Tencent (OTC:TCEHY) just posted its Q4 report, highlighting management’s commitment to rising capital returns. Shares of China’s social media and tech behemoth have struggled to find their footing despite its U.S.-based counterparts recording significant share price gains in recent months. Thus, I believe Tencent’s choice to meaningfully boost both buybacks and dividends is a suitable strategy for pulling the bulls back to the stock. In the meantime, its overall financials came in robust, further supporting the bullish narrative.

Don't Miss our Black Friday Offers:

- Unlock your investing potential with TipRanks Premium - Now At 40% OFF!

- Make smarter investments with weekly expert stock picks from the Smart Investor Newsletter

Q4: Strong Results Contrast Lagging Share Price

Tencent’s share price has lagged behind in recent quarters, significantly underperforming its American counterparts. This is not a recent trend. Chinese stocks, including Tencent, have underperformed for years, with 2023 marking Hong Kong’s Hang Seng Index’s fourth consecutive year of losses. Despite investors remaining skeptical of Chinese stocks, Tencent’s results have consistently defied concerns. Its most recent Q4 report was no different, with numbers contrasting the stock’s underlying performance.

In particular, total revenues rose by 7% to $21.9 billion, with revenue growth in Online Advertising and Fintech Services more than offsetting the softer performance in Value-Added Services (VAS). Let’s take a close look.

Value-Added Services

Tencent’s Value-Added Services division underperformed in Q4, with its revenues declining by about 2% to $9.6 billion. The division’s International Games revenues rose by 1% year-over-year, but that was due to a currency tailwind, as revenues actually declined by 1% in constant currency. Tencent noted that PUBG Mobile saw a strong revenue upturn while VALORANT sustained strong growth. However, most of the other titles appear to have matured in a very competitive video game market.

Domestic Games revenues also came in soft, down 2% year-over-year, while Social Networks revenues, which include Tencent’s WeChat, decreased by 2% year-over-year. This was due to a decline in revenues from music-related and games-related live streaming services, partially offset by revenue growth from music subscriptions and Mini Games platform service fees.

Online Advertising

Unlike the rather underwhelming numbers in Value-Added Services, Tencent’s Online Advertising division posted robust revenue growth of 23% in Q4 to $4.1 billion. The increase in revenues was driven by strong advertising demand for Video Accounts and advancements in the company’s advertising platform. In fact, management noted that all customer categories except automotive recorded year-over-year growth in ad spending.

FinTech and Business Services

Tencent’s FinTech and Business Services division also contributed positively to Tencent’s top-line growth, with its quarterly revenues rising 15% year-over-year to $7.56 billion.

Regarding FinTech Services, this branch enjoyed double-digit year-over-year growth, which was driven by growth in commercial payment activities and advancements in wealth management and consumer loan services. Looking at Business Services, this branch achieved year-over-year growth of around 20%, primarily powered by growth in e-commerce technology service fees within Video Accounts and higher revenues from cloud services.

