For most of this year, investor sentiment was high, and the markets were on an upward tear. But that sputtered to a halt at the end of the summer, and this fall has seen a pullback in the main indexes. We’re still up for the year-to-date, but not by as much as we were in July. At this writing, the S&P 500’s year-to-date gain is 9%, and the NASDAQ’s is 22%.

Discover the Best Stocks and Maximize Your Portfolio:

- See what stocks are receiving strong buy ratings from top-rated analysts.

- Filter, analyze, and streamline your search for investment opportunities with TipRanks’ Stock Screener.

It is most accurate to say that current conditions are volatile and unsettled. Both the bulls and bears can find plenty of evidence and precedent to back up their claims. The result: confusion among investors, who just aren’t sure where to go from here.

Leon Cooperman, the billionaire investor and hedge manager who got his start at Goldman Sachs and now runs Omega Advisors, takes a more moderate stance. Urging caution for investors, Cooperman has stated his belief that the S&P 500 is overvalued now, and will likely face a downturn in the near future.

“I don’t think we’re in a bubble; I think we’re in a rolling correction,” Cooperman has said, and he’s added that it will “take a long time for us to work out the problems.” The S&P hit its last peak, near 4,800, in January of last year, and Cooperman thinks it will take a long while before it can climb back to that level.

So, a cautious mind set is required and that will lead us to dividend stocks. These are the stocks that will ensure a steady income no matter the day-to-day market swings and protect the portfolio against any incoming volatility.

Turning to Cooperman for more inspiration, we took a closer look at two high-yield dividend stocks in which the billionaire investor has placed his trust. Here are the details.

Don’t miss

- Wall Street’s Best Analyst Bets on These 3 Energy Stocks — Here’s Why You Might Want to Follow His Lead

- Billionaire Leon Cooperman About the Stock Market — Here Are 2 High-Yield Dividend Stocks He’s Using for Protection

- Piper Sandler Says the S&P 500 Could Still Surge 14% in 2023 — Here Are 2 Stocks to Keep an Eye On

Energy Transfer

First up, Energy Transfer is a major player in the North American midstream sector, the vital segment of the energy industry that connects oil and natural gas producers with their end customers. Midstream companies operate networks of pipelines, transport assets, storage facilities, and terminal facilities, moving hydrocarbons and refined products to where they are needed. Energy Transfer has operations in 41 states, plus international offices in Panama City, Panama, and Beijing, China.

The company’s core operations include the transport, storage, and terminalling of crude oil, natural gas, natural gas liquids, and refined hydrocarbon products. Energy Transfer’s two largest areas of operation are centered in Texas, Oklahoma, and Louisiana, and in the Great Lakes-Mid Atlantic regions. ET’s network includes gathering facilities, fractionation facilities, pipelines, processing plants, and import/export terminals.

Energy Transfer is a dominant player in the midstream sector, boasting a market cap of $43 billion, and this past summer, the company completed a move that will expand its market share and footprint. In August, Energy Transfer and Crestwood announced an acquisition agreement; ET will fully acquire Crestwood and its assets. The transaction, which will be conducted wholly in stock, is valued at nearly $7.1 billion and is expected to close in early November.

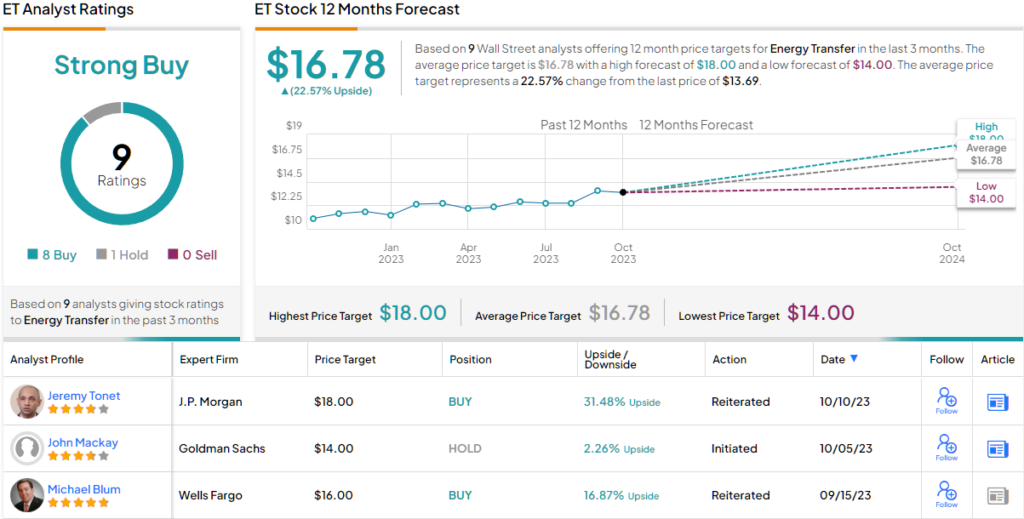

Also in early November, Energy Transfer will release its 3Q23 financial results. Looking back at the Q2 results, we find that the company had a top line of $18.3 billion, a result that was down 29% year-over-year and missed the forecast by over $2 billion. The midstream company’s bottom-line EPS, at 25 cents per diluted share, missed the estimates by 7 cents. For Q3, the Street is expecting ET to show $20.4 billion in revenue and 25 cents per share in earnings.

One recent metric that bodes well for return-minded investors comes from the company’s dividend. ET, on October 20, announced a modest increase in the common share dividend payment, from 31 cents to 31.25 cents. The new payment will go out on November 20; at the new rate, the dividend annualizes to $1.25 per common share and yields 9%.

