Advanced Micro Devices (AMD) could not deliver the by now almost customary beat-and-raise in its latest quarterly statement, even as the company delivered record revenues driven by a big growth for its server sales.

Discover the Best Stocks and Maximize Your Portfolio:

- See what stocks are receiving strong buy ratings from top-rated analysts.

- Filter, analyze, and streamline your search for investment opportunities with TipRanks’ Stock Screener.

The chip giant generated sales of $6.55 billion, amounting to a 70.1% year-over-year increase and just edging ahead of the $6.53 billion consensus estimate. For the bottom-line, adj. EPS hit $1.05, 2 cents above the $1.03 predicted by Wall Street. Data center was the star of the show, as revenue surged by 83% from the same period last year.

AMD stock recently overtook its once far bigger rival Intel’s market cap, and as an indication of how AMD is trouncing it in the data-center market, Intel recently reported a 16% year-over-year sales decline for its data-center server segment.

However, marring the occasion, the top-line outlook just missed Street expectations. Due to the ongoing weakness in PCs, although AMD managed to meet its target for Q3 sales between $6.5 billion to $6.9 billion, the figure came in shy of the analysts’ call for $6.84 billion. Nevertheless, AMD stuck to its revenue outlook of $26 billion to $26.6 billion for the full year.

Scanning the print, Susquehanna analyst Christopher Rolland notes the company remains on track to meet its targets, even in the face of a “challenging PC environment.”

“Despite the slowing PC backdrop, AMD reiterated their full-year outlook, underpinned by strength in server,” the 5-star analyst said. “While we had previewed a 3Q miss and cut estimates, guidance was only a tad below and certainly ‘better than feared’. More importantly, management reiterated their full year guidance of $26.3 billion. That said, it creates a lofty goal for 4Q (even with the 14th week), particularly considering uncertainty around the PC market and traditional decline in consoles.”

All told, there’s no change to Rolland’s Positive (i.e., Buy) rating or $115 price target. The implication for investors? Upside of 12% from the current trading price. (To watch Rolland’s track record, click here)

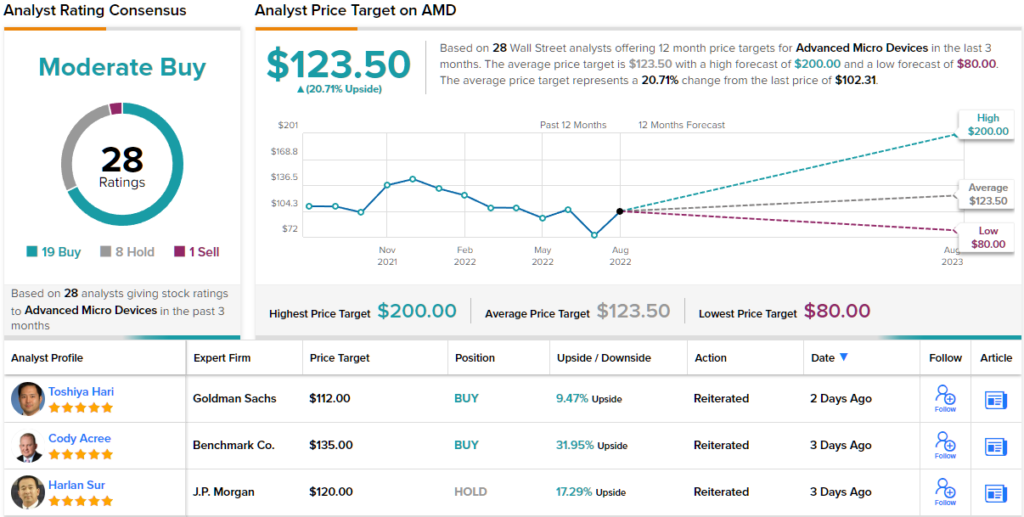

Most analysts are backing AMD’s continued success, although not all are believers. The stock claims a Moderate Buy consensus rating, based on 19 Buys, 8 Holds and 1 Sell. Given the average price target stands at $123.50, there’s room for ~21% share appreciation in the year ahead. (See AMD stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.