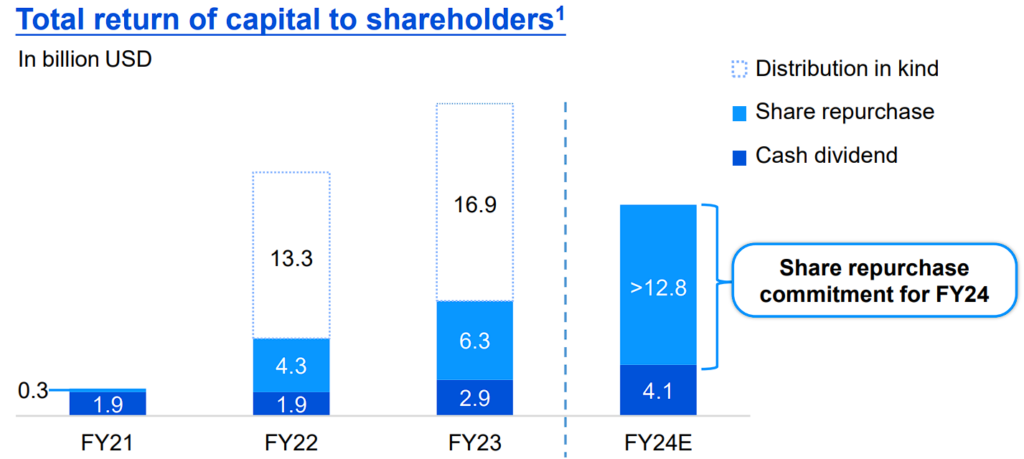

Record Free Cash Flow Prompts Big Buyback, Dividend Boost

Tencent’s strong Q4 report led to full-year revenue growth of 10% to $86 billion. Simultaneously, Tencent managed to keep expenses stable year-over-year, helping revenue growth expand the company’s operating margin from 20% last year to 26% in FY2023. This, in turn, led to Tencent seeing a free cash flow surge of 56% to a record $27.91 billion.

Again, you can see the contrast between Tencent’s financials and its stock price performance. It’s no wonder, thus, that management is now taking the opportunity to utilize its surging free cash flow into buybacks in an attempt to create shareholder value off of the rather muted stock price.

Specifically, management stated that it intends to at least double the amount spent on buybacks this year, from HKD49 billion ($6.3 billion) last year to over HKD100 billion (>$12.8 billion). Furthermore, management proposed increasing the annual dividend for FY2023 by 42% to HKD3.40 per share ($0.43).

The combination of the minimum share repurchase commitment and the dividend payment amounts to $16.9 billion in capital returns, which translates to a blended shareholder yield of about 4.8%. That is not a bad capital return rate, given that this is a growing tech company, especially since buybacks will likely end up being somewhat more than the $12.8 billion minimum commitment.

In my view, Tencent’s sustained, double-digit growth coupled with its robust blended yield make for an enticing blend that could pull bulls back and steer the stock away from its sideways trajectory.

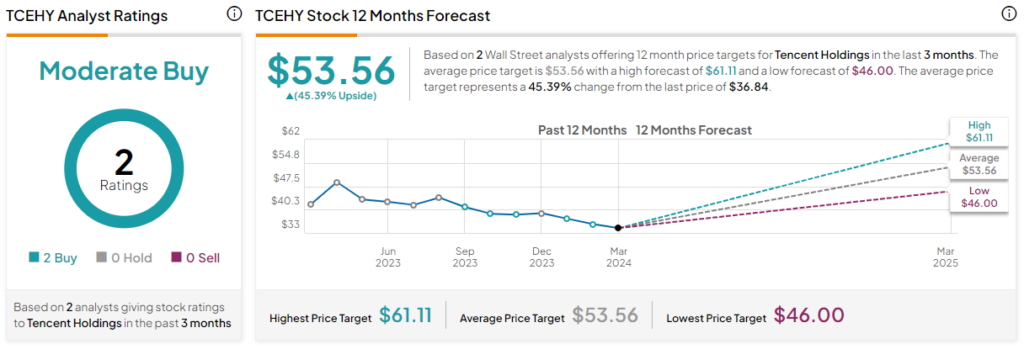

Is TCEHY Stock a Buy, According to Analysts?

Looking at Wall Street estimates on the stock, Tencent Holdings features two unanimous Buy ratings in the past three months. At $53.56, the average Tencent Holdings stock price target implies 45.4% upside potential.

The Takeaway

To sum up, I believe that Tencent’s Q4 report underscores the contrast between the company’s flourishing financials and the stock’s lagging share price. While the VAS division didn’t perform well, the growth in online advertising and fintech services remains vigorous.

Moreover, Tencent’s expanding margins and record-high free cash flow have driven a substantial jump in buybacks and dividends, signaling management’s commitment to creating shareholder value. I believe these developments are likely to attract the bulls back, diverting the stock from its sluggish trajectory.