The York Water Company (YORW) makes for a unique opportunity in the water industry. The company boasts the achievement of being the oldest investor-owned water utility in the United States, having served its local population continuously since 1816. The company operates entirely within the Pennsylvanian counties of of York, Adams, and Franklin, with an estimated 200,000 customers.

Discover the Best Stocks and Maximize Your Portfolio:

- See what stocks are receiving strong buy ratings from top-rated analysts.

- Filter, analyze, and streamline your search for investment opportunities with TipRanks’ Stock Screener.

Talking about the achievements, York Water features a remarkable record of over 200 years of uninterrupted dividend payments to shareholders. The company has been able to forge this legendary dividend track record over the centuries due to the predictable and stable cash flows enjoyed by the participants of the water industry.

While the company’s dividend growth prospects remain robust, I believe that investors have overvalued York Water’s shares. For this reason, I am neutral on the stock.

Latest Results

York Water’s latest results once again displayed the company’s ability to deliver highly predictable and stable results. Revenues came in at $13.7 million, 2.5% higher year-over-year.

Revenue growth was largely driven by the utilization of the Distribution System Improvement Charge. DSIC is a Pennsylvania Public Utility Commission-allowed charge that water utilities collected from customers for the replacement of aging infrastructure. This, coupled with growth in the customer base boosted the metric.

Earnings per share (EPS) came in at $0.31, three cents higher compared to last year, due to moderately stable operating expenses and interest paid on debt. Consequently, EPS for the year landed at $1.30, compared to $1.27 in FY2020.

Management mentioned that they plan to invest $44 million this year and $50 million in 2023, excluding acquisitions. These funds will be allocated towards further main extensions, dam and pipe refinements, an elevated water tank, and water treatment plant construction.

Based on the company’s current rate agreements, population base, and CAPEX guidance, I estimate FY2022 EPS should come in close to $1.30 once again.

Dividend & Valuation

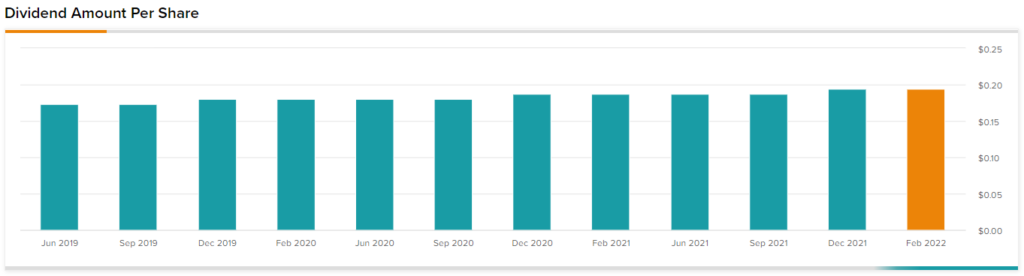

Due to operating such a predictable business model and enjoying resilient financials, York Water has not missed a dividend payment in over 200 years. Dividends have, nevertheless, grown annually for 25 consecutive years.

However, similar to the company’s EPS, the dividend has also been growing at a rather modest rate. York Water’s five-year dividend per share CAGR currently stands at just 3.85%.

The issue with the stock, however, is not that earnings and dividends are growing slowly, although that’s to be expected from the business. The issue is that investors have substantially overvalued YORW relative to the company’s growth potential. Based on an EPS of $1.30, the stock’s P/E currently stands at 33.6.

This is easily explained, as investors are willingly overpaying for the overall safe and predictable, quality cash flows associated with the stock. However, following the stock’s valuation expansion over the past few years, the dividend yield has now been compressed to just 1.77%. Hence, investors now face limited returns ahead and elevated valuation compression risks.

Investor Takeaway

York Water is a high-quality company that has demonstrated robust shareholder value creation for literally centuries. The stock would make for an optimal vehicle for conservative dividend growth investors looking for low-volatility returns.

However, at its current price levels, the stock’s yield is rather trivial considering the dividend’s growth prospects. Further, current investors face the risk of potential valuation compression, which could offset some, if not more, of York Water’s dividend returns.

Download the TipRanks mobile app now

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Read full Disclaimer & Disclosure