The stock markets are all about timing. Whether your investment strategy is bullish or bearish, what matters is making the right moves at the right time. This is the truth at the heart of the old Wall Street cliché that bulls and bears make money, while pigs get slaughtered. If you get greedy, and start chasing money, you’ll overlook the signs that tell you when to buy or sell.

Don't Miss Our Christmas Offers:

- Discover the latest stocks recommended by top Wall Street analysts, all in one place with Analyst Top Stocks

- Make smarter investments with weekly expert stock picks from the Smart Investor Newsletter

Smart investors will be looking for reliable signs that will indicate a stock’s likely movement. In volatile times like these, those signs are more necessary than ever. One signal that has been correlated with a stock’s future performance is insider activity. This makes sense. Insiders, the corporate officers charged with running a company and producing profitable results for shareholders, are privy to far more information than the average stock investor – and they will use it to trade. Following an insider’s trading activity – buy or sell – is a viable strategy for investors.

How can you find the hottest insider trading stocks right now? There is a simple answer: TipRanks’ Insider Hot Stocks tool. This collates all the recent insider transactions to reveal stocks with the most bullish insider sentiment. Plus all the insiders are ranked so you can make sure you follow only the insiders that are actually making money.

With this in mind, here is the scoop on three beaten-down stocks that have seen recent multi-million purchase activity.

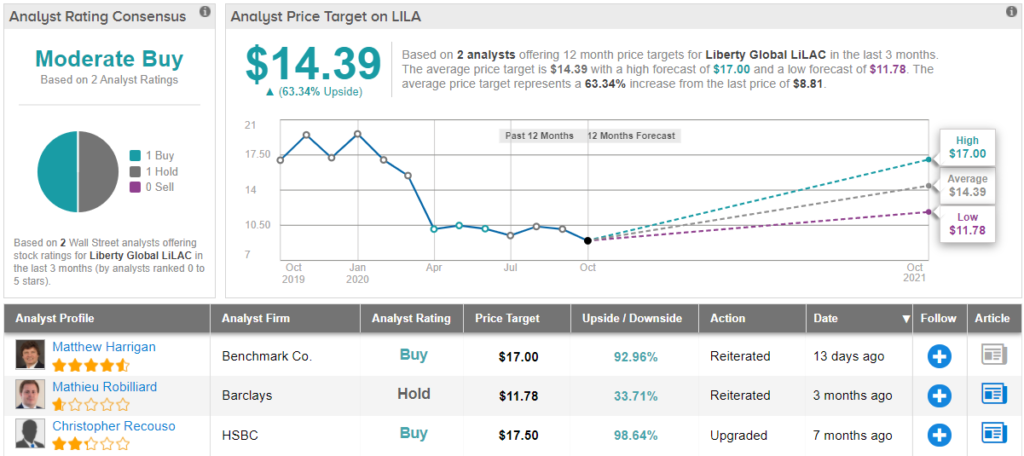

Liberty Global PLC (LILA)

First on our list is a major telecom company in the Western Hemisphere, Liberty Latin America. The company has its hands in broadband internet, mobile services, telephone services, and broadcast video, along with other entertainment services, and its main presence reflects its name: it is most active in Chile, Colombia, Central America, Puerto Rico, and the Caribbean. Liberty Latin America is also active in Florida, where there is a large minority population drawn from these regions.

The COVID crisis has had a heavy impact on LILA’s performance. The company’s financials hit bottom in April, at the beginning of Q2, when positive first quarter performance turned south. Q2 ended with a sequential revenue loss of 8.9%, and deep net loss in EPS. Share prices started falling at the end of February and beginning of March, and have failed to regain traction since. The stock is down 52% year-to-date.

But management is confident that business is returning to normal. And that confidence attracted some strong insider buys during the Latin American recent stock sale. Three of those informative transactions were for million-dollar-plus buys.

The largest came from Eric Zinterhofer, of the Board of Directors, who bought up over 2.96 million shares for a $21,149,572. Fellow Board member John Malone made the second largest purchase, of 2.74 million shares for $19,559,030. And finally, President and CEO Michael Fries, of the original parent company Liberty Global, bought 172,196 shares for $1.229,479. These purchases, along with several smaller, pushed the insider sentiment on LILA shares strongly positive.

