Investors might have been slightly disappointed to hear Tesla (TSLA) will not be releasing any new models in 2022, but Wedbush’s Daniel Ives believes the growing EV demand coupled with announcements from the earnings call point to a good year ahead for the EV leader.

Maximize Your Portfolio with Data Driven Insights:

- Leverage the power of TipRanks' Smart Score, a data-driven tool to help you uncover top performing stocks and make informed investment decisions.

- Monitor your stock picks and compare them to top Wall Street Analysts' recommendations with Your Smart Portfolio

The company certainly saw out 2021 on a bright note, with each of the headline numbers in the 4Q21 report representing quarterly records.

On the top-line, revenue increased by 65% year-over-year to $17.72 billion, coming in ahead of the Street’s $17.1 billion estimate. And on the bottom-line, adj. EPS of $2.54 handsomely beat the Street’s $2.36 forecast.

Despite the chip/supply chain issues, and highlighting “more efficiency” at the Shanghai Gigafactory, the “all-important” Automotive GM (gross margins) hit 30.6%, also above the Street’s call for 29.2%.

The Street was anticipating $2.32 billion in cash from operations, but Tesla delivered $4.59 billion, which the 5-star analyst says speaks to a company “on a pace to generate significant cash flow over the coming years.” Amounting to new records too, operating profit hit $2.6 billion, and free cash flow came in at $2.8 billion.

Wall Street already knew what happened on the delivery front when earlier this month Tesla disclosed it had made 308,000 deliveries in the quarter vs. the Street’s expectation of 265,000. Ives thinks that were it not for the supply chain/logistics issues, the figure would have been 10% higher.

In any case, despite the lingering supply chain woes, deliveries should push higher in 2022 as churning out higher volume of the current models appears to be one of Musk and Co.’s top priorities. This should be possible with the added capacity from the soon-to-be opened Austin facility – where Musk confirmed on the earnings call that the production ramp has started and said Texas built-Model Ys will include 4680 battery cells, both “key” announcements – and Berlin factory. Ives thinks the new facilities will help Tesla reach a capacity of ~2 million units annually – doubling on the ability to produce approximately 1 million a year at present. In fact, against a supply constrained backdrop, the analyst believes the Austin production news and 4680 update are “potential ‘game changers’” to the Tesla story.

Given all of the above, Ives has high hopes. Along with an Outperform (i.e. Buy) rating, he keeps a $1,400 price target on the stock. This target puts the upside potential at 69%. (To watch Ives’ track record, click here)

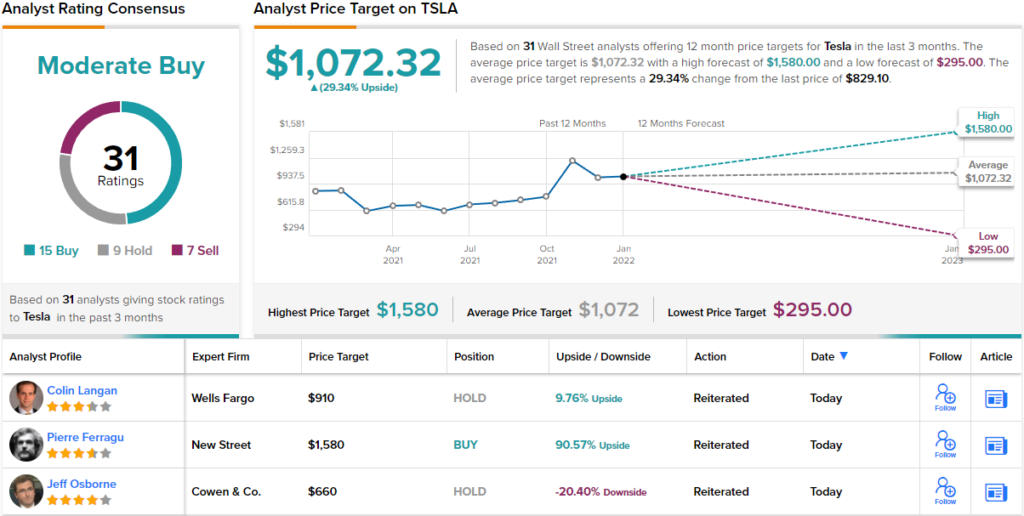

Ives’ objective is on the bullish end of the spectrum; the Street’s average target is a more modest $1,072 and change, which is set to yield returns of ~29% over the coming months. All in, the stock’s Moderate Buy consensus rating is based on 15 Buys, 9 Holds and 7 sells. (See Tesla stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.