What do you get when you combine beaten-down stock prices with an economic and technological niche poised to gain as it becomes ever more essential? You get stocks with a low cost of entry – plus high upside potential and approval from Wall Street’s analysts.

Invest with Confidence:

- Follow TipRanks' Top Wall Street Analysts to uncover their success rate and average return.

- Join thousands of data-driven investors – Build your Smart Portfolio for personalized insights.

The niche we’re talking about is AI, artificial intelligence, once a pipe dream of science fiction but today a computing technology that is growing ever more important. AI powers the rapidly expanding Internet of Things, is the technology behind game changers like 3D printing, and has already transformed the world of online marketing. In its application to autonomous vehicles, it even promises to forever change the way we travel. No matter where you go, you can’t get away from AI.

The beaten down prices are an artifact of the current bear market and the lingering supply chain snarls. We’ve been facing a semiconductor chip shortage since last year, and it’s been affecting everything from heavy industry to health care to high-end computing. But the supply issues are starting to sort themselves out, and demand for AI-related tech remains high.

So let’s take a dive in, and look at some artificial intelligence stocks that are primed for growth in the months and years ahead – and whose prices now represent a low point of entry. We’ll take the latest data from the TipRanks platform, add in the analyst commentary on these stocks, and get a full picture.

Nvidia Corporation (NVDA)

First up is Nvidia, one of the chip industry’s major names. Nvidia has long been known for its high market share – better than 80% – in the graphics processing unit (GPU) segment, an important coup for this company, as high-end GPUs are in high demand. The chips, which were originally designed to allow sharper, more realistic graphics for computer games, have found applications in plenty of other sectors, where their high computing capacity has enabled AI and machine learning tech in data processing, medical imaging, smart home and city tech, and autonomous machines.

Nvidia has customers in all of those areas, and the autonomous machines – especially vehicles – proved to be a bright spot in the company’s recent fiscal 2Q23 earnings report. The quarter, which ended on July 31, saw Nvidia’s revenues and earnings both fall off sharply from Q1, but drilling down shows that the company’s news had some positive aspects, too.

At the top line, revenues dropped sequentially from $8.3 billion to $6.7 billion. At the same time, the Q2 results were still up 3% y/y. Earnings, however, did not fare so well. Non-GAAP diluted EPS fell q/q from $1.36 to $0.51, were down y/y by 51%. And that’s only part of the bad news.

Nvidia’s revenue was well below the $8.1 billion expectation, a miss that has been attributed to contractions in the computer gaming segment. And the company pulled back on its Q3 guidance, spooking investors – and prompting a sharp drop in the stock post-earnings release.

On the positive side, Nvidia saw large gains in its Data Center and Automotive segments, both areas in which the company’s high-end, AI capable chips have strong potential to expand market share – they offer strong computer capacity, backed by a company with a reputation for delivering quality in these areas in particular. Data Center revenue rose to $3.81 billion in fiscal Q2, for a y/y gain of 61%. The company’s automotive business is smaller, generating Q2 revenues of $220 million – but that was up 45% y/y and 59% q/q, showing not just gains, but accelerating gains.

Truist’s 5-star analyst William Stein acknowledges Nvidia’s slip in gaming revenue, describing it as ‘bitter medicine,’ but recommends the stock for its AI leadership. He writes, “Bears will focus on the potential for weakness to spread to datacenter. We acknowledge this possibility, but continue to see NVDA as the best positioned to capture share in the datacenter long-term, because its GPU leadership is sticky, and its newer products (DPU & CPU) align with emerging disaggregated compute architectures…. In CQ2, Automotive revenue of $220m grew by ~45% y/y and set an all-time high. Management noted strength driven by self-driving and AI cockpit solutions, partially offset by a decline of legacy cockpit revenue. The long-awaited growth in NVDA’s automotive business finally appears to be materializing. Datacenter revenue was also strong, driven by demand in vertical markets and North American hyperscale customers.”

Along with an upbeat outlook, Stein gives NVDA shares a Buy rating; his $198 price target implies a one-year upside potential of 50%. (To watch Stein’s track record, click here.)