This was noted by Benchmark’s 5-star analyst Matthew Harrigan, who wrote, “…we believe LILA executed well against its business plan despite operating performance that has been hampered by COVID-19 dislocations, especially in Chile. LILA also focuses on a Latin Emerging Markets region that is now decidedly out of favor with investors. This is as [the CEO and CFO] have made recent open market share purchases even beyond the rights offering.”

Harrigan’s $17 price target suggests an impressive 93% upside for the stock, and supports his Buy rating. (To watch Harrigan’s track record, click here)

Overall, Liberty Global has a Moderate Buy rating from the analyst consensus, based on a 1:1 split between Buy and Hold reviews. The stock is selling for $8.81, and the average price target of $14.39 suggests a 63% upside in the coming year. (See LILA stock analysis on TipRanks)

Continental Resources (CLR)

Next on our list is a player in the North American oil and gas industry. Continental produced 340K barrel of oil equivalent per day last year, producing over $4.63 billion in total revenue. The company operates in Oklahoma, but its major presence is in the Bakken formation of North Dakota and Montana.

Falling prices and falling demand during 1H20 hurt the company, as the COVID pandemic put massive downward pressure on the economy. Revenues slipped to just $175 million in Q2, generating a net EPS loss of 71 cents.

But there is a rebound as the economy restarts, and the outlook for Q3 is better – a projected EPS loss of 27 cents. The company is in the midst of streamlining operations, shutting down unproductive wells to cut costs and focus efforts on the most profitable activities.

Sliding 63% year-to-date, one board member sees better days ahead. Harold Hamm spent over $9.74 million buying up 769,235 shares in the company. His move made the net insider sentiment positive on CLR stock.

MKM analysts John Gerdes believes the stock is undervalued at current levels, noting, “CLR has depreciated over 30% (vs. XOP -~25%) since early June and reflects over 40% intrinsic value upside… Our 3Q20 production expectation is ~295 Mboepd is in the upper half of guidance, and our YE20 production outlook of ~323 Mmboepd is 1% above the midpoint of guidance…”

Gerdes sets his price target at $20, implying a 58% upside for the coming year, which fully backs his Buy recommendation. (To watch Gerdes’ track record, click here)

The overall view on CLR stock is cautious; Wall Street’s analyst consensus rating is a Hold, based on 12 reviews breaking down to 3 Buy, 7 Holds, and 2 Sells. However, the average price target is $16.54, suggesting a 30% one-year upside from the current share price of $12.69. (See CLR stock analysis on TipRanks)

Net 1 UEPS Technologies (UEPS)

South Africa-based Net 1 is a is tech company, with a non-exclusive worldwide license for the Universal Electronic Payment System. The company is a leader in providing financial tech, payment solutions, and transaction processing in multiple emerging economies and across multiple industries. The company offers services through an alliance network with banks, card issuers, and retailers.

Like the other companies on this list, Net 1 saw revenues and earnings fall when corona shut down the economy. The general slowdown in economic activity, especially in retail, was a hard blow. Q2 number reflected that, with the top line at just $25 million and EPS deep in negative territory with a 69-cent net loss. Share price has been volatile, and has not yet recovered from losses sustained early in the crisis. UEPS is down 20% from its peak in early February.

There are some bright spots. The outlook for Q3 is better, with the EPS loss projected at just 9 cents. And the company ended the second quarter with no debt and unrestricted cash on hand of $218 million. This puts UEPS in a strong position to rebound as the economy starts revving again.

Turning to the insider trades, Anthony Ball of the Board of Directors has the most recent informative buy. Last week, he purchased over 350,024 shares, laying out $1.2 million for the stock.

Rajiv Sharma, of B. Riley FBR, has written the only recent review of UEPS on file, and he is upbeat on the stock.

“We believe UEPS’ long-term investment portfolio holds solid promise, especially its MobiKwik investment in India and despite their illiquid status. Despite ST COVIDrelated setbacks to UEPS’ operating business in South Africa, we believe it holds promise as a valuable business given its hold on micro lending and a sizable potential subscriber market in South Africa. There is a good chance that UEPS could grow its customer base substantially from here and continue to add ancillary services to their core businesses.”

Sharma rates UEPS share a Buy, and his $5 price target suggests room for 45% growth from the current share price of $3.44. (To watch Sharma’s track record, click here)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.