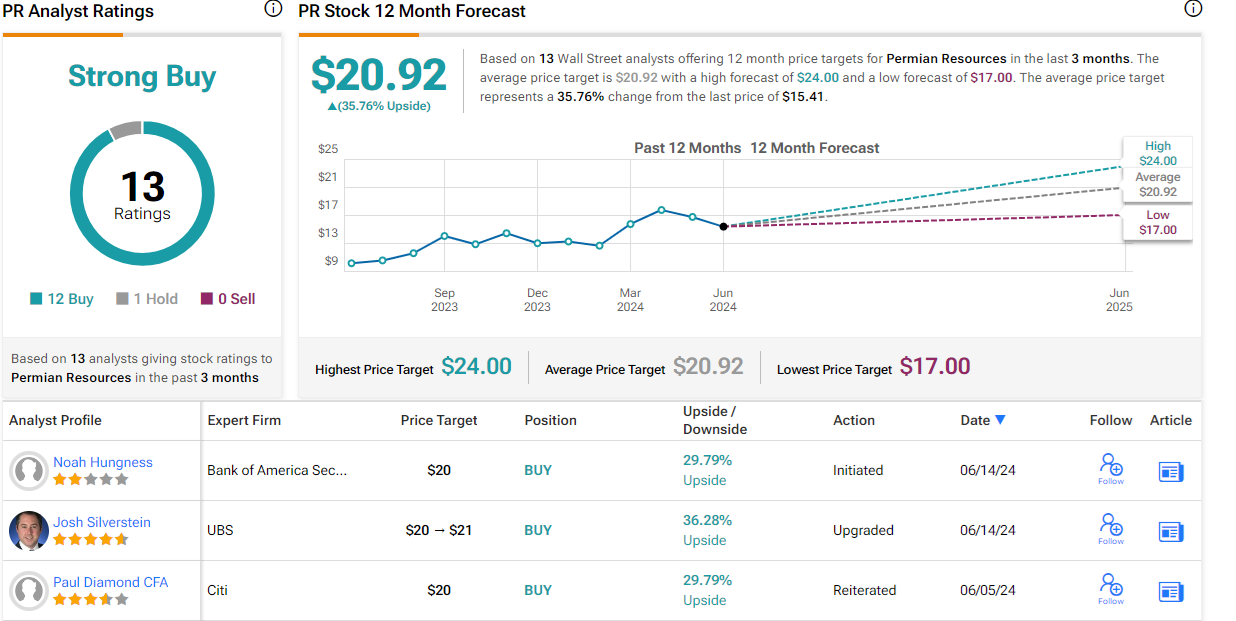

For Hungness, these factors add up to a Buy rating for this stock, and he puts his price target at $20, implying that the shares will gain 30% in the next 12 months. (To watch Hungness’s track record, click here)

Overall, the Strong Buy consensus rating on Permian Resources is derived from 13 recent analyst reviews – that break down to a lopsided 12 Buys and 1 Hold. The shares are priced at $15.41 and their $20.92 average price target suggests a one-year upside potential of 36%. (See Permian’s stock forecast)

Chord Energy (CHRD)

Next up is Chord Energy, an oil and gas company operating in the northern part of the Great Plains. Specifically, Chord holds more than 126,000 net acres in the Bakken Shale of the larger Williston Basin formation, the oil-rich production region that has made North Dakota a major player on the global energy scene. Chord’s holdings are located mainly in the Bakken of North Dakota but extend southward into the larger Williston and westward into Montana.

Chord’s operating model is based on high-quality assets and a low break-even price. The company has 6 operating rigs on its holdings, and some 57% of its proven reserves are made up of crude oil. During 1Q24, the last period reported, the company’s 99 MBopd exceeded the top end of the previously published guidance. Total production in the quarter came to 168.4 MBoepd. That total included 58.8% crude oil, with the remainder being natural gas and natural gas liquids.

Revenues in the quarter came to $1.09 billion, beating the forecast by over $323 million and growing more than 21% year-over-year. Likewise at the bottom-line, non-GAAP EPS, at $5.10 per share beat expectations by $0.34 and was up 13.5% from 1Q23.

Additionally, Chord has now completed its previously announced acquisition of the Canadian oil and gas firm Enerplus. The transaction’s completion was announced on May 31. This merger boosted Chord’s total Bakken acreage to 1.3 million.

Looking at the dividend, we find that Chord declared a combined base and variable payment of $2.94 per common share ($1.25 base, $1.69 variable) on May 7, which was paid out on June 5. The total dividend annualizes to $11.76 per common share and gives a high yield of 7.15%. We can note here that shares in Chord are down 13.5% from the peak reached this past April.

Analyst Hungness specifically notes the share price decline as a reason for investors to buy in, pointing out that it gives the stock a relative discount price. He says of Chord, “Shares have pulled back with the oil price creating an attractive buying opportunity into a core E&P name. CHRD is currently trading at 3.6x 2025 DACF, compared to the peer average of 4.7x. While CHRD doesn’t fit our oil growth thematic, and is focused on holding production flat for the next ten years, at this level, shares offer compelling risk reward with operational upside catalysts. Post-Enerplus combination, CHRD has a larger platform to push the limits of capital efficiencies, where its track record in recent years stands out. In our view, its scale and reputation as an operator lays the foundation for (more) potentially accretive M&A.”

Hungness quantifies his stance with a Buy rating on CHRD, and his price target of $201 points toward a one-year gain of 22%.

The broader view of these shares on Wall Street is somewhat more bullish. The Strong Buy consensus rating is unanimous, based on 9 positive reviews set in recent weeks, and the $219.56 average price target implies a 33.5% one-year upside from the current trading price of $164.49. (See CHRD stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.