Starbucks (NASDAQ:SBUX), the world’s largest coffee shop chain, has struggled recently amid woes in China and weak same-store sales in the U.S. This prompted former CEO Howard Shultz to call for a “maniacal focus on the customer experience” and to say he doesn’t like the Starbucks app. I’ll explain why I think Howard Schultz’s approach is likely wrong and why I remain bullish on Starbucks despite its negative shareholders’ equity.

Confident Investing Starts Here:

- Easily unpack a company's performance with TipRanks' new KPI Data for smart investment decisions

- Receive undervalued, market resilient stocks straight to you inbox with TipRanks' Smart Value Newsletter

Why Howard Schultz Is Likely Wrong

Former CEO Howard Schultz recently did an interview with Acquired. In the interview, he said that he wasn’t a big technology guy and that he built the company on humanity, the customer experience, free advertising, great coffee, a unique cup, and brand power. I think Howard did everything right, and the company’s low employee turnover and friendly staff show that the culture he built is still intact.

Nonetheless, Howard then spoke out against the Starbucks app, saying he doesn’t like how it has ruined the connection between the customer and the Barista. He said that Starbucks needs to bring back the human connection that it was built on. This was met by resistance from the show’s hosts, who said they probably wouldn’t go to Starbucks if not for the app.

I think the Starbucks app is one of Starbucks’ key competitive advantages against regular coffee shops. The app seems to be attracting young customers, and the technology costs can be spread out over the company’s thousands of locations. In addition, the app is instrumental in the customer loyalty program and data collection. Single-location coffee shops simply cannot afford to compete with Starbucks on its technology.

Starbucks’ other advantages are its drive-throughs, its tens of thousands of combinations of drinks (some sources say over 100,000), and its brand power. If you think about it, single-location coffee chains can easily beat Starbucks on customer connection. But single-location coffee shops cannot beat Starbucks on convenience, selection, technology, and brand. Also, chains like McDonald’s can offer drive-through coffee, but they just can’t match the quality, brand, and selection of Starbucks. There’s a reason Starbucks coffee is priced at a premium.

In summary, while the barista-to-customer connection was instrumental in building Starbucks, I think Howard Schultz is now missing what separates Starbucks from single-location specialty coffee shops: its technology (app), drive-throughs, selection, and brand.

Is Starbucks’ Negative Shareholders’ Equity A Problem?

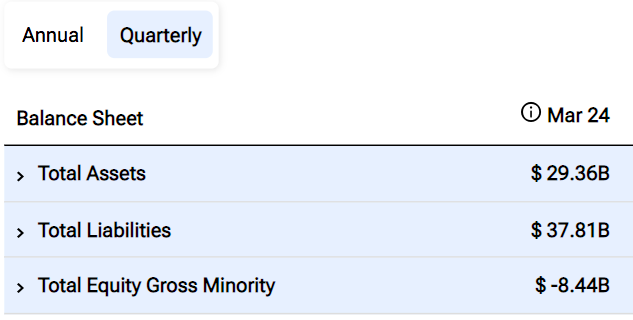

As we can see on Starbucks’ balance sheet below, the firm has a pretty deeply negative shareholders’ equity, with its liabilities exceeding its assets. While this would be a problem in most industries, it’s not a big issue for Starbucks. The company has had negative equity for many years. In this regard, the company is similar to McDonald’s (NYSE:MCD).

So, why is this not an issue? Well, first off, Starbucks’ assets are understated on its balance sheet. Real estate assets such as buildings are often carried on the balance sheet at historical cost (the cost at which they were purchased). Then, they are depreciated over time. Starbucks has maintained these assets pretty well, and the U.S. money supply has grown tremendously. This means that these assets are likely worth way more than their purchase price, not less. Thus, their balance sheet value is likely understated.

Second, the Starbucks brand carries tremendous value. If Starbucks were to sell its brand, it would command a massive sum of money because it is world-renowned and gives the company pricing power. This, too, is not carried on Starbucks’ balance sheet at its true value.

So, if Starbucks were to carry its brand and its real estate on its balance sheet at fair market value, its shareholder’s equity would likely be positive and fairly robust. Now, is the company carrying too much debt and capital lease liabilities? Maybe a little. But if we look at its interest coverage ratio, the company’s operating income covers its net interest expense by more than 12x, which is excellent.

The Valuation

Also, the value of Starbucks is not its balance sheet; rather, it’s the firm’s future cash generation. To eliminate the effects of growth CapEx on free cash flow, I instead prefer to look at Starbucks’ P/E ratio, which sits at 22x. This gives investors a starting earnings yield of 4.5%, which is attractive for a company with Starbucks’ growth prospects and predictability.

China Will be Fine

Luckin Coffee (OTC:LKNCY) has been expanding rapidly in China, and there seems to be some price war dynamics going on. This is typical behavior for Chinese companies, which often try a little too hard to gain market share, sometimes at the expense of profitability. I think Starbucks has taken the right approach in refusing to engage in price wars.

Starbucks’ CEO said the following in the Q2-2024 call: “I think the growth that’s taking place in the mass area of the China business, of the China overall coffee and tea segment, is one where we see just intense price competition. We’re choosing not to participate in that. We are a premium brand.”

It may be prudent for Starbucks to slow its store openings in China in the meantime, but overall, I think the Chinese consumer has a lot of cash to spend (Chinese savings rates are extraordinarily high). In light of this, I’m looking for ways to get exposure to China without taking on undue geopolitical/ownership structure risk. Starbucks may be one of those avenues.

Is SBUX Stock a Buy, According to Analysts?

Currently, eight out of 26 analysts covering SBUX give it a Buy rating, 18 rate it a Hold, and zero rate it a Sell, resulting in a Moderate Buy consensus rating. The average SBUX stock price target is $88.78, implying upside potential of 10.7%. Analyst price targets range from a low of $75 per share to a high of $112 per share.

The Bottom Line on SBUX Stock

As the largest coffee chain in the world, Starbucks’ competitive advantage no longer comes from its customer relationships but from its technology, data, brand, drive-throughs, and selection. These advantages cannot be matched by coffee chains and family-owned shops alike. Therefore, I believe Howard Schultz was wrong to denounce the company’s app.

There are many reasons to be bullish on Starbucks. Between its plethora of competitive advantages, its invaluable brand and real estate (which is understated on its balance sheet), and its rebound potential in an extremely cashed-up Chinese economy, I’m bullish on SBUX at a P/E ratio of 22x.

Looking for a trading platform? Check out TipRanks' Best Online Brokers , and find the ideal broker for your trades.

Report an Issue