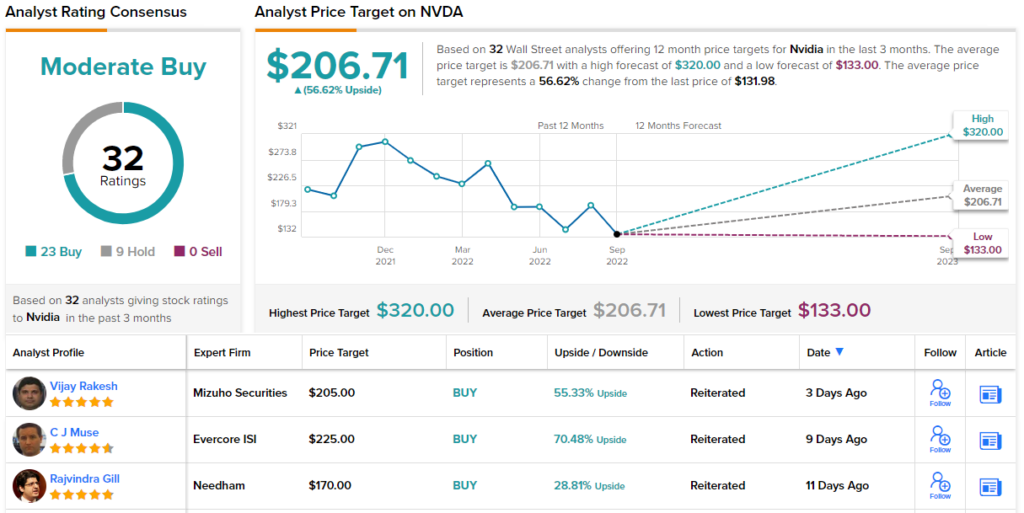

Turning now to the rest of the Street, where the stock has 31 reviews on file, with 23 Buys weighed against 9 Holds for a Moderate Buy consensus rating. Nvidia shares are selling for $131.98 and their $206.71 average price target indicates potential for 57% improvement in the next 12 months. (See Nvidia’s stock forecast at TipRanks.)

Marpai, Inc. (MRAI)

From semiconductor chips we’ll move to the health care sector, where tech firm Marpai has seen an opportunity to bring AI tech into the third-party administrator (TAP) segment of the field. This is a $22 billion market, and Marpai uses AI to design system features that will elevate care quality while reducing claims cost and lower the stop-loss premiums. Marpai’s approach to TAP is based on the use of proprietary predictive algorithms to streamline processes.

This health admin tech firm is relatively new to the public markets, having held its IPO just at the end of October last year. The offering, which opened on the 27th and closed on the 29th of the month, sold over 7.1 million shares for $4 each, and raised $28.75 million in gross proceeds, exceeding the $25 million originally planned for. Since the IPO, however, the stock has fallen by 78%.

Marpai has released 4 quarterly financial reports since going public, and shown a top line consistently between $4.8 million and $6.2 million. The most recent report, for 2Q22, showed revenues of $5.6 million, in the middle of that range – and slightly above expectations. On earnings, the company reported a net loss of $6.66 million, or 34 cents per diluted share. On a per-share basis, this was a significant improvement over the 54-cent diluted EPS loss recorded a year prior.

Giving Marpai an in-depth look, analyst Allen Klee of Maxim Group describes both the company’s product innovation and its potential: “MRAI is well-positioned to drive innovation in the third-party administrator (TPA) space. Employers that self-insure their employees’ healthcare can use Marpai to process claims and administer benefits. The company’s technology uses artificial intelligence (AI) to predict and mitigate potential high-cost health events, as well as to auto-adjudicate claims, reducing costs. Technology can also reduce waste in the system by steering members to the most cost-effective providers ahead of time. Through these efficiencies and by cutting out excess expenditures from traditional healthcare plans, Marpai believes employers can reduce healthcare costs by over 25%.”

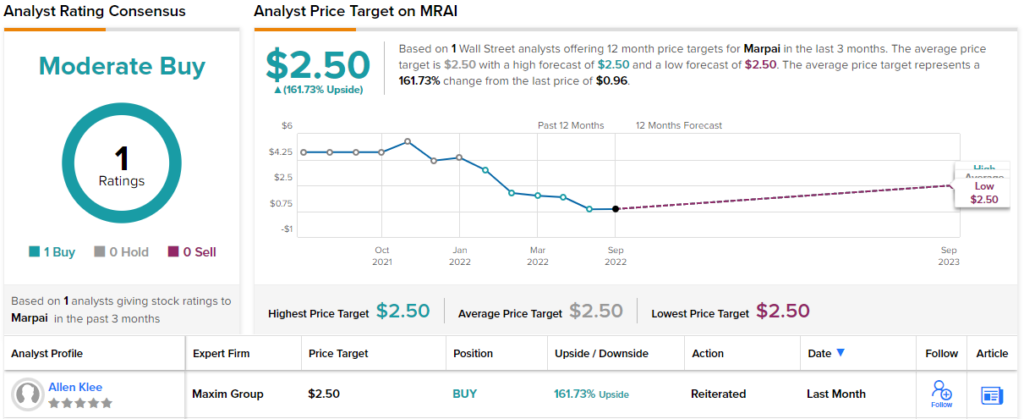

Believing that Marpai can deliver for investors, Klee rates the shares as a Buy, and his 12-month price target of $2.50 implies a robust gain of 162%. (To watch Klee’s track record, click here.)

Some stocks fly under Wall Street’s radar and Marpai appears to be one such name; Klee’s is the only analyst review posted over the past 3 months. (See Marpai’s stock forecast at TipRanks.)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.