EV leader Tesla (NASDAQ:TSLA) reported its Q1 2023 production and delivery numbers on Sunday, and the news was both good and bad. It really depends on how you look at the data, and more importantly, on what you thought the data were going to look like before it was released.

According to the company, Tesla produced 440,808 electric cars in Q1, and delivered 422,875 EVs. Crunching the numbers, J.P. Morgan analyst Ryan Brinkman observed that Tesla delivered 36% more EVs in Q1 2023 than it had in Q1 2022, and that this was better than the 29% growth rate that J.P. Morgan had estimated — and even a bit better than what Tesla itself had predicted.

So good news? Yes… but.

The problem was that most investors weren’t focusing on J.P. Morgan’s estimate (or on Tesla’s, which was probably presumed to be a lowball hurdle designed to be easily jumped). Instead, investors focused on consensus Wall Street estimates that predicted Tesla would deliver something on the order of 432,000 electric cars in the quarter. And by that yardstick, Tesla missed estimates by more than 9,000 cars.

Merely “missing estimates” wasn’t the sum total of bad news for Tesla however, as Brinkman points out. You see, part of the reason Tesla supposed to perform so well on deliveries (i.e. sales) in Q1 is that the company cut prices on many of its cars earlier this year (in some cases, by as much as 20%). The goal was to spur sales, undercut competitors’ prices, and win market share. Factors “such as higher interest rates and tightening lending standards,” however, says Brinkman, as well as increasing competition from other automakers that are beginning to sell EVs, mean that Tesla is driving into the wind in these efforts.

The analyst notes that the net effect of macroeconomic factors, mitigated only in part by Tesla’s price cuts, is that most estimates now see Tesla delivering only 1.8 million cars through the end of 2023 — versus the 1.9 million deliveries Tesla was expected to make before announcing its price cuts in January.

And that’s not even the bad news.

Not only are price cuts apparently failing to goose sales numbers as much as expected. They’re also doing serious damage to Tesla’s profits. Brinkman estimates that for every 10% that Tesla cuts prices (and remember, for a lot of its cars, Tesla has cut prices 20%), it needs to sell 20% more cars to make up the difference and hold profits steady. Tesla’s failure to ramp sales as fast as it had hoped to, therefore, means that profits are almost certainly going to decline this year.

Mind you, Tesla’s still going to be profitable. Brinkman estimates $3.65 per share this year, $4.30 per share in 2024, and $4.65 in 2025. The question is really whether a Tesla stock growing at that expected rate — about 13% per year — is worth the 53 times earnings that Tesla stock currently costs.

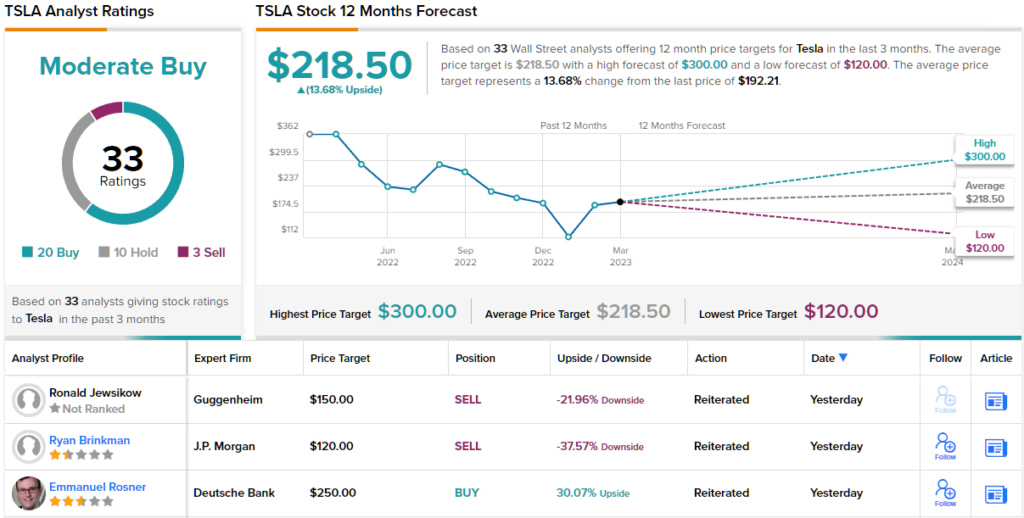

Brinkman doesn’t think it is. He rates Tesla shares an Underweight (i.e. Sell) with a $120 price target that implies ~38% downside from current levels. (To review Brinkman’s track record, click here)

Realizing all of this, investors sold off Tesla stock by 7.5% over the past two trading sessions.

Turning now to the rest of the Street, Tesla currently holds a Moderate Buy consensus rating among industry analysts. This rating is based on a breakdown of 20 Buy recommendations, 10 Holds, and 3 Sells. The stock has a $218.50 average price target, which suggests ~14% growth potential from the current price. (See TSLA stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.

Questions or Comments about the article? Write to editor@tipranks.com