Shares of Starbucks (SBUX) have trended lower over the past month despite the multinational coffee chain operator delivering a solid Q3 performance, and raising its full-year global comparable-store sales (comps) growth and EPS outlook.

What didn’t excite investors was the cut in the international comps growth outlook, primarily in China. (See Starbucks stock charts on TipRanks)

Notably, Starbucks lowered its full-year international comps growth outlook to 15-17% (previously 25-30%). Meanwhile, it expects comps to increase by 18-20% in China, down from earlier growth guidance of 27-32%.

The cut in international growth guidance comes on the back of the resurgent COVID-19 virus that limits traffic, and hurts the overall recovery process. I’m neutral on Starbucks stock.

Moreover, investors’ fears were exacerbated further when its peer, Yum China Holdings (YUMC), a licensee of Yum! Brands (YUM) in mainland China, reported that its comps declined by a mid-teens rate in August, due to the rapidly spreading Delta variant of COVID-19.

Yum China warned that its adjusted operating profit would be reduced by 50-60% in Q3.

While the coronavirus poses challenges, Starbucks’ solid margin outlook is encouraging. The company raised its adjusted operating margin outlook to 18% from the previous forecast of 16.5% to 17.5%. Highlighting the strength in Starbucks’ average ticket (a key driver of margins) in the U.S., Sharon Zackfia of William Blair reiterated her Buy rating on the stock.

Notably, Starbucks’ adjusted operating margin in the Americas remains strong, benefitting from favorable sales mix and SKU rationalization.

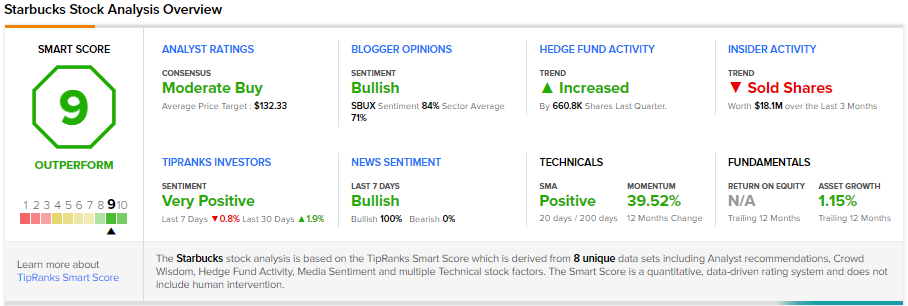

On TipRanks, SBUX stock has a Moderate Buy consensus rating, based on 13 Buys and five Holds. The average Starbucks price target of $132.33 implies 15.4% upside potential from current levels.

Further, SBUX scores 9 out of 10 on TipRanks’ Smart Score rating system, indicating that it has strong potential to outperform market expectations.

Disclosure: On the date of publication, Amit Singh had no position in any of the companies discussed in this article.

Disclaimer: The information contained in this article represents the views and opinion of the writer only, and not the views or opinion of TipRanks or its affiliates, and should be considered for informational purposes only. TipRanks makes no warranties about the completeness, accuracy or reliability of such information. Nothing in this article should be taken as a recommendation or solicitation to purchase or sell securities. Nothing in the article constitutes legal, professional, investment and/or financial advice and/or takes into account the specific needs and/or requirements of an individual, nor does any information in the article constitute a comprehensive or complete statement of the matters or subject discussed therein. TipRanks and its affiliates disclaim all liability or responsibility with respect to the content of the article, and any action taken upon the information in the article is at your own and sole risk. The link to this article does not constitute an endorsement or recommendation by TipRanks or its affiliates. Past performance is not indicative of future results, prices or performance.