“Ball of confusion, that’s what the world is today,” sang the Temptations on their 1970 classic, a sentiment which can readily apply to the stock market’s present state.

It’s hard to get a grip on the market’s choppy action in 2022 and investors could use a clear signal to follow when considering a new investment.

One way to get a head start is by tracking the moves of the insiders. These are the corporate officers with in-depth knowledge of the companies they helm. To keep the playing field level, they are required to make their trades public, and when they start scooping up their own company’s stock, it sends a clear signal to investors they believe the shares are ripe for the picking.

Using the TipRanks’ Insiders Hot Stocks tool, we’ve homed in on 2 names which those in the know have been backing up the truck for. In addition to the insiders, Wall Street has a favorable take on these stocks too; both are rated as Strong Buys by the analyst consensus and offer plenty of upside. Here’s the scoop.

PacWest Bancorp (PACW)

We’ll start in the finance sector with bank holding company PacWest Bancorp. The Los Angeles, California-based mid-cap holds assets worth more than $39 billion and favors a relationship-based approach to its business, catering to small, mid-market, and venture-backed businesses across the nation. While its branch footprint is mostly in California, the company is also a nationwide lender.

Capital market volatility has put significant strain on PacWest’s fee income in the latest quarterly statement – for 1Q22. Revenue not only declined by 47% from the same period last year to $162.12 million but also fell way short of the $342.21 million consensus estimate. The bottom-line performance disappointed too, as EPS of $1.01 missed the $1.04 analysts expected.

There were positives to note, though, with strong loan growth – loans increased to $1.4 billion, amounting to a 6.1% sequential uptick, while management also plans on hiring more stuff and intends to invest in PacWest’s digital platforms – actions which could deliver loan growth over the coming months.

Overall, the earnings display did not help the stock; PACW shares have trended south this year and sit 35% into the red. But now the insiders evidently feel the time is right to pounce.

The past few days have seen some big transactions by several corporate members. William Black , EVP, Strategy & Corporate Development, has loaded up on 20,000 shares for a total of $400,000, Rebecca Cordes, EVP, HR, paid 250,000 for 10,000 shares while Christopher Blake, Pres. & CEO, Community Banking, bought 8,000 shares for the total sum of $200,000.

Reflecting the insiders’ confidence, despite the issues, RBC analyst Jon Arfstrom takes an upbeat approach to the latest earnings release.

“Results this quarter were generally strong at the core, with solid loan growth and margin expansion, as well as very stable credit metrics and well-controlled expenses,” the 5-star analyst wrote. “While the volatility in the capital markets did pressure fee revenues meaningfully, we believe the sustained strength in the core banking business and a continued favorable outlook here should be the key takeaway from this quarter. Our expectation is that the fee pressures will abate over time, and ultimately revenues trend higher from here.”

Accordingly, Arfstrom rates PACW stock an Outperform (i.e. Buy) while his $56 price target makes room for 12-month growth of ~93%. (To watch Arfstrom’s track record, click here)

The RBC analyst is certainly no lone PACW bull. Barring one Hold, all 6 other recent analyst reviews are positive, making the consensus view here a Strong Buy. The forecast calls for one-year gains of 69%, considering the average price target stands at $49.14. (See PACW stock forecast on TipRanks)

Concert Pharma (CNCE)

Let’s take a sharp turn away from the banking sector for our next stock. Concert Pharma is a clinical-stage biopharma company and a pioneer in the use of deuterium chemistry – a chemical reaction in which a covalently linked hydrogen atom is replaced by a deuterium atom, or vice versa, in what is known as hydrogen–deuterium exchange. Via deuterium substitution, the company hopes to find and develop novel drugs that have a beneficial impact for patients and solve serious medical needs.

Concert’s pipeline includes several collaborations with other pharma companies, one of which is with Avanir Pharmaceuticals; Avanir is undertaking several Phase 2 and Phase 3 clinical trials to evaluate AVP-786, indicated to treat neurologic and psychiatric disorders.

As for Concert’s own drug development, it is working on CTP-543, an oral inhibitor of Janus kinases JAK1 and JAK2, intended as a therapy for alopecia areata – an autoimmune condition that usually leads to patchy hair loss; the disorder currently has no approved treatment.

Last month, the company released positive results from the Phase 3 THRIVE-AA1 study in which CTP-543 met its primary endpoint; following 24 weeks of treatment, the drug showed a dose-dependent improvement in the percentage of patients attaining an absolute Severity of Alopecia Tool score of 20 or under (SALT ≤20).

The results have helped Concert buck the trend in 2022 and the shares are up by an impressive 51% year-to-date. However, some insiders obviously think the stock still has more room to go up.

This week has seen 3 directors making Informative Buys; Thomas Auchincloss spent $28,500 on $6,000 shares, Christi Van-Heek splashed out $49,999 on 10,526 shares, although both outlays were dwarfed by the $999,999 Richard Aldrich paid for 210,526 shares.

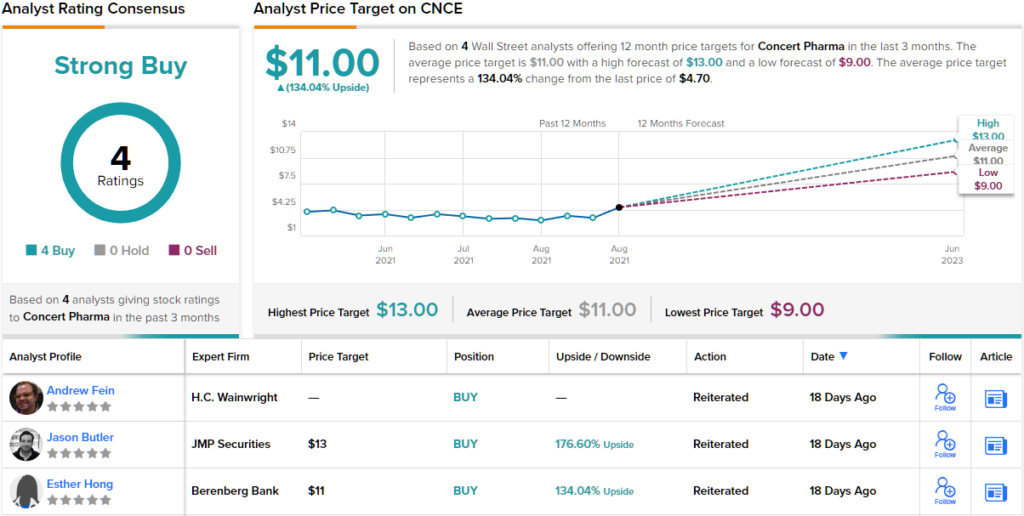

They are not alone in feeling confident regarding Concert’s prospects; H.C. Wainwright analyst Andrew Fein laid out the bull-case, writing: “With a robust efficacy from the first pivotal trial, the Phase 2 and OLE efficacy data, and safety data consistent with the Phase 2 trial, we believe CTP-543 might also meet the primary endpoint in the second pivotal trial, THRIVE-AA2 (readout expected 3Q22).”

“Despite competition, based on the robust risk-benefit profile, we believe CTP-543 has the potential to be a blockbuster drug with the possibility of capturing nearly 35% by 2028 reaching around $1B by 2030,” the analyst added.

These comments underpin Fein’s Buy rating and are backed by a $17 price target. The implication for investors? Upside of a hefty 262%. (To watch Fein’s track record, click here)

Joining the bull parade, all 3 other recent Wall Street reviews are positive, providing this stock with a Strong Buy consensus rating. The average price target stands at $11, suggesting the share price will more than double in the year ahead. (See CNCE stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.