Tesla (TSLA), the leading EV maker in the United States, has a clean energy business that could become the company’s secret growth machine in the next decade. Under this business segment (known as Energy Generation and Storage), Tesla sells energy storage products and solar energy systems to customers, capitalizing on the growing demand for renewable energy products.

Since its founding in 2015, Tesla’s energy business has grown into a $3 billion business today, and the company is aggressively expanding it in key global markets such as China to gain long-term competitive advantages on a global scale. I am bullish on the outlook for Tesla as I believe the company is well-positioned to grow in the next decade.

The Booming Energy Business

In Q2, Tesla’s energy storage deployments reached an all-time high of 9.4 GWh, a year-over-year (YoY) increase of 158%. On the back of record deployments, Energy Generation and Storage revenue reached a new high of $3 billion compared to just $1.5 billion in Q2 2023. Meanwhile, the core EV business reported a revenue decline of 7% in Q2, which highlights the importance of the energy business at a time when macroeconomic pressures are limiting the growth of the EV segment.

The growing energy business is already helping Tesla’s bottom line. In the second quarter, the gross profit margin of the energy segment expanded by more than 600 basis points YoY to 24.6%, while Automotive gross margins declined by 70 basis points to 18.5%. Even on an absolute basis, energy gross margins are way ahead of Automotive margins, which suggests the energy business is fundamentally more profitable compared to Tesla’s core EV business. Q2 was the most profitable quarter for the energy business since its inception.

A year ago, the energy business only accounted for 6% of total gross profits, but in Q2, the contribution from this segment rose to 16.3%. This is an encouraging sign, given the high profitability of this business segment.

Tesla is aggressively investing in its energy business to capitalize on the opportunity in renewables. During the Q2 earnings call, CEO Elon Musk claimed that the company is planning to ramp up production in the U.S. In addition, Tesla is building a Megapack factory in China to cater to the growing demand for energy storage systems. According to company executives, Tesla is on pace to at least double the energy storage capacity in the foreseeable future.

The Big Picture Is Promising

According to BloombergNEF, the global energy storage market tripled in 2023, with record global additions of 97 GWh in storage capacity. This year, global energy storage additions are expected to hit 100 GWh, building on the positive momentum from last year. BloombergNEF projects the global energy storage market to grow at a CAGR of 21% to 442 GWh by 2030. Continued adoption of renewable energy is at the center of these expectations.

Energy storage systems play a crucial role in supporting the transition from fossil fuels to renewable energy. They help balance the intermittent nature of renewable energy sources by helping consumers and energy producers store excess energy to be utilized when production falls below demand.

Analysts Are Betting Big on the Energy Business

Wall Street remains concerned about Tesla’s growth prospects amid the slowdown in global EV sales, but some experts are banking on the energy segment to deliver outsized returns. For instance, Nancy Tengler, CEO and CIO of Laffer Tengler Investments, believes the energy segment will drive strong earnings growth for Tesla in the coming years. She even compared the energy segment to Amazon Web Services, which has been the key earnings driver for Amazon (AMZN) in recent years.

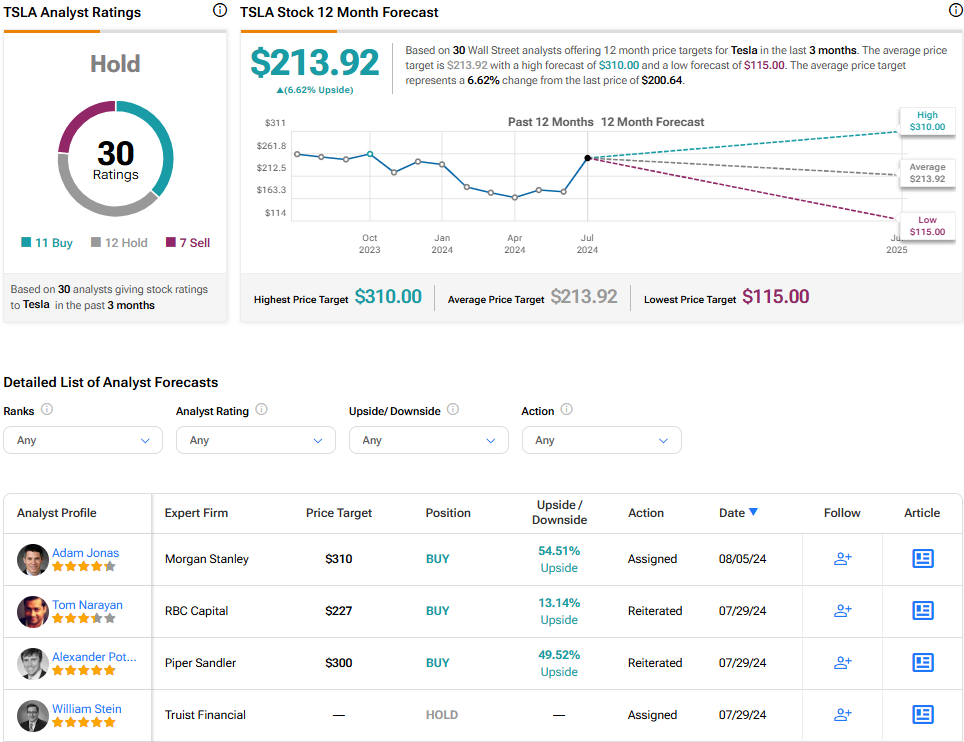

Additionally, Morgan Stanley (MS) analyst Adam Jonas, after digesting Q2 earnings, raised Tesla’s price target to $310, assigning the energy business a value of $50 per share, up from his earlier estimate of $36 per share. After boosting his estimates, the analyst commented that the energy business is a “show stealer.”

Cantor Fitzgerald analysts also raised their full-year revenue estimates for Tesla on the back of the improving outlook for the energy business. Cantor analysts now expect energy storage deployments of 29 GWh in 2024, up substantially from the previous estimates of 16.3 GWh. Energy segment revenue is expected to hit $9.6 billion this year against previous expectations of $6.6 billion. Stifel and Baird analysts also commented positively on the outlook for Tesla’s energy business following the strong second-quarter performance.

Is Tesla Stock a Buy, According to Analysts?

Tesla stock has declined more than 16% this year amid EV price cuts, intensifying competition, elevated interest rates, inflationary pressures, and regulatory challenges. This lackluster market performance has brought Tesla’s valuation to more reasonable grounds. Still, based on the ratings of 30 Wall Street analysts, Tesla stock earns a Hold consensus rating. The average Tesla stock price target is $213.92, which implies upside potential of 6.6% from the current market price.

Based on analyst projections, Tesla seems fairly valued today. Tesla has always enjoyed premium valuation multiples because of the company’s long runway for growth. Today, at a forward P/E of 83x, Tesla is trading well below its five-year average multiples of close to 300x. Although Tesla may not be as cheaply valued as traditional automakers, the growing energy business, Tesla’s dominance in the U.S. electric vehicle market, and the company’s expansion into robotaxis justify its valuation today.

The Takeaway: Tesla Still Has a Lot to Offer

Tesla’s energy business is proving to be a growth driver at a time when the company’s core EV business is facing challenges. In the long run, both these business segments will contribute positively to growth, which justifies the company’s premium valuation today. Analysts are also becoming bullish on the prospects for the energy business, which should lead to a meaningful hike in earnings estimates.

This is good news for Tesla, as positive earnings revisions often lead to stock market momentum. Despite short-term challenges, Tesla seems well-positioned to grow.