As for Leon Cooperman, he remains long and strong here. The billionaire investor holds an impressive 11,912,500 shares in ET, which are worth $163 million at current prices.

For Stifel analyst Selman Akyol, Energy Transfer is a company with high return potential going forward in a favorable commodity market environment. He writes of the stock, “Over the last several years ET has focused on reducing debt while finishing a campaign of large capital investments. With the upturn in the commodity environment and production on the rise across the US, Energy Transfer is poised to generate significant free cash flow. We believe investors will be well served by owning ET as demand for US energy increases around the globe… The set up for 2024 looks great for ET.”

The 5-star analyst goes on to give ET stock a Buy rating, with an $18 price target that suggests it will gain 30% in the year ahead. Add in the dividend yield, and the total return potential hits 31%. (To watch Akyol’s track record, click here)

Overall, ET shares maintain a Strong Buy consensus rating from the Street, based on 9 recent reviews that include 8 Buys and 1 Hold. The stock is selling for $13.69 and its $16.78 average price target implies an upside of ~23% on the one-year horizon. (See ET stock forecast)

Arbor Realty Trust

From energy, we’ll switch to another segment that is well known for perennial dividend champs: real estate investment trusts. The REITs are companies that acquire, own, lease out, and manage real properties – residential, commercial, industrial, and more – as well as invest in mortgages and mortgage-backed securities. They attract shareholders with strong profit-sharing policies, including high dividend yields.

Arbor Realty works in the commercial REIT segment, focusing on funding the development and building of multifamily residential projects. That is, the company provides commercial mortgages for developers and builders working on apartment complexes. Arbor is involved in multiple commercial property funding operations, and in addition to private loan funding also works with both Fannie Mae and Freddie Mac.

As of June 30 this year, the end of 2Q23, Arbor’s fee-based loan servicing portfolio totaled $29.45 billion, with the bulk of that – slightly more than $20 billion – serviced through Fannie Mae. Arbor’s loan and investment portfolio had an unpaid principal balance of $13.49 billion and had an average current interest pay rate of 8.76%.

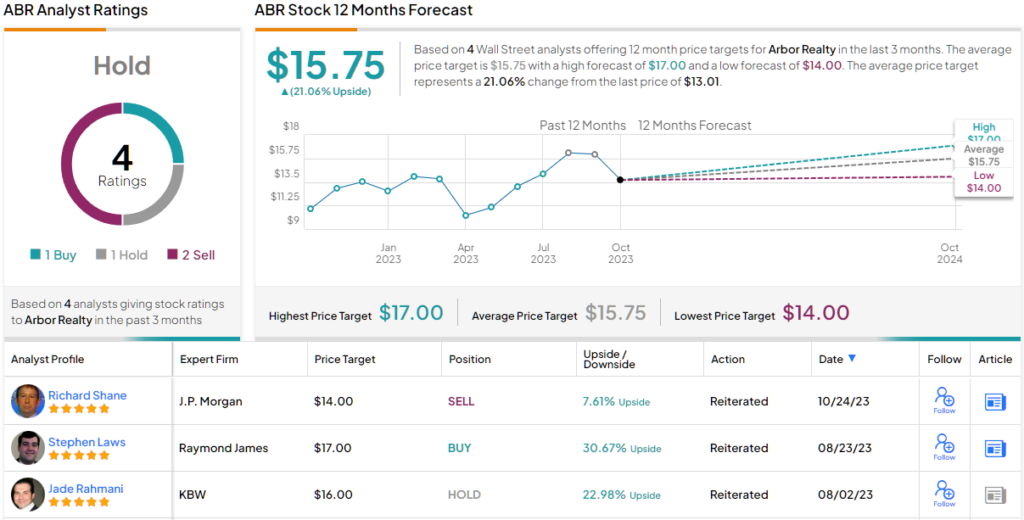

This portfolio activity generated a net interest income for Arbor of $108.5 million in Q2, up 15% year-over-year and $9.7 million better than had been expected. The company’s bottom line, a non-GAAP distributable earnings per diluted share, came to 57 cents, beating the forecast by 12 cents. Arbor will report its Q3 results on October 27, and the Street is looking for 47 cents per share in distributable earnings and $98.35 million in revenues.

The company last paid its common share dividend on August 31 at 43 cents per common share. This was up a penny from the previous quarter and was fully covered by the distributable earnings. The dividend’s annualized rate of $1.72 gives a forward yield of 12.5%.

Cooperman also has a big position here. He currently owns 3,454,694 shares of ABR, which command a market value of ~$45 million.

ABR also gets the support of Raymond James’ 5-star analyst, Stephen Laws, who likes Arbor for both its dividend and its clear ability to cover that dividend.

“Our distributable earnings estimates are increasing, as the benefits of wider portfolio spreads and lower expenses more than offset the impact of more conservative portfolio growth assumptions. Our Outperform rating reflects the attractive portfolio characteristics (floating rate, primarily multifamily), business diversification, high earnings visibility provided by the agency segment, and strong dividend coverage,” Laws opined.

Laws uses this stance to support his Outperform (i.e. Buy) rating on the shares, and his $17 price target implies that ABR will gain ~31% in the coming year. Combined with the dividend yield, that return can reach ~43%. (To watch Laws’ track record, click here)

The rest of the Street is less confident, however; based on 1 Buy and Hold, each, plus 2 additional Sells, the stock has a Hold consensus rating. Yet, the $15.75 average target price suggests an upside of ~21% in the next 12 months. (See ABR stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.